The Chinese simply did what every Economics textbook currently in print says you are supposed to do. When confronted with a downturn, no matter its size you borrow your way through it. In fact, it says the greater the contraction the more you need to lean on finance. The neo-Keynesian model is unyielding on the matter.

Using debt to boost aggregate demand in the short run is already tempting fate. But let’s set that aside for a moment. There’s a more basic and bigger problem to consider, one which is derived from the original assumption – and it is an assumption.

Any Keynesian in good standing knows that the debt they are advocating is a cost; there are no free lunches, they are just sold to the public that way often by Keynesians in good standing. You take on those costs to soften the blow of the worst times, and then spread them out into the better times of the future.

Therein lies the problem. What if there are no better times?

It is taken for granted that there will be. Contractions are viewed from the perspective of the business cycle; or, to borrow and paraphrase a cliché, what goes down must come up. It is simply never considered that an economy once down might stay down. Why it might is another matter entirely.

In that shape, you’ve underwritten a whole lot of debt under false pretenses. It may have softened the blow during the original contraction, and that’s arguable, but in that future you’ve set yourself up for the very procyclical forces you’ve tried to countermand. Rather than more easily absorb the weight of debt during robust growth when you can best afford it, you’ve created a massive burden that without robust growth instead spreads out the pain.

The complications for China came during the early “recovery” period. The developed world economies had emerged from the Great “Recession” under a “new normal.” There was nothing normal about it, of course, so it was an attempt to sell suspiciously low growth to the Western public expecting a business cycle. Something had changed and it changed around 2008, but officials couldn’t quite bring themselves to put their finger on it.

It should’ve mattered to the Chinese, but for various reasons it was assumed China and other EM’s would continue to grow unimpeded even without their end markets in reasonably healthy shape. To this day, I don’t really understand how so many people rationalized this dichotomy; the US and Europe aren’t coming back so China won’t be able to sell as much goods to them as they were expecting back in ’07, but this won’t matter because EM’s always grow!

The sharp finance-driven rebound in 2010 and the first half of 2011 seemed to underscore this widely-held belief. No matter what, China would find a way. It was the government’s mandate, after all, for growth at all cost.

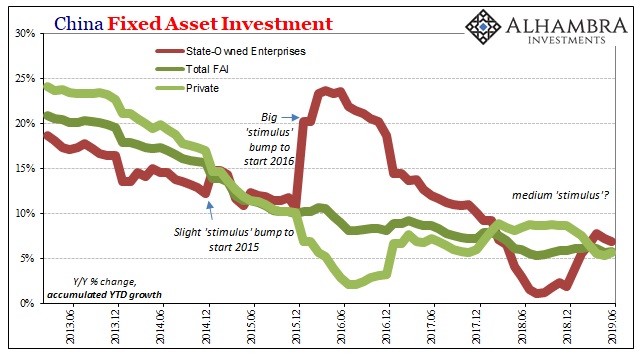

This is where “rebalancing” came in. It was one of several of these rationalizations. If the US and Europe weren’t going to be dependable end markets (and where the Chinese had always disagreed about what were always described as “strong” Western economies) then China would simply conjure one of its own inside its borders.

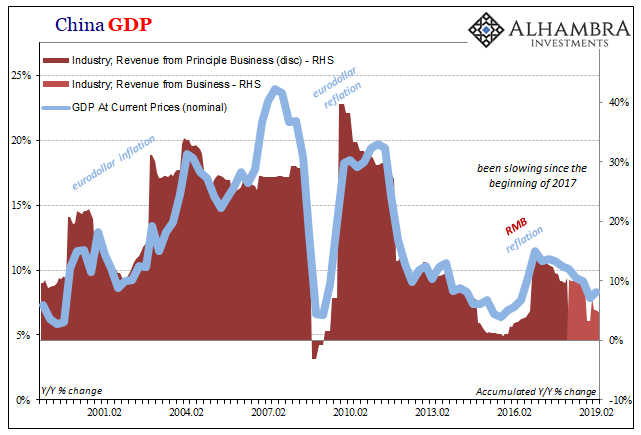

The vast Chinese industrial sector, strained by the debt taken on in 2009 and 2010 to manage a temporary decline, and unable to sustain that debt by 2012 selling only into US and European markets, then China’s consumer markets would be made to pick up the slack.

How? Nobody really knew. Rebalancing wasn’t a plan so much as a slogan.

Euro$ #3 when it hit in 2014 really called everything into question. China’s economy slowed even more than it had after 2011, way below the thresholds of what “conventional wisdom” had assigned as reasonable. For the first time, China and EM decoupling didn’t seem so assured (which is why they were pounded by the eurodollar squeeze). The entire post-crisis premise wasn’t just being challenged, it was being directly disproved.

