Who would’ve ever guessed? Jay Powell flooded the world with dollars, “overseas” swaps and all, but more and more you get the impression he doesn’t really know what he’s doing. The Fed Chairman, of course, is never alone when it comes to these things. He’s plenty of company.

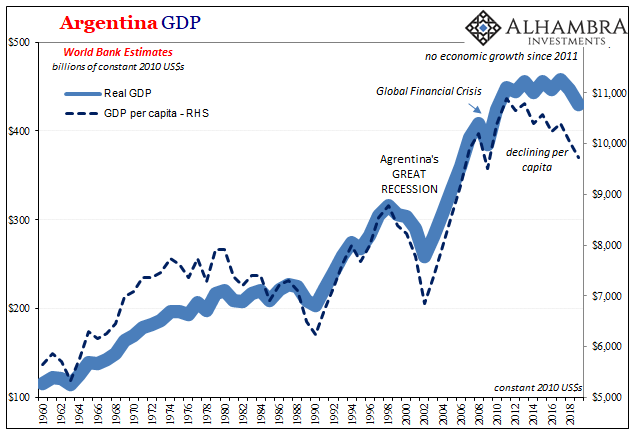

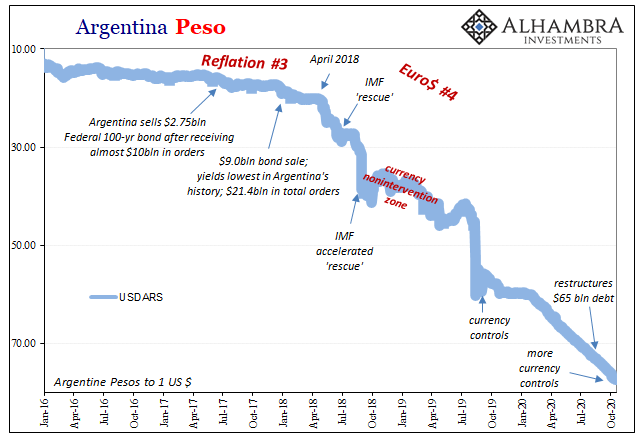

Recall, for a moment, how the IMF in June 2018 “rescued” Argentina. Big, big deal. Biggest bailout in IMF history. Previously, the country had binged – hard – in Eurobonds at a time when globally synchronized growth had been somehow taken seriously because of people like Jay Powell (specifically his immediate predecessor).

The country went from a 2.4x oversubscribed Eurobond at historically low yields (January 2018) to the biggest IMF action ever (June 2018) in the space of five months. Five months.

What had changed in that small amount of time? What monumental shift could have flipped such a switch? Trade wars between the US and China, right?

It’s easy to believe that it was something specific to Argentina, but it’s obvious this was never the case.

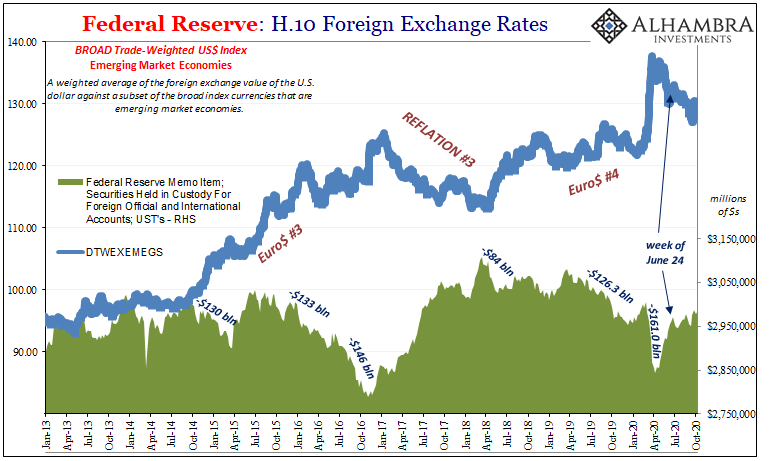

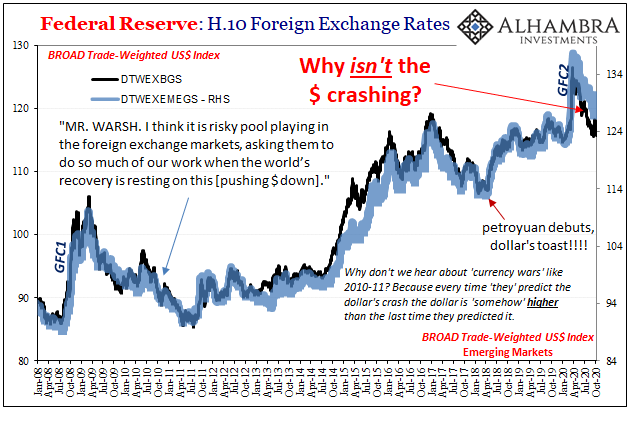

April 2018 is when the dollar surged higher (despite the petroyuan’s heavily-promoted introduction). In everything that has happened in the two and a half years since, we still write about this one little country in South America because it is the embodiment of all that’s wrong with conventional dollar theories. Or conventional theories about the dollar.

