Italy had been one of hardest hit countries, if not the worst for a good while. For months rather than weeks, life was shut down in an effort to get ahead of COVID-19 while it ravaged seemingly unchecked. It became a buzzword of sorts, the name of the nation synonymous with the pandemic itself.

Don’t be Italy.

As a result, the economy was shut off more there than anywhere else at least so far as the data was concerned. But that kind of led toward hope and optimism; if the Italians could weather such a storm and get through it, then maybe just maybe the “V” could happen anywhere and everywhere else.

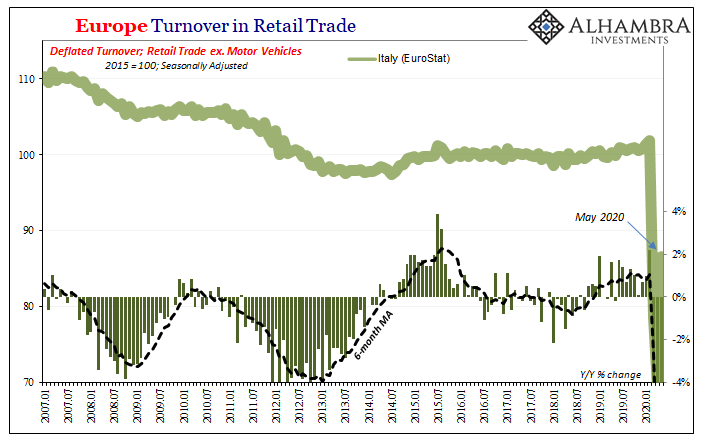

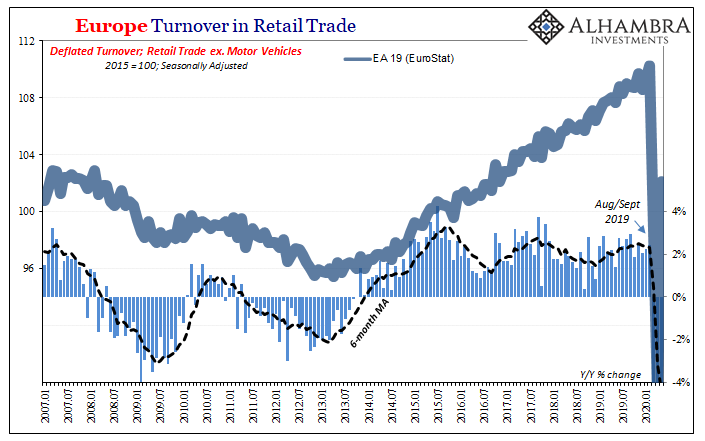

According to Europe’s Eurostat, retail sales here surged in May 2020 by an absolutely incredible 25.3%. And that wasn’t year-over-year, either, rather it was a +25% from April. Reopening, baby!

Such a gigantic positive, however, merely understates the gravity of the situation. In Italy especially, the issue isn’t just a large hole dug out of its economy, more so how this one merely the latest (and biggest) in a series of them. When you look at the track of retail sales here (below), you can’t but gawk wondering what economy? Suddenly, +25% never looked so inconsequential.

In other words, the coronavirus outbreak will end up having little to do with whatever happens next over there over the intermediate term and long run.

Not merely an isolated case, either, when you have a prolonged period of economic dysfunction it impacts the system’s ability to get back up after being knocked down. Weakness begets weakness, Italy and Europe hardly alone in sticking to that sickening standard.

The numbers are truly huge in May, and will be again in June. But then what? Retail trade actually makes it look better simply because people have to buy things no matter what, and have a ton of government cash for now with which to do some of it. Prevented from going out and purchasing during March and April, May and June will be the months where there’s catching up.

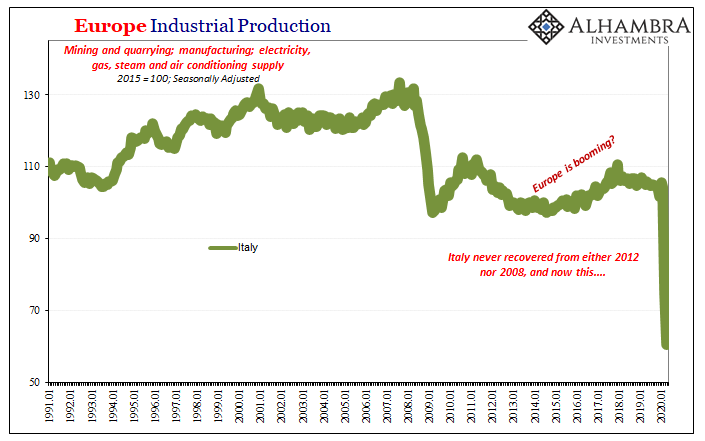

Goods producers, on the other hand, aren’t seeing it so huge on the upside. They’re the ones stuck with two and a half years (in Europe) of globally synchronized downturn. Now this.