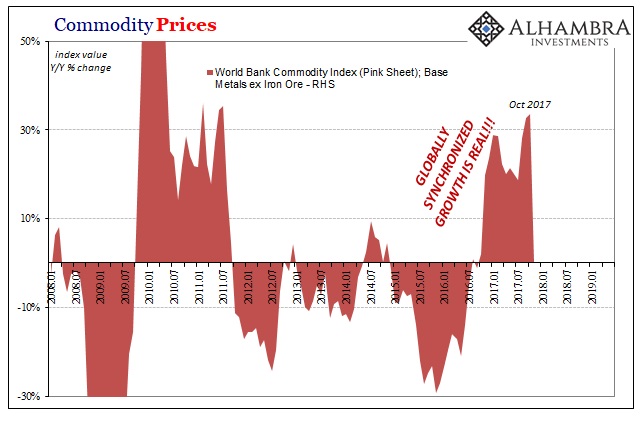

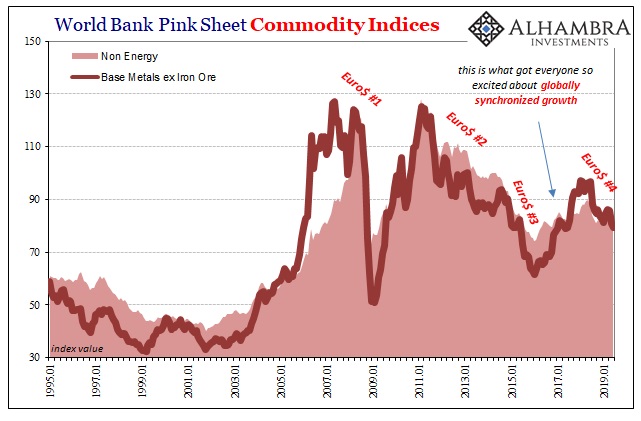

It’s one key reason why the Communists panicked in early 2016. Fiscal stimulus was unleashed, driven by even more debt. To the Keynesians in the West, it was welcome relief in order to set the stage for globally synchronized growth in 2017.

The Chinese, by contrast, were abhorred. As they saw in their own numbers, globally synchronized growth wasn’t a plan so much as a slogan. A whole lot more risk for very little gain, with Western denial about the true state of the global economy just making it worse.

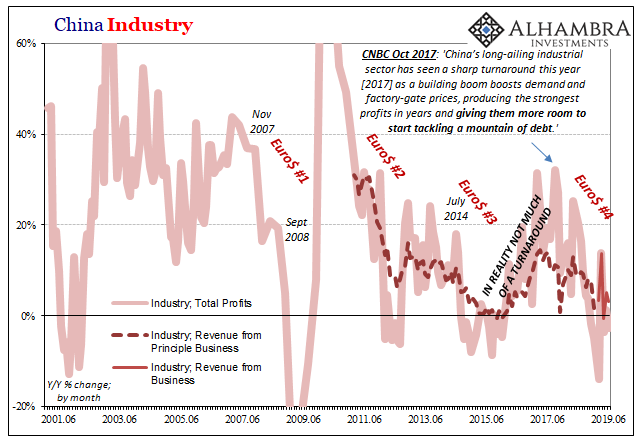

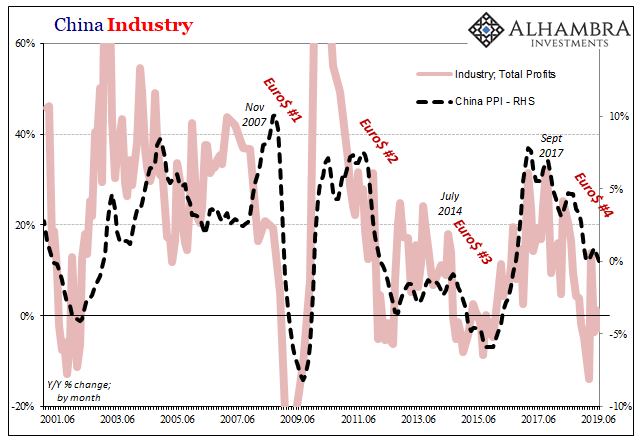

A big part of that denial was derived from how some of the numbers seemed to be substantial, good evidence (in the absence of context) that 2017 was different – meaningfully different. China’s vast industrial sector put up a lot of them. For September 2017, for example, Industrial Profits rose by more than 30% year-over-year, with revenues up by double digits.

It did appear on the surface as if the two slogans had been merged into beautiful synergy; China’s rebalancing and globally synchronized growth, the perfect combination for a global inflationary breakout. Just in time, as one contemporary CNBC article noted:

China’s long-ailing industrial sector has seen a sharp turnaround this year [2017] as a building boom boosts demand and factory-gate prices, producing the strongest profits in years and giving them more room to start tackling a mountain of debt.

The article was written in late October 2017. Barely a week before, China’s ruling Communists had written a very different message for the Chinese people. The short version was this: quality growth over quantity. I’d say it was an unmistakable message announcing a no-growth world, but the Western media, Economists, and policymakers (redundant) intoxicated by inflation hysteria all mistook or missed it.

The danger wasn’t just in terms of economy. As CNBC (CNBC!!) realized, “room to start tackling a mountain of debt” was an enormously consequential assumption. What if there is no room? What if there is never going to be?

I have little doubt this is why Japanese banks chose October and November 2017 to, frankly, run for the hills. If China’s rebalancing was a sham and globally synchronized growth total delusion, then economic risks while already substantial they would be incredibly compounded by financial risks – nowhere more than in China.

Debt taken on over the last decade was underwritten for very different times. How it all gets sorted out eventually cannot be adequately predicted. That’s what risk means. Rising risk means many people (and financial agents) are finally figuring this out. It’s not trade wars, another realization which is becoming more widespread as this year drags on.

Halfway through 2019, Chinese industrial profits are shrinking again and showing no signs of turning around. Industrial revenue growth is below 5% (accumulated) for the first time since 2016 – and is still decelerating (on a monthly basis in June 2019, revenue growth was just 3%).

If a Chinese industrial renaissance in 2017 was “room to start tackling a mountain of debt”, what is a renewed industrial slump in 2019? Heightened, self-reinforcing financial and monetary risk. I’d say it was unmistakable, but there’s, you know, rate cuts this week.

Stay In Touch