Or conventions thinking backward about what is this dollar and its true role as a reserve currency regime.

So, IMF rescue a couple years ago plus Jay Powell’s global dollar flood throughout the middle part of this year equals…not what it was supposed to. Instead this (thanks T. Tateo):

Like thousands of companies, Guerrini Neumáticos is unable to import goods because the country’s central bank is running out of dollars to conduct basic foreign exchange transactions.

I know, you’re just as shocked as I am (/sarcasm) Argentina’s central bank is running out of sufficient dollars just to carry on with the absolutely bare minimums of a functioning economy.

In recent months, the country has negotiated debt restructuring on about $65 billion of its external (Eurobond) debts. Like others in its neighborhood, de facto default didn’t really accomplish much except buy a little temporary breathing room – which, yet again, proves to be far too temporary.

That’s really the major issue in all of this; from the IMF to the Fed. Forget the technical details or the complicated ways in which these things are meant to work (but never do). The big picture is really pretty simple.

The IMF’s rescues like Jay’s fairy tale flood are designed for one purpose. They are a way, in theory, for a bank, system, or country to buy itself time. To grab some official dollar liquidity in order to restructure (via the IMF), or to back off the eurodollar sharks (through the positive sentiment from fake money printing), carving out some badly needed space to get everything back in order.

In other words, the world’s entire official sector continues on the belief that these problems are each country or financial institution. Buying time would make sense in that case. They don’t seem able to comprehend how the actual issue resides in the global dollar system itself. Therefore, chronic rather than temporary which means buying time with these fake floods and ridiculous rescues only squander it.

By the time whatever country or authority gets to the other side, there is no other side. It’s the same thing, systemic shortage, as when the whole thing got started. And that’s why, for entities like Argentina (or so many others) the slide into disaster never leads to emerging from out of it.

See for yourself:

One day you’re the darling of the Eurobond world and seemingly the next it’s a nightmare from which you just can’t escape – even when all the “right” people and places throw you what they claim is the best lifeline ever conceived and constructed.

Trade wars didn’t do this, just as the IMF’s rescue(s) were never going to fix it; nor Jay Powell’s lying about dollar floods and overseas liquidity. Global dollar shortage goes way beyond the conventional imagination first, therefore all its (meager) technical capabilities.

The one reason why it’s all make believe and puppet shows: the Federal Reserve is not a central bank. Sorry, it’s just not. We’re taught and made to think that it is; that the Fed through its Open Market Desk is in charge, even, of the whole monetary system. The dollar is backed by it, supposedly.

In reviewing this, a few things should stand out. First, how the Federal Reserve is not a dollar central bank, or a central bank in charge of the dollar monetary system. That’s what we are led to believe the institution does, take direct care of dollars broadly speaking (using bank reserves). Instead, the Fed is nothing more than a domestic bank authority whose actual authority ends at the US border.

But it’s not just that its authority ends at the border, the entire official understanding of dollars and money does, too. No small thing. This despite the fact, as I chronicled in good detail in the article above, what goes on outside the US in dollars is bigger, more relevant, and therefore the primary means of setting the global direction. US, like Argentina, included.

The only difference is one of degree, not type.

The gross eurodollar size was in 1988 a third greater than the entire [domestic] M2 stock would be three years afterward, while its net size was closing in on two-thirds of it. And this was three decades ago.

They don’t care; they don’t factor this at all. In fact, central bankers and Economists struggle even to explain the “good” times like the so-called Great “Moderation” because in the mainstream, official view there are only domestic banks to worry about. And the only time anyone worried about domestic banks was a dozen years ago.

Global dollars, they might exist, and a few Fed researchers have occasionally, infrequently written about them, but that’s as far as it has ever gone. Or ever goes in orthodox thinking.

The results show. It’s all a puppet show. There’s no inflation puzzle, nor is there some huge global mystery about why everything changed around 2008 (August 9, 2007, specifically).

The IMF mega-bailed out Argentina. The Fed flooded 2020. And yet, “somehow” this country is out of dollars again. It’s really easy to think that it’s just Argentina being Argentina, but that’s just what the IMF and Jay Powell think. Look where it’s got them – and us.

They are hardly alone.

It’s the eurodollar’s world. We’re all just trying to live in it as best we can, and we’re forced to do so because people at the IMF, like everyone at the Fed, they really have no idea what they’re doing. They’re not idiots; rather, they’re stuck in a 1960’s view of the 1930’s.

The reason the modern central bank like the Federal Reserve isn’t central is largely because it’s not really a central bank at all.

Stay In Touch