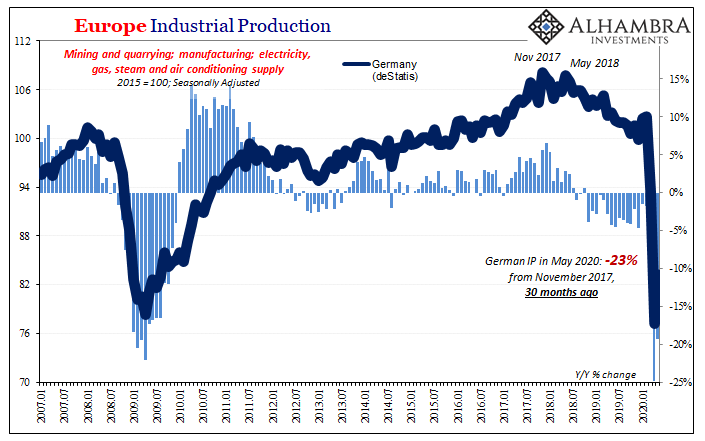

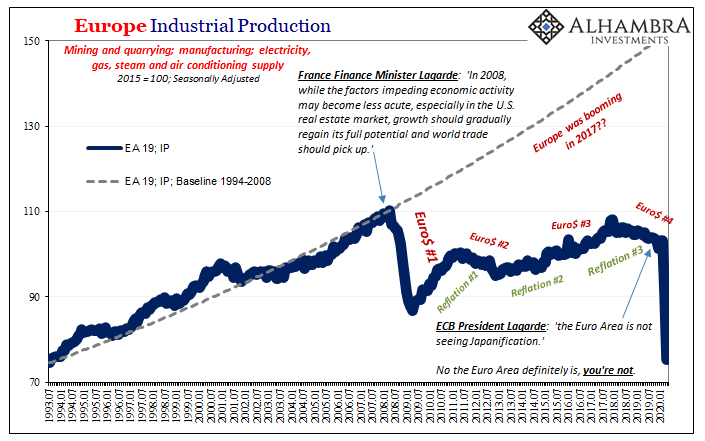

In Germany, formerly the European economy’s manufacturing engine, Industrial Production rebounded substantially two months ago but remains dwarfed by the contraction which preceded the comeback. Production levels are back to 2009 again, which has left them about a quarter less than they had been all the way back in November 2017.

That 30 months of decline matter as much if not more than the -23%.

Central bankers have done such a bang-up job post-GFC1 that Italian production is so low even on the rebound you’d probably have to go back to the first half of the 20th century to find comparable levels. Thus, what help to the overall economy even as things move back toward normal?

In short, as good as it may seem in some cases in some places, it is beginning to look like a very long road ahead. Again, a big part of the reason is that Europe, like the rest of the world, has been on this same road for a very long time already. V-shaped recoveries just don’t happen, no exceptions.

The Europeans are normalized instead to seeing “L’s” while hearing about future tense booms. Why would this time be any different? More zeroes on the same style of QE?

You get the picture. And so do European Economists, for once. Despite Italy’s plus 25 percent in retail trade, as well as all the other huge monthly positives, the EU once again downgrades its forecasts. Deeper hole this year, slightly lower rebound next year. Combined, still the same lack of recovery, only becoming more recognizable that way.

The European Commission said Tuesday that it expects the EU economy to shrink 8.3% in 2020, considerably worse than the 7.4% slump predicted two months ago. Growth next year is expected to be “slightly less robust” than previously thought, with GDP seen expanding by 5.8%.

And the next forecast will be downgraded, followed by the one after that and the one after that. Before you know it, the slightly V-ish forecasts of today will be near full L’s maybe by next month. Weak economies just don’t get back up when they are hit. While every central banker talked about how strong the world was, globally synchronized growth and all that, there was nothing behind it; a total lie.

I’ve said all along “they” made three huge mistakes, each of them driven by trust in stochastic modeling. The first one, thinking the economy was in decent to good shape heading into this thing, may have been the most harmful of the trio. In Europe, we’re starting to see it in the data for May, which should be, and probably will end up, the best of all the months.

If this is the best…

Stay In Touch