The yield curve’s inverted! The yield curve’s inverted! That was the news I awoke to last Wednesday on CNBC as the 10 year Treasury note yield dipped below the 2 year yield for the first time since 2007. That’s the sign everyone has been waiting for, the definitive recession signal that says get out while the getting is good. And that’s exactly what investors did all day long, the Dow ultimately surrendering 800 points on the day. I don’t remember anyone on CNBC mentioning it – although surely they must have – but by the end of the day the curve actually ended up back in positive territory, the inversion lasting less than a day. So, never mind. Maybe.

Of course, the 10/2 curve is only a small slice of the yield curve and other parts have been inverted for some time. Indeed the Fed’s research says the 10 year/3 month curve inversion is the most accurate for predicting recession and it has been inverted since May, although you can be excused for not knowing that since no one seems to care. No, the one that gets everyone’s attention is the 10/2 curve, the granddaddy of all the yield curves because, well, just because, okay? It’s the curve everyone is watching and the people watching the people who are watching it think it’s the curve the watchers think is most important, so when it inverts, well you just have to sell because you don’t know how long the watchers of the curve watchers are going to wait before they get worried that all the watchers of the watchers of the curve watchers are about to sell, so sell and ask questions later because Lord knows I’d rather be early than late, right?

Is it possible that there is anyone left in America who doesn’t know the yield curve inverts prior to recession? Based on the recent experience of one of our partners, I’m going to climb out on a limb and answer a resounding no. This partner bought a house a few years back and recently had to replace a door. It’s an older house and the door is a non-standard size so he called a door company who promptly sent someone out to hang a new, custom door. The installer noticed the partner was watching the market and a conversation ensued in which the door installer talked at length about the importance of the yield curve and how things were bound to get worse now that the inversion had arrived. Sell your stocks, he warned the partner, and buy bonds.

There’s an old story on Wall Street about how Joseph Kennedy sold all his stocks in 1929 when the shoeshine boy started offering him stock tips. There is some evidence that Kennedy was short stocks into the crash of ’29 but whether that was due to his shoeshine boy insight is unknown. True or not though, the story does impart a certain wisdom about crowds, namely that one can have wisdom but only until the crowd reaches a critical mass of the masses at which point wisdom turns to conventional wisdom. And we all know what conventional wisdom is worth.

I don’t know if the door installer knowing about the yield curve is evidence that its predictive power has diminished to the point we can safely ignore it. And I surely don’t want to belittle door installers as the equivalent of shoeshine boys. Hanging a door isn’t as easy as it looks and down here in South Florida where that door may be what stands between you and a 175 MPH wind, getting it right is pretty dang important. But I have been doing this a long time and the focus on this one indicator has reached an extreme. The recession fears seem totally out of proportion to what we see in the economic statistics and other indicators we use to judge the health of the economy.

No, I’m not saying it’s different this time although it very well may be. The yield curve’s predictive powers have been perfect since about 1980 but it isn’t the definitive indicator for recession everyone today seems to believe it to be. It doesn’t work in every country and it doesn’t need to invert prior to recession. It also can and has inverted in the past without a subsequent recession unless you want to say the brief ’98 inversion predicted the 2001 recession. You’re perfectly welcome to do that but 2 or 3 years early falls into the category of wrong in my book.

The 10/2 curve also inverted briefly in February of 2006 about 22 months before the last recession. Is that a false positive? Call it what you want but the 2006 inversion certainly didn’t warrant taking the door installer’s advice and selling your stocks. The S&P 500 rose another 23% after that 2006 inversion, a gain that would have been very hard to ignore in real time. Even if the inversion does signal recession ahead, it doesn’t mean you need to swerve across four lanes of traffic to hit that exit ramp.

