It’s incredible, in a way, because right from the start he’s got everything on his side. There are the media write-ups which all say the exact same thing, calling this an exact science being practiced by the wisest, most considerate stewards. The legend we’ve been raised with. Lore and scholarship (I repeat myself). Most of all, everyone.

When everyone says it’s a very good thing that Jay Powell’s definitely a reckless money printer, our brains aren’t wired to readily believe everyone could be so wrong on both counts (that he is and that it’s good he is). This, of course, explains a whole lot of the darker side of human history.

What monetary policy consists of in this post-GFC2 environment is theoretically very simple – to use the great tools at the Fed’s disposal to ward off further damaging effects. This great toolkit does not include a printing press, rather because it doesn’t it has instead been stocked with all those things listed in the opening paragraph.

To that end, if you believe in the money magic then mainstream convention believes that will be sufficient to prevent a bad situation from becoming worse; maybe, given enough time, to easily get back to good again. If you think Jay Powell is supporting markets, then you sure as hell won’t sell your clients’ stocks and will probably buy more for as much as you can.

Businessowners who believe could hold out a little longer, keeping up staffing levels even though their gut instinct tells them something different. Consumers don’t hesitate to make that next purchase they don’t really need to make. The bigger the better, and the faster – inflation, you know.

Most of all, banks and credit investors need to take Jay Powell at his word – that even though it’s absolutely ridiculous to believe the Fed is in any real or rational sense supporting all sorts of risky markets by conducting bond purchases off a predetermined list put together months ago by a committee of bureaucrats, who cares? Lend freely in all corners of the economy while buying up all the junk bonds being offered.

That’s the whole toolkit.

If it works, if everyone buys in to the obvious buffoonery and it all goes perfectly, then maybe the economy will actually recover…sometime in 2023.

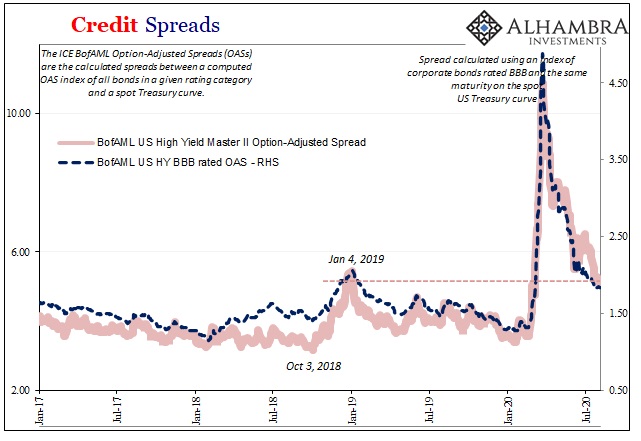

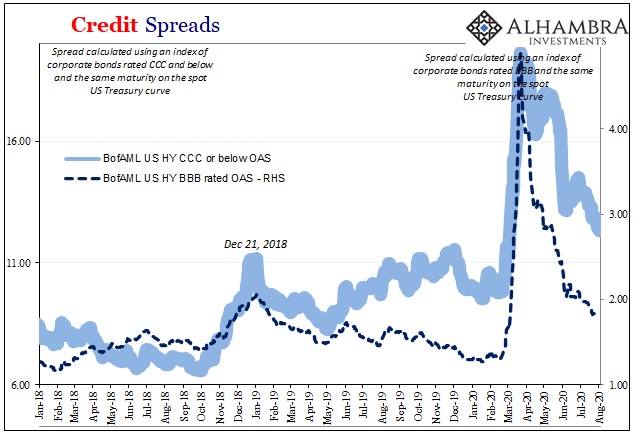

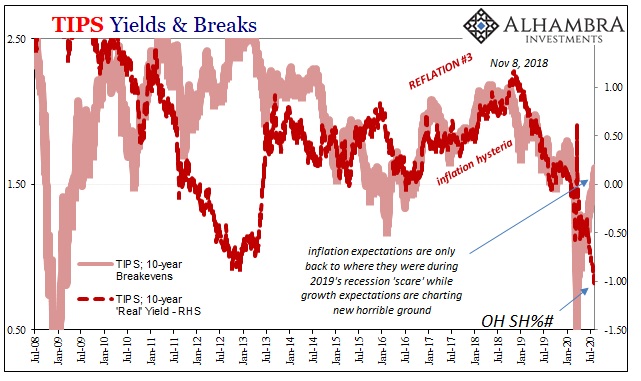

About that. Not everyone, you see, is buying in. On the contrary, many are quite obviously opting out. Start with credit markets, the junk that nearly broke the system back in March.

