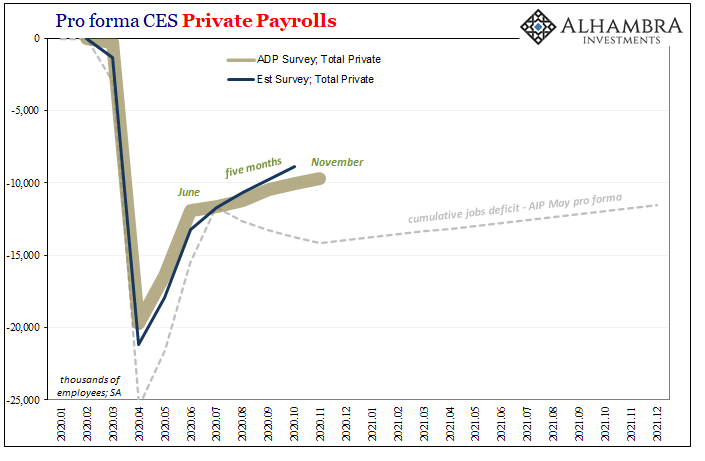

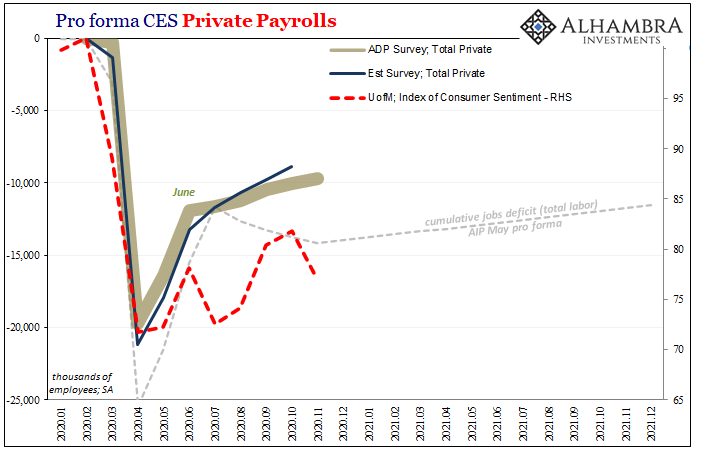

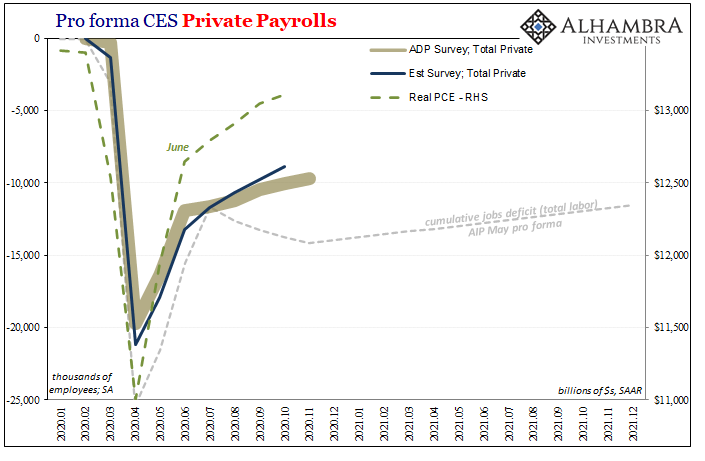

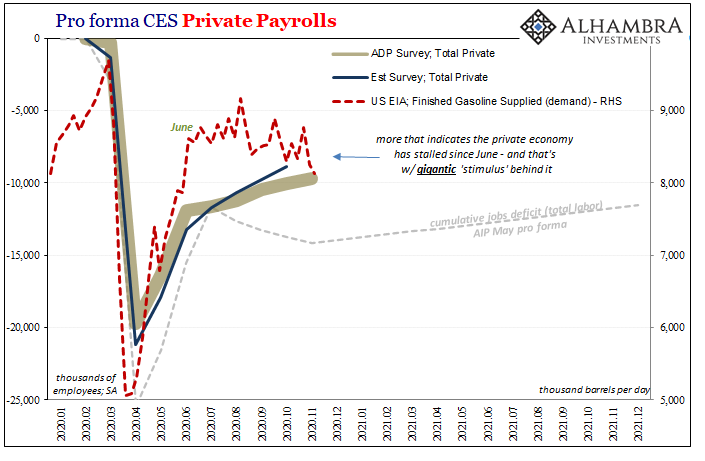

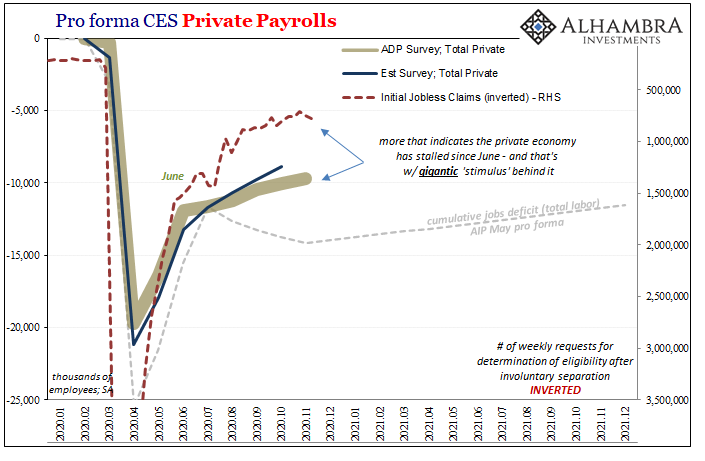

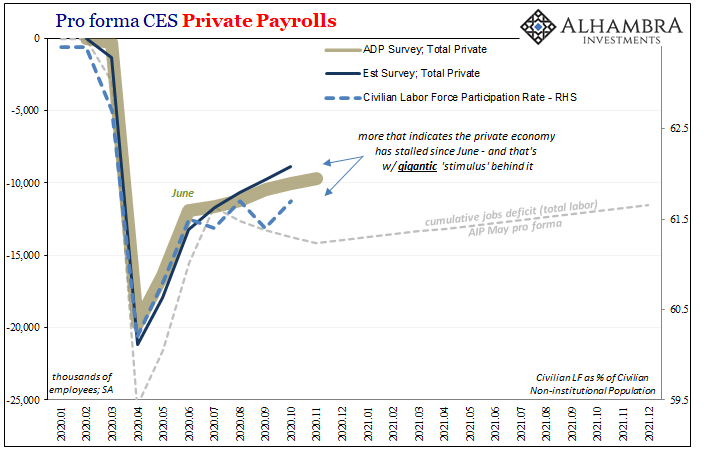

ADP reports today that, for the fifth consecutive month, the labor market recovery everyone had hoped for has instead been transformed into something else entirely. According to the firm, private payrolls expanded by just 307,000 in November 2020 from October. That’s the slowest pace since July, and, most important of all, leaves the private US economy near 10 million short of its February departure point.

At this rate, it’ll take another two and a half years just to close this original gap – assuming the rebound doesn’t decelerate any more over that timeframe – and in the process opening up another huge deficit related to the nearly 4 million in payroll expansion which won’t happen during that extended period of time.

Needless to write, I’ll write it anyway, this is kind of a big deal.

