Germany’s Finance Minister Olaf Scholz ignited and invited controversy today when he signaled that the federal government is looking at a possible suspension to constitutional budget measures. With a nasty political fight certain to follow, even temporarily adjourning the country’s so-called debt brake would not be easy. With Chancellor Angela Merkel’s party already in a precarious position, one might wonder, why now?

The mere hint of a softening to the prevailing budget position picked up an immediate, and obvious, champion. ECB Governor Christine Lagarde was practically overjoyed upon hearing what is to now just a rumor (really a trial balloon). Speaking in Wiesbaden, Lagarde remarked, “Any fiscal measures intended to support the economy are certainly very welcome, particularly under present circumstances.”

What are those “present circumstances” one might also wonder? You can go back only a month to the last ECB meeting and press conference for clarification. On January 23, the new head of Europe’s central bank had sounded quite differently. She had said:

The incoming data since our last meeting are in line with our baseline scenario of ongoing, but moderate, growth of the euro area economy. In particular, the weakness in the manufacturing sector remains a drag on euro area growth momentum. However, ongoing, albeit decelerating, employment growth and increasing wages continue to support the resilience of the euro area economy.

It’s the same message as you hear from any central banker located anywhere. Some overseas stuff that’s to bother about manufacturing, but unemployment rate. Strong economy otherwise.

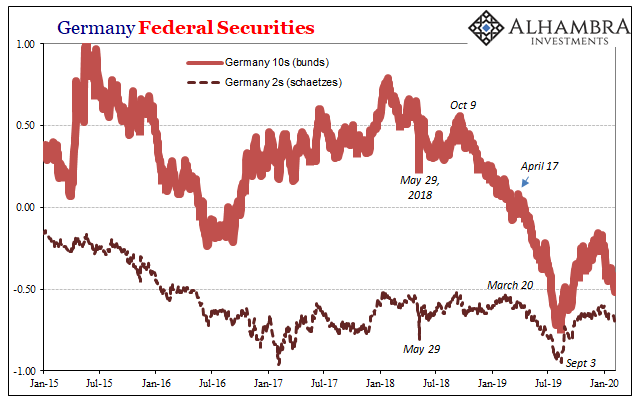

For a time, it had seemed like the bond market, central bankers’ fickle nemesis, was in agreement. After plunging throughout much of 2019 and frightening even mainstream media members into questioning the unemployment rate narrative, yields backed up – a touch. It was called an all-clear anyway.

Now nearly two months through 2020, Germany and everywhere else is right back into that same position. Had anything really changed? Yes, but not for the better.

Officials will undoubtedly run for cover under the coronavirus. But even some chief Economists at Big Label firms aren’t buying the latest “transitory” factor excuse. When your closest allies declare themselves tired of hearing it…

Carsten Brzeski, chief economist at ING Germany, last week declared his exasperation at the all-too-predictable evolution in the official outlook:

Even though we would expect the ECB to look through the short-term impact from any adverse external developments, January’s optimism will be hard to maintain at the March meeting. It has happened too often in the recent past that initial short-term or one-off factors quickly morphed into more structural problems for the eurozone economy.

Again, no wonder Lagarde pitched in her full support for Germany’s fiscal flirty temptation. The only real question is whether she actually believed what she said back on January 23.

It would have been hard to, but it’s not beyond the capacities of central bankers to deny their lying eyes. In fact, it seems the defining quality government authorities look for in putting forward candidates, particularly those like Christine Lagarde.

In any case, the more the data comes in the more it looks like any January optimism had been hugely misplaced. And we haven’t even gotten into 2020 figures yet. Where improvement, at least stabilization, was declared to be, all the numbers for the end of 2019 instead keep turning up as some shade of only ugly.

The idea has been as Lagarde spelled out in her quote above; overseas turmoil which has only impacted manufacturing and maybe industry, and mostly as it has to do with outward facing sectors. Exports and trade (thus, the whole “transitory” trade wars focus).

Overall, Europe’s economy is otherwise healthy because employment, though it is a lagging indicator, it still indicates everything’s just fine.

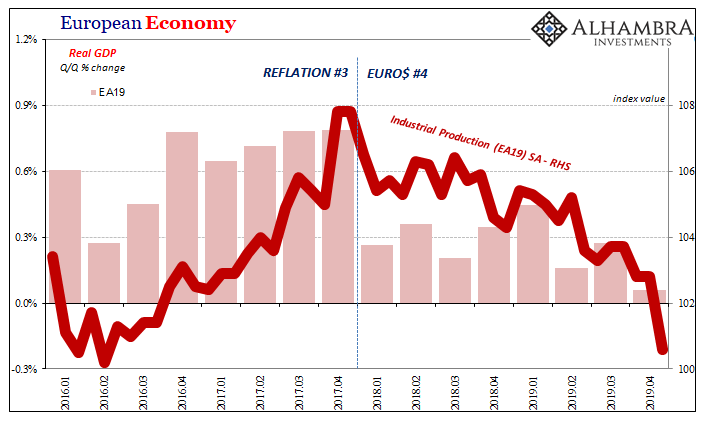

That view is pretty much supported by the data – except for the “just fine” bit. The manufacturing and global trade recession has already sapped most if not all of Europe’s (and the rest of the world’s) growth. Coming in on the close of 2019, there was already more than a whiff of that nasty recessionary smell.

