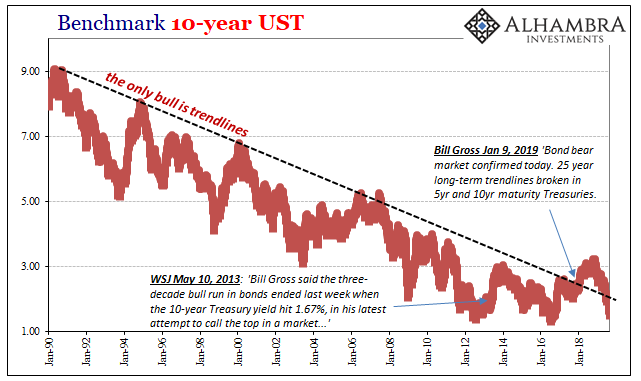

In January 2018, Bill Gross was at it again. Famous for being the longtime public face of PIMCO, he’d acquired as much notoriety for being the boy who cried bear. By the way he talked and by what he predicted, you’d have to think the US Treasury had visited some horrible circumstance on a young Bill early in his life. It’s like he was possessed with unnatural hatred bonds for some reason.

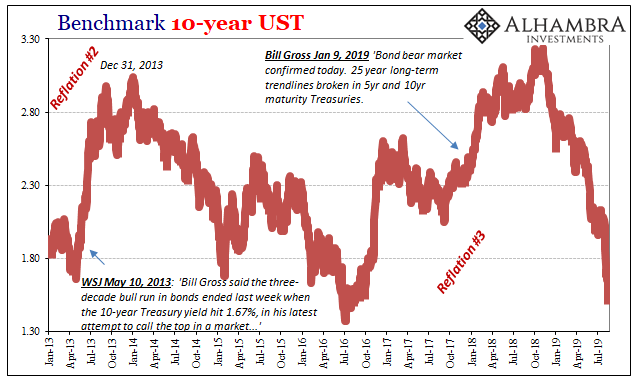

Gross: Bond bear market confirmed today. 25 year long-term trendlines broken in 5yr and 10yr maturity Treasuries.

— Janus Henderson U.S. (@JHIAdvisorsUS) January 9, 2018

In truth, he just disliked low interest rates because as a quant trader, a pioneering one for the bond market, he presumed that the next big payday in the sector would be a rout. With interest rates so low following the 2011 crisis, Gross reasoned that with a third (and fourth) QE they really had nowhere to go but up. Surely, Bernanke wouldn’t fail a third time (and a fourth).

What is this, Japan?

A joke, sure, but there’s truth underneath. People have a very, very hard time believing that the US economy (or the world economy, for that matter) could eve be darkly diving down the path set by the Japanese a decade or so before. No freakin’ way.

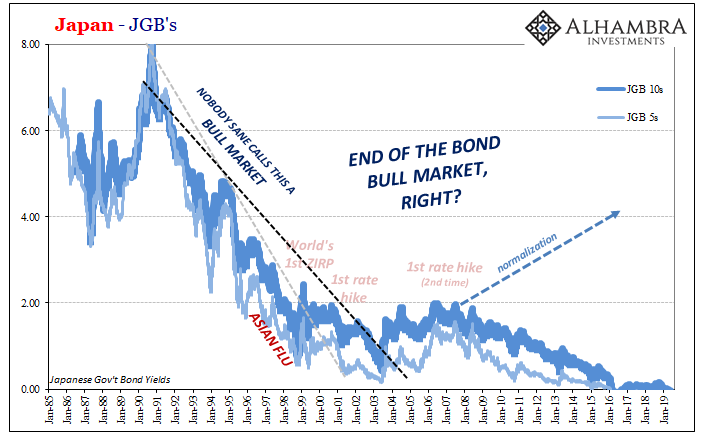

It didn’t matter that the Japanese had even gone through the same hysteria. In the middle 2000’s, JGB yields rose to their highest level in many years. Economists as central bankers were thrilled at how a combination of two QE’s along with continued zero interest rate policy (ZIRP) when given enough time seemed to have been effective.

