———WHERE———

AlhambraTube: https://bit.ly/2Xp3roy

Apple: https://apple.co/3czMcWN

iHeart: https://ihr.fm/31jq7cI

Castro: https://bit.ly/30DMYza

TuneIn: http://tun.in/pjT2Z

Google: https://bit.ly/3e2Z48M

Spotify: https://spoti.fi/3arP8mY

Breaker: https://bit.ly/2CpHAFO

Castbox: https://bit.ly/3fJR5xQ

Podbean: https://bit.ly/2QpaDgh

Stitcher: https://bit.ly/2C1M1GB

Overcast: https://bit.ly/2YyDsLa

PocketCast: https://pca.st/encarkdt

SoundCloud: https://bit.ly/3l0yFfK

PodcastAddict: https://bit.ly/2V39Xjr

———WHO———

Twitter: https://twitter.com/

Art: https://davidparkins.com/

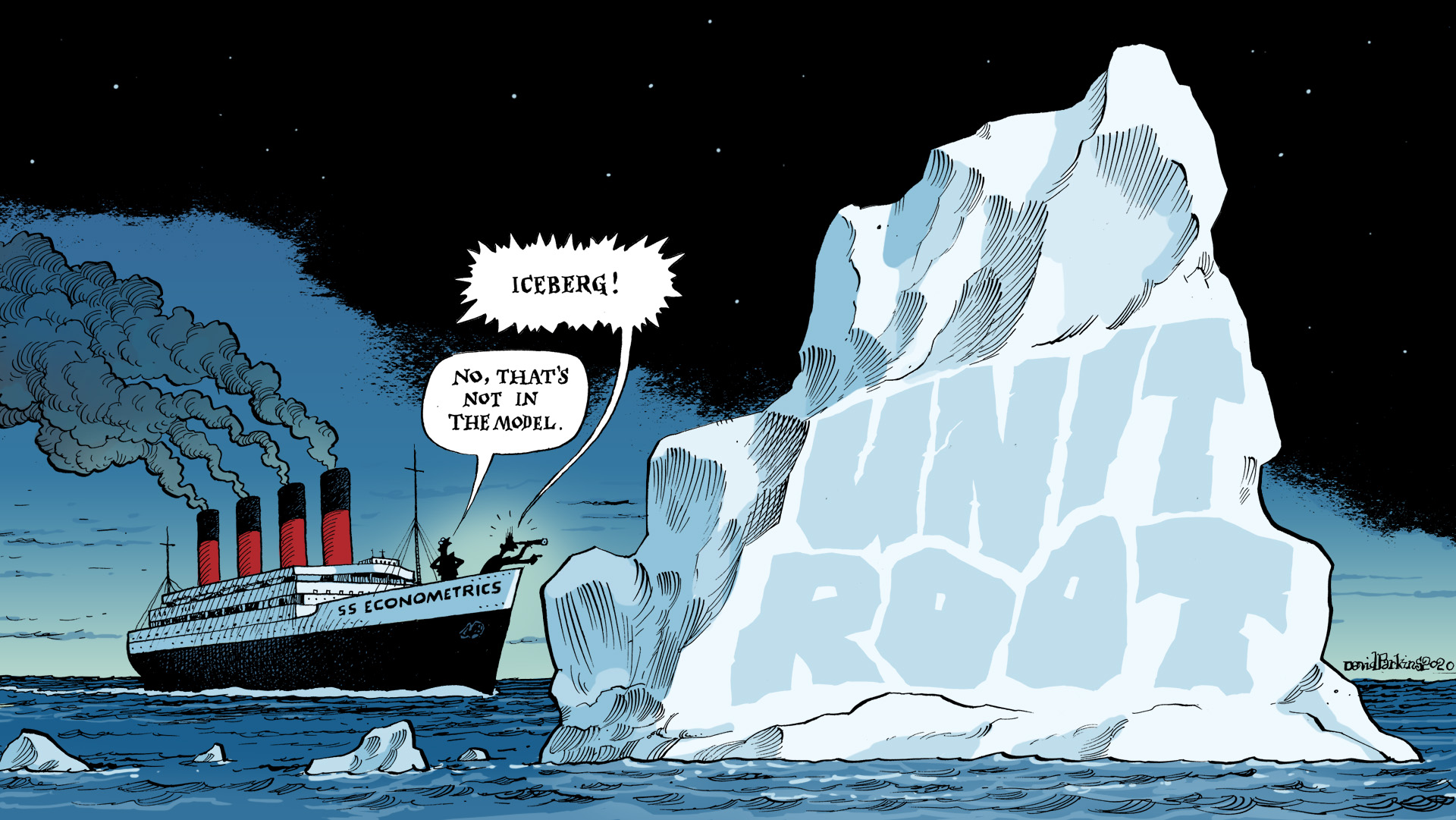

32.2 Self-Reinforcing Delusion of Econometric Models

The world is complex. Too complex to model. Assumptions must be made. Is the exclusion of permanent shocks to the economy a reasonable one? Rational? Plausible? Yet econometricians — with their hands on the wheel — say it is. That iceberg dead ahead? Not in the model.

[Emil’s Summary] The bread of this podcast hotdog features Jeff Snider putting into context how far behind the times monetary authorities are, and that all may not be as it seems with the appreciating Chinese currency. But the middle, the wiener if you will, is about the unit root. But please! Before you throw your device across the room in disgust rather than listen to yet another podcast about monomial equations and non-stationary processes realize that it’s all about econometricians assuming economies do not suffer permanent shocks. The assumption that an economy must experience a recession AND a recovery.

A 1993 paper by Milton Friedman averred the data showed this is how economies operated, and indeed they did — in the post-WW2 experience. Friedman referenced an earlier work of his, from 1964, with data that stretched over a longer period that ALSO showed this. And indeed, the 1879 to 1961 period does, as long as you exclude the war cycles and 1945 to 1949 because, as Friedman put it “of their special characteristics.” So, if your podcaster understands this correctly, if you exclude permanent shocks and data discontinuity then one is welcome to assume no permanent shocks.

Now, your podcaster is admittedly missing something here. For one, he’s missing econometricians’ razor-sharp intelligence. Second, he hasn’t won a Nobel in economics – not yet at least. The cost of this lacuna is that shoelaces give him trouble – all his trainers and loafers have Velcro. Simultaneous gum chewing and walking results in emergency trips to the dentist. And hot dogs are eaten with the bun in one hand and dog in the other. But the benefit of not having a towering intelligence is not falling prey to hubris. In believing intricate mathematics model out permanent shocks. In believing that it can go back to the way it was. The year 2008 was a permanent break. Like 1914. Like 1929. Like 1945.

———WHEN———

00:05 What is Milton Friedman’s “Plucking Model”?

05:30 Milton Friedman takes to task economists of the 1930s, 40s and 50s for ignoring money.

07:17 Why is math VERY important to economics? What is econometrics? What is a “unit root”?

09:53 What happens to a trending economic data series if it encounters a “unit root”?

11:52 Why would econometricians assume the economy doesn’t experience permanent shocks?

———WHAT———

The Unit Root of the Missing Monetary Monomial: https://bit.ly/37zvVBV

Milton Friedman’s 1964 The Monetary Studies of the National Bureau: https://bit.ly/3dQquQ2

Milton Friedman’s 1993 “The Plucking Model of Business Fluctuations Revisited”: https://bit.ly/3dQ1OY3

Alhambra Investments Blog: https://bit.ly/2VIC2wW

RealClear Markets Essays: https://bit.ly/38tL5a7

Stay In Touch