The unemployment rate wins again. In a saner era, back when what was called economic growth was actually economic growth, this primary labor ratio did a commendable job accurately indicating the relative conditions in the labor market. You didn’t go looking for corroboration because it was all around; harmony in numbers for a far more peaceful and serene period.

Ever since the Great “Recession”, however, the unemployment rate has really struggled. Nearly the entire way during this supposedly record-length labor market win streak the measure was entirely alone in its optimism. Even the Establishment Survey took (more than) a few breaks along the way (including since mid-2018).

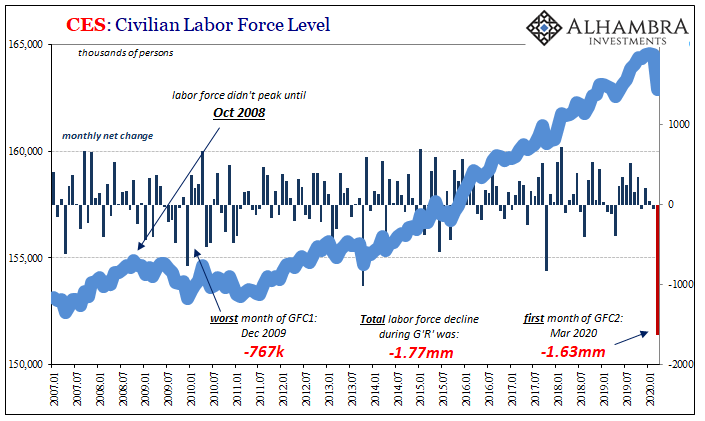

It didn’t start out like this; the unemployment rate behaved itself during the first part of GFC1. The labor force, which is what all this fuss comes down to, performed as anyone would’ve expected for a cyclical peak. Though the economy had fallen into recession way back in December 2007, the labor force kept rising with the population level until its peak was finally reached in October 2008, almost a year into the thing.

That was somewhat normal; even if you get laid off during a recession you are still part of the labor force looking for work. During 2001’s dot-com recession, for example, the labor force level wasn’t substantially changed by the contraction – only the number of American workers had shrunk. Laid off employees continued to participate by remaining in the job market.

It was shaping up to be that way in 2008, too, until AIG. The big crash changed everything. From October 2008 forward an astounding number of workers stopped looking for work. Not that anyone could’ve blamed them, there weren’t any jobs being offered. But a decline of this magnitude is and was a statement from inside the labor market about perceptions of longer run prospects.

Between October 2008 and December 2009, the US labor force actually shrank by 1.77 million.

This was the beginning of the participation problem leaving the unemployment rate unsuited to its original purpose.

I don’t really know how to properly frame the latest employment data from the BLS for the month of March 2020. What the government just reported, if anywhere close to accurate, is remarkably depressing.

I keep saying that the current economic data doesn’t matter; and it shouldn’t. But then these numbers show up and it’s difficult to see how what’s becoming so much greater of a downside won’t make a difference in the ability of the economy to bounce back. We all knew there’d be a deep hole to climb out of; this is a chasm approaching an abyss.

More and more it is being shown how the US government, as well as those around the world, have made a grave miscalculation. The “strong” economy of Jay Powell’s dream was every administration’s insurance policy to take the most extreme coronavirus countermeasures. They’d prioritize total shutdowns on the belief the economic (and financial) system could handle them.

Everyone, and I mean everyone, had listened to Economists and central bankers talk up the situation in late 2019. What recession scare, they asked by December. The economy’s in great shape moving into 2020.

Nope. It wasn’t true and now we’re going to pay the price.

The most depressing statistic is the level of the labor force. In the first month of GFC2, not even the full thing yet, and the number of Americans reporting that they are looking for work plummeted by more than 1.6 million. That’s almost as many in a single month, just the first month, as the whole Great “Recession” start to finish.

These are not layoffs or furloughs, instead potential workers who no longer see any potential. They’re out of the game entirely and it’s just the first inning.

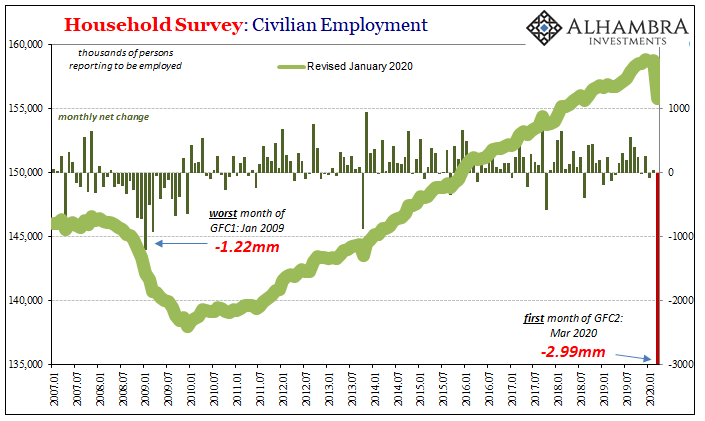

While the headline Establishment Survey finally produced a negative number, at -701k the monthly change in payrolls actually makes the economy seem strong by comparison. That comparison is the Household Survey which suggested the number of American workers reporting to be working dropped by 3 million. I’m struggling to find the words here.

The payroll figure is at least comparable even if to the worst months of the Great “Recession.” The Household Survey is, well…

Therefore, while the unemployment rate rose sharply it still understates the severity of the chasm; meaning it continues to overstate resilience and strength. It went from 3.5% to 4.4%, sure, but had the labor force not collapsed the rate would’ve been 5.3% last month!

The statistic is unsuited to our era – which is now one that includes more than one GFC. Coronavirus, sure, but that’s not all to what happened in the labor market during March. As the economic (and monetary) hole gets even wider and deeper in the coming weeks (hopefully not months), it’s going to be that much harder and require that much bigger of a miracle just to get back to even again.

GFC2 will make it impossible, especially if, like GFC1, it creates the same kind of long-term damage – which is already being indicated by just the very first monthly data. No wonder 1.6 million workers bugged out of the labor force. They can see what’s ahead because, unlike Jay Powell, they probably weren’t so thoroughly fooled about where we were coming from.

Stay In Touch