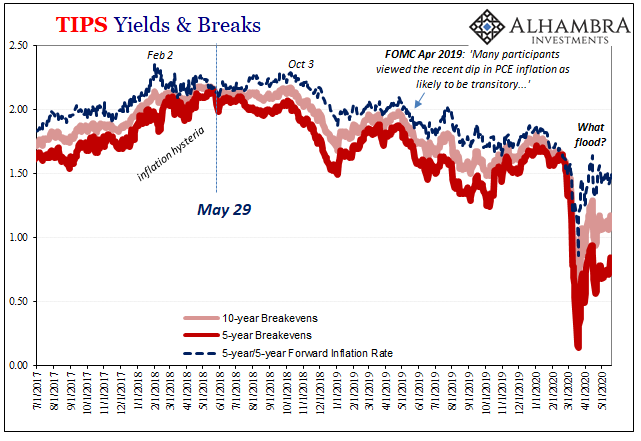

I suppose you can admire their zeal and persistence, but then again what is a zealot without his or her zeal? The desperation by which to rescue the Fed’s money printing exercise is palpable. Stocks, sure, bonds, however, aren’t making it easy. Especially inflation expectations which are crucial to Jay Powell’s fairy tale.

That whole flood.

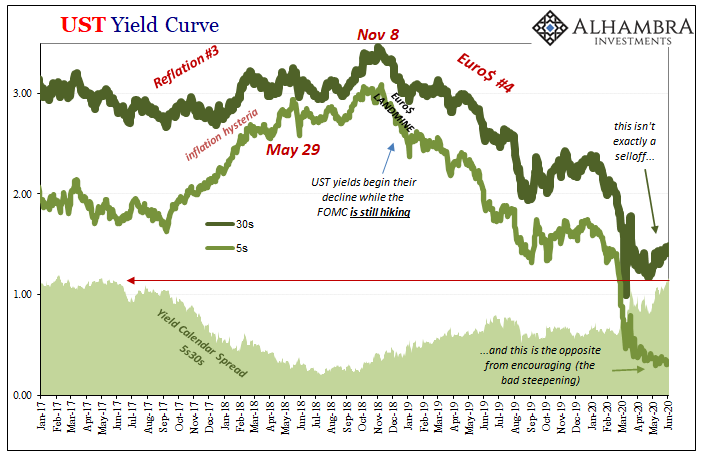

Over the last several days, Bloomberg (obviously) has been unusually and sharply focused on the 30-year long bond. The publisher like everyone else mainstream absolutely hated the damn thing for years when it was inconveniently signaling (correctly) that globally synchronized growth was a bumper sticker slogan and never anything more than that.

Now they can’t get enough of the long end. Why?

Investors in the world’s biggest bond market are starting to see what the other side of America’s worst-ever economic downturn could mean for their portfolios… “It would signal the curve may be steepening more so for economic reasons,” said Chris Ahrens, a strategist at Stifel Nicolaus & Co. “The long end seems to be pricing that we are getting to the worst of the bottoming of the economy.”

BOND ROUT!!! baby.

There’s more (another article today, thanks M. Simmons):

The re-steepening since then reflects Fed policy expectations that are keeping short-term rates low, while the Treasury boosts long-maturity supply to finance economic-recovery measures, said Guneet Dhingra, head of U.S. interest-rate strategy at Morgan Stanley. The curve’s move also coincides with a sense that the economy may be starting to revive after months of lockdown measures, with stocks hovering near the highest in almost three months.

And it’s true, the 5s30s haven’t been this wide since May 2017. Big things, right? Huge. Massive stuff befitting the Fed’s printing press explosion.

Yeah, no.

The 30s are up (in yield) a miniscule amount (31 bps since mid-April, hardly a selloff) while the 5s continue to trend lower. In other words, the bond market still views the economy as full-on depressionary. This is hardly good news (bad steepening) and doesn’t signal anything other than atrocious conditions as far as the eye can see. Even the mainstream models see this.

It won’t stop the media from claiming Jay Powell’s behind everything, too. They’re all ablaze with talks of yield caps and that’s why the short-end remains so fixed. And, as usual, no one bothers to check the Japanese experience for why this is so utterly stupid (YCC, the Bank of Japan called it, and it’s never once been put in use or has it ever been needed; there’s so much more to say about this at a later date). Series of one-year forwards, that’s all these people know.

If this is all they got in the bond market to suggest the slightest hint of “money printing” and recovery…

How the mighty BOND ROUT!!! has fallen. Now if only they could figure out why.

Stay In Touch