Do yield curves today mean the same thing they meant 10 years ago? 20 years ago? 30 year ago? Does widespread knowledge of the yield curve and its past behavior change its predictive nature? Do investors taking actions in the market based on their limited knowledge of the yield curve change the shape of the yield curve? Has central bank intervention in the Treasury market – QE and QT – affected the yield curve? Is it coincidence that the Fed announced the end of QT and the long end of the market promptly rallied, producing the inversion everyone was already expecting? I don’t know the answer to those questions but I think they are ones that we need to consider when viewing the Treasury market.

I also think it would be wise to ignore the current panic over a potential recession – and yes in a way it is a panic – and take a more deliberate approach to analyzing the economy. We don’t rely on one indicator to guide tactical changes to our portfolios. We require multiple indicators to agree on the current state of the economy. The yield curve may be saying that the economy is headed for recession but it is, at least for now, a lone voice.

Meanwhile, our other main bond market indicator, credit spreads, are well behaved. And stocks, although not one of our primary indicators, are well less than 10% from their recent high. That isn’t “recession is right around the corner” action. Our broad based indicators like the CFNAI tell a story we’ve been writing for over a year, namely that the economy is slowing back to trend after a brief surge from the tax cuts. All the other indicators we use privately and don’t share with the public say the same thing. And the yield curve inversion isn’t a recession signal in any case. That would be when the curve steepens rapidly as the market anticipates multiple, deep cuts from the Fed. We aren’t even close.

We understand the fears pulling the market in all directions over the last couple of weeks. The administration’s trade policies create vast uncertainty for investors and business operators today in exchange for, hopefully, fairer trade tomorrow. Unfortunately, fairer – assuming such can be achieved – does not necessarily mean better for everyone. That wasn’t true of freer trade and it won’t be for less than free trade. There will be winners and losers and no way to know today who they might be. But we see most of this as distributional anyway, with the US economy mostly absorbing whatever damage the tariffs do without much impact on growth. The economy has slowed back to the trend that prevailed before Trump took office. That’s not great but it isn’t recession either. So forget the yield curve until it does something that really deserves your notice. And ignore the door installer.

Economic Reports

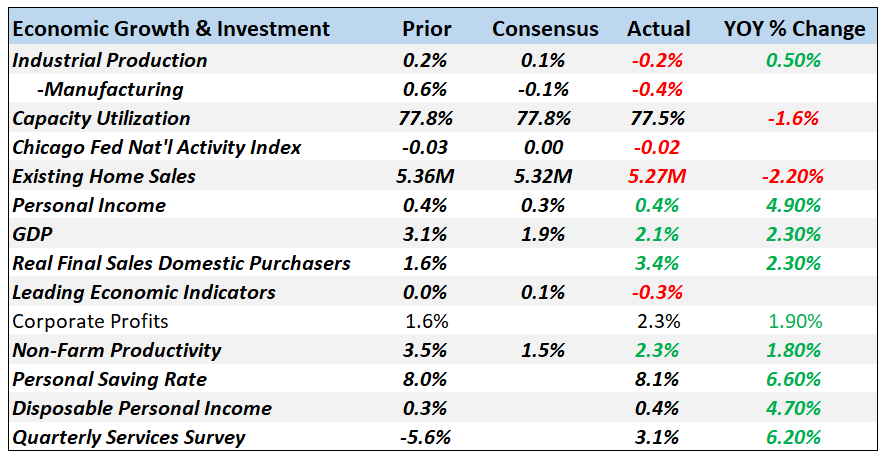

Economic Growth & Investment

This slowdown is primarily about manufacturing. Industrial production is down but its just minor so far. The CFNAI at -0.02 and a three month average of -0.26 tells the story. We’ve slowed but just back to the previous trend. Obviously, that is just where we are now and not where we might go but the recession talk is just way overblown right now.

As for long term implications for the economy the most interesting stat here is the savings rate. The savings rate fell pretty steadily from 15% in 1975 to 2.2% in 2005. It has been rising steadily since is now up to 8.1%. This new frugality may be the most significant thing to happen the the US economy in decades.

Personal income is rising again which is good news but keep in mind that incomes don’t usually fall until after the recession starts.