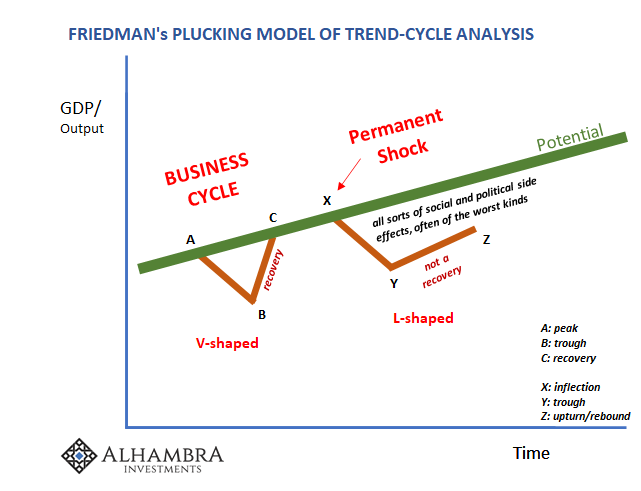

This has brought up a curious if ultimately trivial twist in the ongoing attempt to make sense of the economy and its related recovery alphabet. At first, when reopening was new and furious, the letter of choice was an unaltered “V”; straight down, then straight back up. If it was so easy to close an economy down, and it sure seemed easy, why wouldn’t it have been just as easy to get it back up to speed?

After all, huge doses of fiscal “stimulus” (or was it subsidies?) as well as the top echelon of Federal Reserve officials bragging to every media reporter how they’d rendered the biblical story of Noah tiny and pitiful when compared to the flood of digital dollars their handiwork had unleashed; the guaranteed inflationary and market-rimming ebullient currency orgy of yesteryear lore.

How could it not be “V?”

Well, it wasn’t; V is dead. And it wasn’t the ADP or any one data point or series which killed the dream. Rather, it’s been everything, everywhere. Summer slowdown is real, except now it’s December and the thing only drags on.