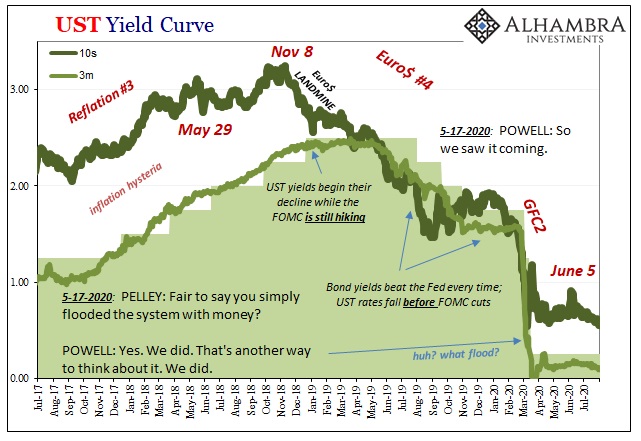

After that immense spasm (collateral bottleneck that even though it actually happened hardly anyone realizes what it truly was), a great deal of empathetic effort has been officially expended to get credit spreads back down to their starting point. While spreads have come down by a lot, it’s now August and they are still elevated equal to the peak of 2018’s very troubling eurodollar landmine.

Like the dollar, suspiciously still high.

The riskier the asset class, the more elevated. Underneath, volumes have come in just the way you’d figure given the stubbornness of spreads – not normal. The other kind of volume, however, that’s still on track to blow out:

“Default volume tallied $41.1 billion during the second quarter, exceeding the previous record of $39.5 billion set back in 2009. Frontier Communications and Chesapeake Energy made up nearly half that total. Overall, telecommunications and energy accounted for 70% of the total volume,” said Eric Rosenthal, Senior Director of Leveraged Finance.

Year-to-date volume is on track with Fitch’s 2020 base case forecast of 5-6 percent and an expected 7-8 percent base case default rate for 2021. This translates to a two-year cumulative base case default rate of about 15 percent.

And this right here in the junk bond/leveraged loan space is where Jay Powell is having his most success. It only gets worse moving onward.

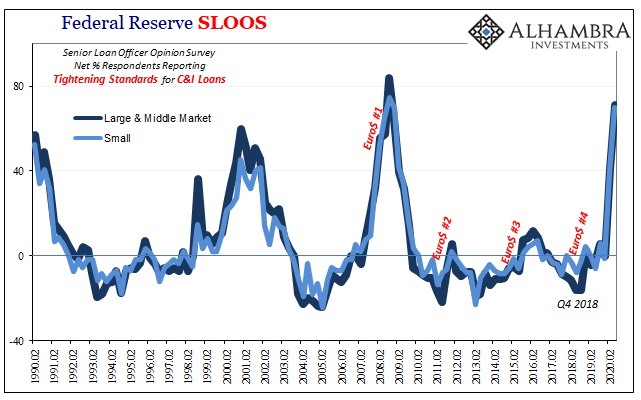

Bank lending.