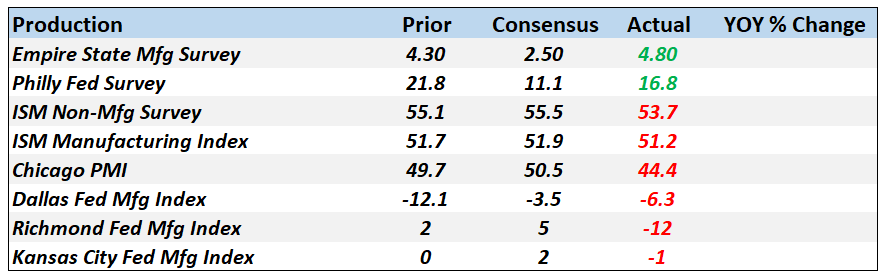

Production

The most recent reports – Empire State and Philly Fed – both improved. Start of a trend?

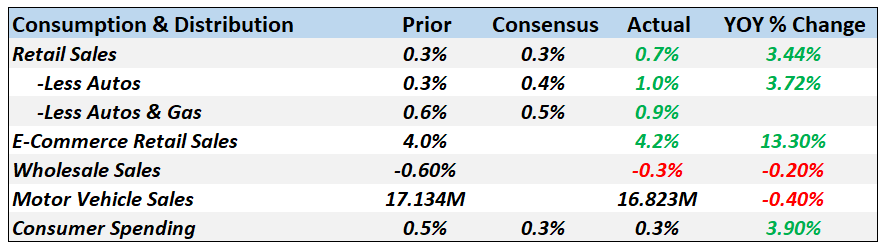

Consumption & Distribution

Retail sales have been steady if unspectacular in this expansion as people are saving more. And like income, it is a lagging indicator so doesn’t tell us much about the onset of recession.

Inventories

Inventories have stopped building. I still don’t know how much of this inventory build was intentional as a way to avoid tariffs. But right now, inventories appear to high and will need to be worked down one way or the other. That’s isn’t particularly good news for current production.

Orders

Core capital goods orders are the good news here but as I’ve pointed out many times before, these orders are barely higher today than they were in 2000. Our economy has changed a lot since then but I don’t think so much that this is an expected or satisfactory outcome. It is at the high for this cycle though.

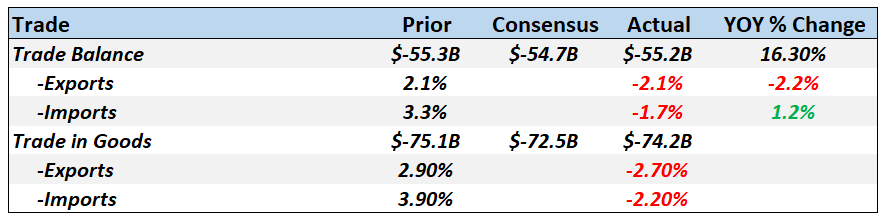

Trade

I have no idea how to interpret this data in light of the ongoing trade war. Suffice it to say that contracting global trade is not a good thing.