In response, almost something like a compromise. If the “V” is gone, and it is, then how about a “K?”

For this mutation, the recovery might not be so easy and perfect but mostly “V”-like…at least for those on top, the ascender mark on the right-side of the letter, enjoying the uptick thoroughly. And while we might feel bad and sorry for those lost in the depression of the “K’s” lower leg heading forever, it might seem for those stuck in it, downward, the media sells us on the pattern as, darn it, the “best that could be done.”

That is supposedly “K.”

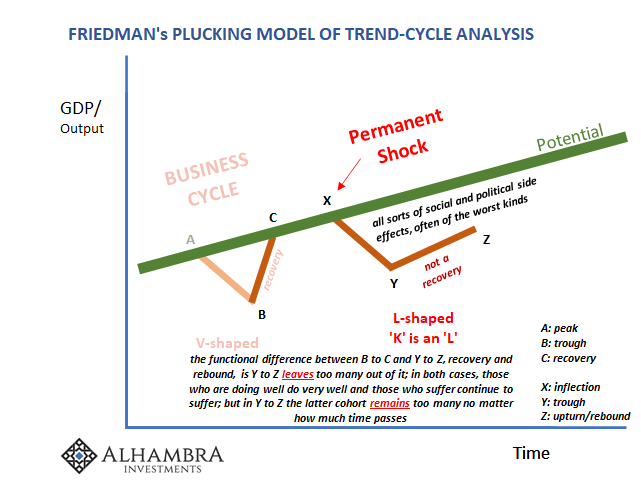

No. What’s going on here is rather simpler than all that. A “K”-shaped recovery is really an “L” rhetorically decorated in order to make these rationalizations seem somewhat plausible and less tragic.

It all starts with what seems to be confusion over what is, and is not, recovery – as if there ever could be various types of it. Words, after all, have meaning. In the economic context, the word recovery has a specific meaning and the reason it has a specific meaning is that this meaning conveys meaningful information beyond mere dictionary purposes.

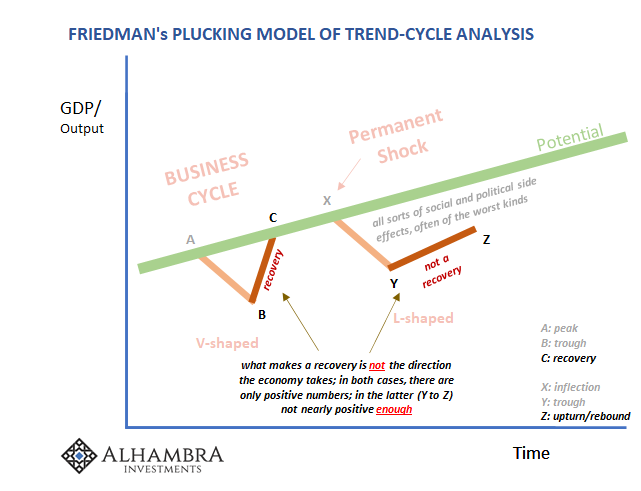

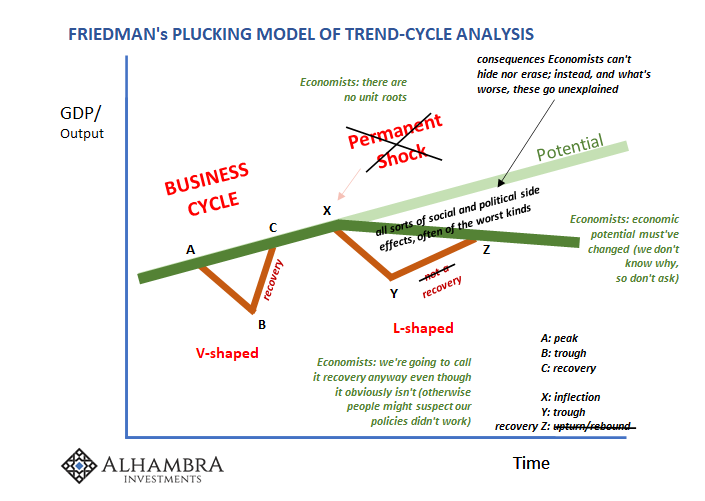

The first segment illustrated above, B to C, now that is a recovery and the only form of recovery by the term’s only applicable definition. Notice how it sure does resemble the letter “V.” For an economy experiencing the typical rigors of a normal business cycle, recovery means you end up where you would’ve been had you avoided experiencing a temporary deviation or setback (that’s what a recession means; temporary).