Seemed.

The “bull market” in bonds was declared ended several times, the Japanese told to brace themselves for higher interest rates. And if not all the way back to nominally like they were in the eighties, then at least partial normalization much closer to that than zero.

The US is not Japan! The US is not Japan! The US is not Japan!

That’s all this really amounts to. The Japanese allowed themselves to fall into their “deflationary mindset” largely because their central bankers were ineffective. That’s exactly what ours said in June 2003. They actually laughed at how they would perform so much better, especially as the US economy had the added benefit of (assumed) structural factors going for it that the Japanese did not.

They might lose a decade maybe two, but it was viewed as an impossibility outside of Japan. The problem with Japan, everybody said was Japan.

Persistently low bond yields elsewhere proposed a very different view on where the problem might be located.

This was the emotion underneath the constant stories and proclamations about the BOND ROUT!!! throughout 2017 and into 2018. Bill Gross declared the US Treasury “bull market” at an end in January 2018 for that reason. Enough was enough. QE had begun to flower in the economy and he could see nothing on the horizon which would further keep the US economy from reasserting its differences.

All the models pointed in the Fed’s direction (not least because all the models are derived from the Economists who work at the Fed). Any attempt to equate the US Treasury market with the JGB market was deemed plain silly; not worth legitimate consideration.

What Gross and others never considered was that the comparison really wasn’t between the US and Japan. Rather, the only assessment worth anything was if the US (or anywhere else in the world) had become meaningfully different itself; the key word, the trillion-dollar word, is meaningfully.

In many people’s estimations, that trend line you see above qualified as “meaningful.” It was sold to the public that way many times over. It’s just a dotted line.

Only a few weeks after UST rates rose to their highest in years, affirming for many Gross’ bond bull wisdom, in late October 2018 I wrote that it would still be much better to take a second look at Japan and realize its bonds were simply saying – nothing has changed. Just as the landmine was starting to emerge, confirming that in US market fact:

Given what’s going on now, I wouldn’t be at all surprised if over the next multi-year period UST rates not only register new lows less than 2016 but follow Japan’s under zero for a large part of the curve. It may take some time, there will be resistance from the short end with central banks the last to figure out what’s really happening.

Why?

Because nothing has changed. Eleven years of “accommodations”, ZIRP’s, and global QE’s and we are still staring at another downturn. The (non-linear) contraction remains in place – worldwide.

As interest rates tumble not skyrocket in 2019, the cries of BOND ROUT!!! have largely faded. They’ve been replaced by puzzled wonderment and in many cases outright anger (how could this be!) The bond king Bill Gross is gone, a conveniently timed retirement just as this latest “bull” was getting going again.

The BOND ROUT!!! is not dead, though. Shriveled and sullen, it still shows up from time to time in whispers even just recently. For some, if they thought bonds were in a bubble last October, they must be in a huge one now.

Investors are starting to question the epic bond rally that’s driven global yields to new lows and fueled the U.S. Treasury market’s best performance since the era of quantitative easing.

The warning signs go beyond this week’s failed German 30-year bond auction, which showed that demand may be faltering for negative yields across Europe, even amid growing evidence of ebbing economic growth.

People say the stock market bull rally is the most hated one imaginable. Not even close, especially where the mainstream financial public is concerned. There’s been no more steadily questioned and cussed market action than stubbornly low and lower interest rates.

Contrary to the line, investors have simply embraced the logic that QE and ZIRP beliefs cannot.

People will still have a very hard time accepting what this latest rally in bonds truly means. First, nothing has changed. Second, that means we are following Japan. Third, and what hurts the most for the media which loves, loves the very idea of a technocracy that the Fed represents, is that US central bankers (and European) are, and have been proven to be, just as incompetent as their Japanese counterparts despite having the Japanese example to work from.

The only part that’s really true in the mainstream view, is that there really is a lot of bull when it comes to bonds. And that’s before we even get to term premiums.

Stay In Touch