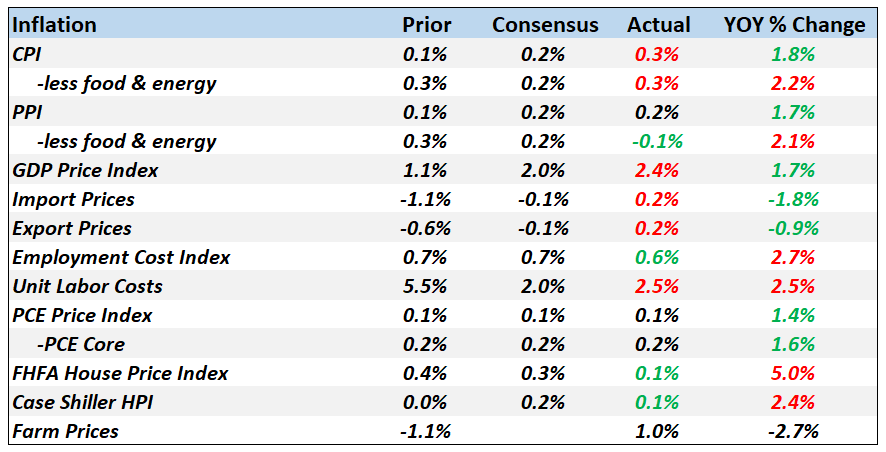

Inflation

Inflation is still fairly tame but I wonder if that will last if the trade war continues. It takes time for this stuff to feed through to consumers, something Peter Navarro doesn’t seem to understand. I am stunned, on a near daily basis, at the ignorance that comes out of Navarro’s mouth. I don’t care how you feel about Trump or the Chinese, this man shouldn’t be anywhere near the economic leadership of this country.

Employment

Employment is slowing and jobless claims appear to have hit bottom. In past cycles, claims hit their low well before the onset of recession. In the last cycle, the low was in January of 2006, nearly two years before the start of recession.

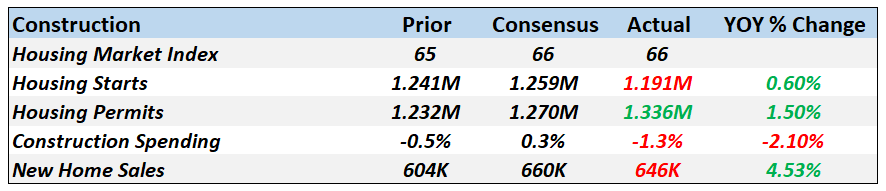

Construction

Construction continues to disappoint but at least permits ticked higher last month. The recent weakness in starts has been in multi-family too which doesn’t impact the economy as much as single family. Public spending has recently slowed too, impacting overall spending negatively.

Other

The recent drop in Consumer Sentiment is all about the tariffs.

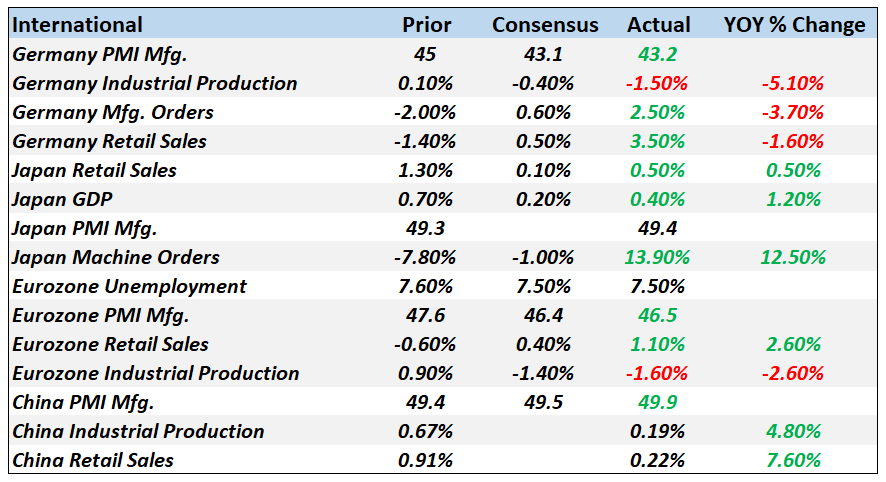

International

There’s a lot more green in the international section than you’d expect given the recent commentary. Germany is obviously slowing and a lot was made of last quarter’s contraction. But it was minor – -0.1% – and not that bad considering the slowdown in global manufacturing. In Japan meanwhile, growth surprised on the upside. Everyone seems to believe that a global recession is inevitable but it sure doesn’t show up in this data.

The economy has slowed back to trend just as we expected. It could surely continue to get worse but our job is to see the present with clear eyes, not predict the future. I’ll cover all our market based indicators in a separate post but the recent inversion of the yield curve probably doesn’t mean what it once did. And it surely doesn’t mean much until there are other indicators that also point to recession. And right now, we just don’t have any confirming signals.

Stay In Touch