But if it ain’t really a “V”, it ain’t really a recovery. And that’s only where the problems begin.

What’s going on instead Y to Z may look and sound and feel somewhat like what happened B to C, but this second form is an altogether different thing. Categorically so. Yes, the economy is moving upward again, the economic accounts uniformly or near uniformly positive. Those, however, are the only superficial resemblances to recovery.

As are how the top echelon experiences conditions in either; those who are doing well continue to do well even during the worst contractions in history. What separates these “V’s” from the “L’s” is the size of the group left outside of basic economic performances when it all starts to come back up; especially jobs and labor. In the “V”, this group may start out large, as in 1981-82, but in relatively little time it shrinks right back down.

The “L” experience, by contrast, there also begins a huge number in this suffering cohort as the contraction hits X to Y, but then during the upturn Y to Z that number doesn’t improve nearly enough. By the definitions of mainstream “analysis”, that’s their “K” – which, again, is really nothing more than a derived “L.”

Too many stuck for suspiciously too long in the lower leg of the “K” are what give us this “L.”

The longer run consequences of this are not purely economic in nature, though that is where they are felt most readily even on-the-ground, closer to home. Lack of legitimate recovery and economic growth has always been associated with social and political upheaval. And, in many historical cases, the worst periods of them are those when few real answers are available to explain for their economic deficiencies.

In the 21st century, we like to think of ourselves and our “experts” as having conquered all such boundaries of ignorance; when the people of America, for example, faced the Long Depression of the 1870’s they didn’t know where it came from or why it seemed to just stick around and create misery for so long. Surely modern Economists would’ve filled in all the gaps by now?

Except, no. Not remotely. Instead, what happened is the embedded expectations for econometrics – that business cycles of the post-war economy (1945 to ~2000) were some new kind of different template from which it was assumed (by Economists) no economy would ever again deviate. This subjective interpretation was even hard-wired (no unit root) into the statistical models that dominate the discipline, therefore drive the public’s opinions on such matters.

But when confronted by a real-world set of outright contradictory evidence, drawn from allegedly different, far-flung economies all over the world, Economists refuse to rethink their post-war master. In the face of constant, uniform “L’s”, they reclassified Y to Z as “recovery” anyway. Changed its meaning entirely.

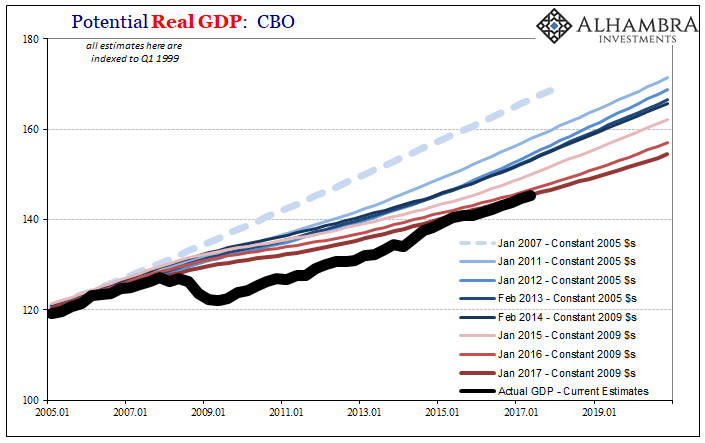

In order to pull off such a dastardly feat, all that was required was to further rewrite economic “potential” and to obscure when this modification needed to be introduced. In the real-world data, that has literally meant downward revisions in economic potential the world over, especially the United States, beginning, interestingly, right at 2008.

Who in the public would ever notice? Quite predictably, hardly anyone has.

Here’s the thing; while the average worker/consumer/employer/portfolio manager hasn’t noticed, they sure have understood at least on a personal level the increasingly grave level of dissatisfaction with how things apparently don’t work anymore. The economy has “recovered”, so sayeth the sage advice from the Ivory Towers, but it really hasn’t no matter how many times the pedigree-d few declare reality differently.

Instead, it only raises the temperature even more – just like the 1870’s, the 1830’s, and, if you prefer, the 1930’s. An economic condition that’s both “L” in overview and “K” in detail leaving too many on the outside looking in, and no one with answers for either side.

That was all post-2008. Here in 2020, we’ve now been set up do this all over again. Yep, another “L” being lined right up right in front of our eyes to add on (further subtract from?) to the prior “L” still causing inordinate suffering. Saying this is a “K” is only more lying window dressing.

In this case, unlike the 2008 case, Economists and their like are being more open about it – because they believe they can be. While they had no good answers for the first permanent shock of 2008 (come on, subprime mortgages!), this time, oh yes, it’s not our fault blame COVID!!!!