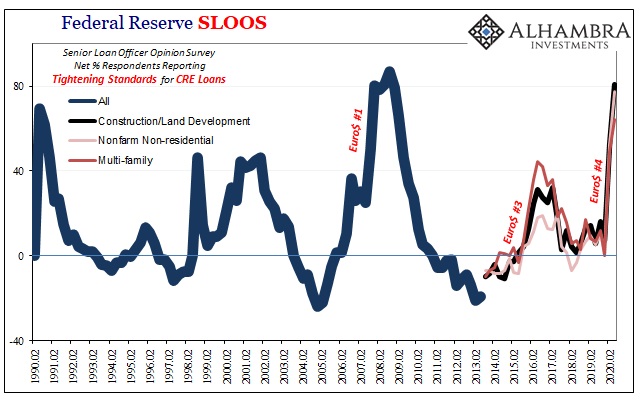

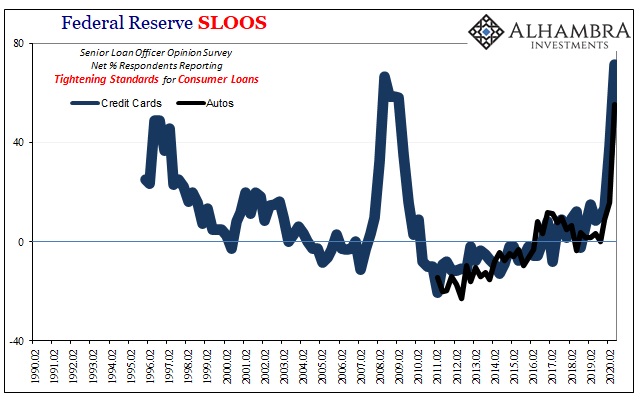

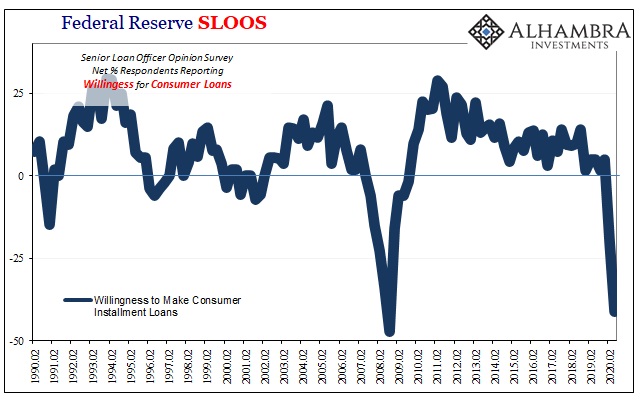

As my colleagues at Alhambra had pointed out to begin this week, the Federal Reserve’s very own Senior Loan Officer Opinion Survey (SLOOS) for the third quarter conducted during the month of July – July! – was on par with the fourth quarter of 2008. The very worst in the series’ history.

Powell has told the banking system over and over, and the financial media has reinforced this legendary message time and again, don’t worry about a thing; the magic money man has this recovery issue completely covered front to back. After all, he saw it coming the whole way.

The banking system, however, has told Powell, in no uncertain terms, to stick his happy words where the sun don’t shine. Bank lending standards have been seriously tightened across the entire system and in every single loan category; commercial loans, commercial real estate loans (CRE), residential mortgage loans (not shown here), and consumer credit loans.

In that last loan bucket, especially revolving credit, banks have told the Fed, again, in July with the labor market purportedly on fire, that not only are their standards much tighter they don’t even want to lend to the fewer remaining consumers who might qualify for them.

The July 2020 lending environment was not supposed to have been equivalent only with October 2008. Not after the biblical “flood of liquidity” and the mountainous market support to each and every one that exists.

As Joe Calhoun has pointed out, even if the government offers to guarantee loans (as some have surmised) what good will that do? No bank will knowingly originate and then carry a bad loan simply because some desperate politician or central banker claims they will stand behind it at some point (do people really not remember the part of 2008 having to do with the GSE’s?). Default is not the only headache and potential drawback from lending activities (NPL’s carried on an institution’s books can be just as bad).

In other words, a loan guarantee might convince banks and financial firms to continue to hold worthless paper they’ve been holding rather than selling it off at fire sale prices (and, again, that’s debatable), but it’s definitely not going to convince a bank to make a new loan that under any other circumstance it would avoid at all costs. On the other hand, it might end up making things worse given how banks might read the overall economic and lending environment which would’ve so alarmed otherwise disinterested politicians.

What the Fed’s toolkit lacks is effective money in it, but more than that it’s terribly short on reality and rational thinking. The bucket’s been leaking for a long time, and sprung a big new one five months ago. You don’t fix the problem by trying to fool everyone into believing you’re pouring water back in that you don’t even have. And even if you could put some water back into it, what good would that do?

The bucket is still leaking, at times gushing.

![]()

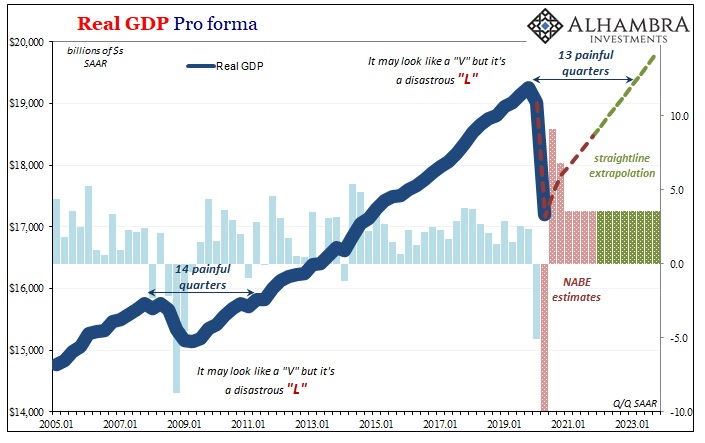

There are second and third order effects evident in a variety of data already in hand. The idea that the economy was going to skate through all this with a perfectly shaped “V” was impossible right from the start. And it was a long shot for the reopening rebound to come close to approximating that lettered shape.

Pro-cyclicality showing up here and all over will mean further depressing the upturn more than it’s already been squeezed, and more than that, like 2009 and after, keeping up these negative pressures for a prolonged period. A future even more filled with “L’s.”

Jack had a better chance with his beans than Jay with seemingly everything on his side. Well, nothing really useful, but still almost everything.

Stay In Touch