To get all the way there, Lagarde was right in that it would take more than manufacturing. The industrial downturn would have to erode enough positive domestic factors to complete the full potential of this downswing. Things like building and consumer spending.

What we see in those specifically are once again how the entire European economy, not just Germany within it, finished up 2019 in very bad shape. As it was supposed to have been getting better, instead acceleration only to the downside.

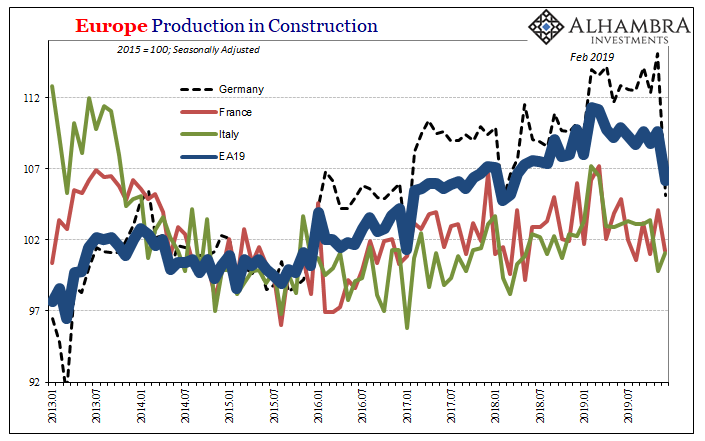

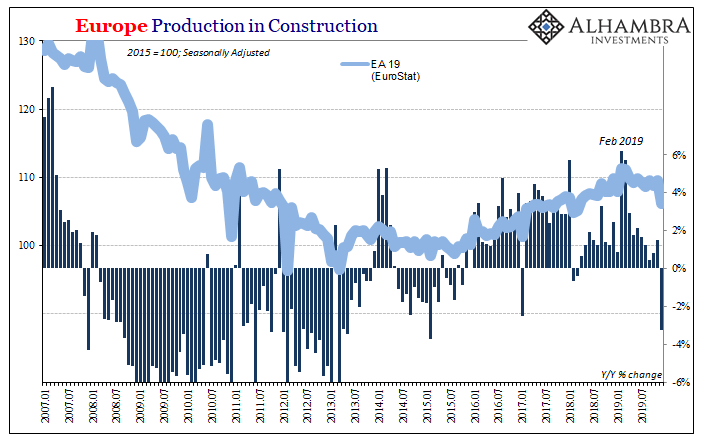

It took a full year of the trade and industrial downturn before construction across the Continent reversed its hard-won (some would say) upswing following Euro$ #3. And then production in construction tanked in December 2019.

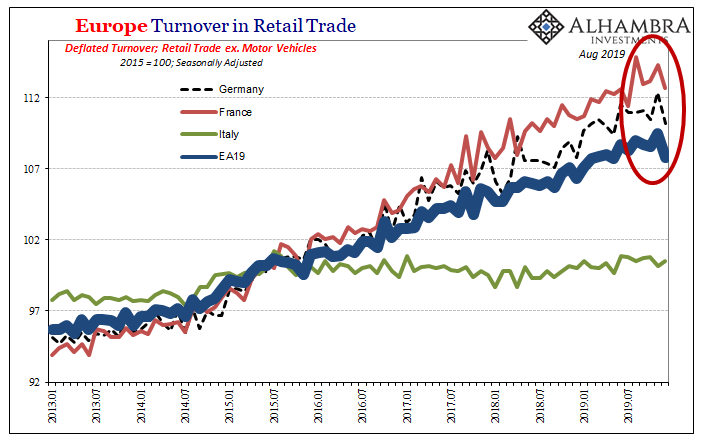

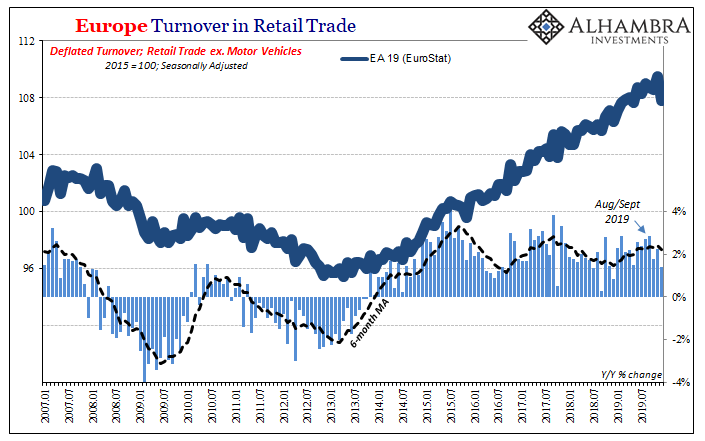

Retail trade was seemingly unaffected by the decay in European economic fortunes until August and September. Just as everything was supposed to have been getting right, these estimates suggest instead the weakness was indeed spreading inward. Like Industrial Production and Production in Construction, Retail Trade also seems to have taken a bad step in December 2019.

And that’s all before we get to any fallout from COVID-19.

I have to hand it to this one Economist, practically exhausted from hearing the officially optimistic case perhaps one too many times. The excuses are piling up unlike the prospects for a return to meaningful growth.

It has happened too often in the recent past that initial short-term or one-off factors quickly morphed into more structural problems for the eurozone economy.

Not just Europe. That’s just where the negative effects, the global disinflationary pressures, of ongoing Euro$ #4 seem to land first.

Stay In Touch