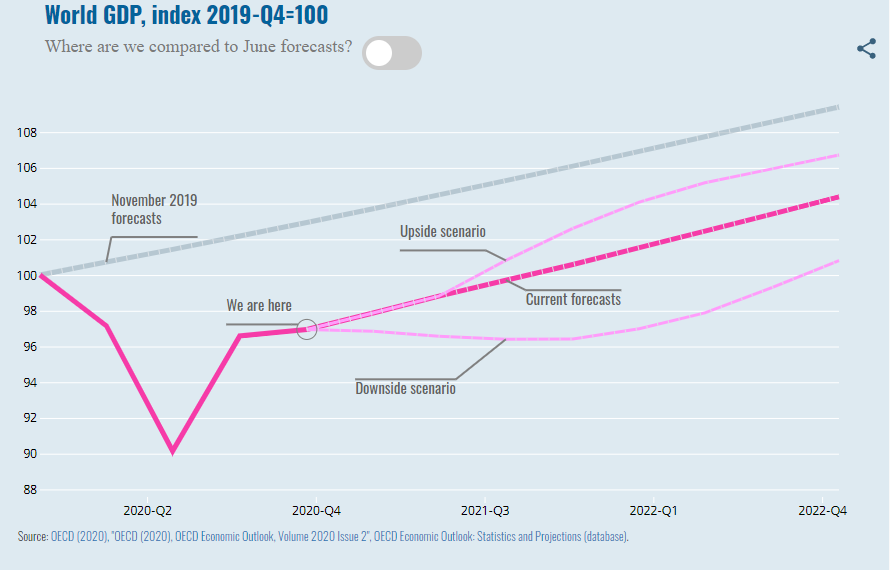

Whereas around 2010 and 2011 you never would’ve heard such honesty and openness as what I quoted yesterday from an outlet like the OECD, instead there was only ever “recovery is still happening” garbage, nowadays they aren’t quite hiding it in the same way. If you have any doubts about this “L” versus “K”, I’ll reproduce it again here (I couldn’t have written it any better):

Despite the huge policy band-aid, and even in an upside scenario, the pandemic will have damaged the socio-economic fabric of countries worldwide. Output is projected to remain around 5% below pre-crisis expectations in many countries in 2022, raising the spectre of substantial permanent costs from the pandemic. The most vulnerable will continue to suffer disproportionately. Smaller firms and entrepreneurs are more likely to go out of business. Many low wage earners have lost their jobs and are only covered by unemployment insurance, at best, with poor prospects of finding new jobs soon.

‘

The OECD’s Chief Economist wasn’t writing about specifically this ADP data, but he might as well have been (see below).

But what actually produces these “L’s?” That’s the fifty trillion-dollar question. As Henry George finally pieced together in 1879, depressions like this are provoked by an “impediment in the machinery of exchange.” A recession, on the other hand, practically any old shock can do that.

What could be so destructive that it could actually alter and detour the longer run economic course and do so across the entire face of Planet Earth; so thoroughly and repeatedly thwart what even the most astute of Economists (there are some, a few) had come to believe was a new paradigm of only ever mild business cycling?

Economists, obviously, this time are already blaming COVID as that impediment, but it’s no different than saying subprime mortgages were the inhibition responsible for the last one. To the point: it’s becoming indisputable that there have been two.

In both cases, as in all those prior depressions, the answer is in one sense much easier (because it’s always the same thing, as John Maynard Keynes observed) to identify. Wrecking the labor market, the Pièce De Résistance of any “L”, is the specialty impediment of the monetary system.

This explains both Jay Powell’s flood myth as well as why it was a myth and the consequences from it being no more relatable than a boring, badly-spun fairy tale. Not COVID, the slowdown, as we’re still documenting here, it hit over the summer.

We’re again violating the “prohibition” on unit roots, introducing serious and long-running impediments in the machinery of exchange, and have therefore been set once again on a course way, way short of recovery. Call it a “K” if you must, just don’t you dare call it hope (yes, that OECD cover above really made me mad; as it should make you furious, too).

Real hope, not the bland sloganeering we’ve been normalized to, the same which has rewritten the word recovery into something it so is not, true hope lies in recognizing these things all for what they are, the only thing they could ever be or have been. Some real science and evidence, for once, would be a great place to start.

A permanent shock really narrows the suspects down. A second permanent shock would, in an honest world, leave no doubt. Especially when just this thing was predicted years ago. We don’t live in an honest world; we’re told we live in an Economist’s world when in truth we inhabit the eurodollar’s increasingly restricted space.

But inflation…

Stay In Touch