They really got carried away, though in the context of that time there seemed any number of legitimate reasons for this. Gold investors were bidding up the precious metal like there was some kind of shortage, the price in dollars making a new record high (LBMA morning fix) on August 7. The way it was reported in the mainstream, this was more confirmation of Jay Powell’s flood of money printing making its way into every last corner of the financial world driving gold bugs nuts in the process (as intended).

Nah.

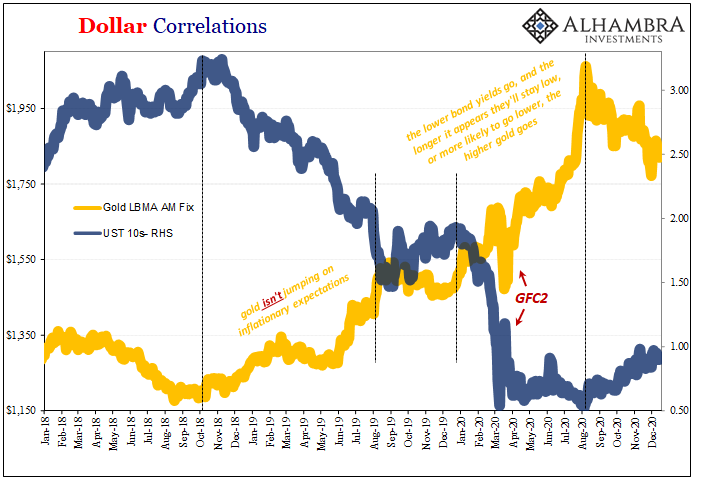

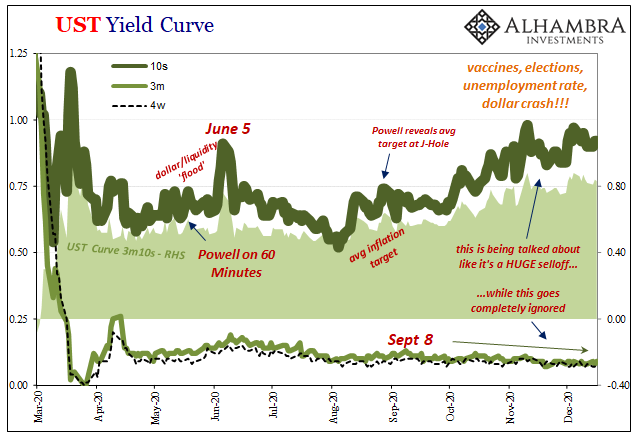

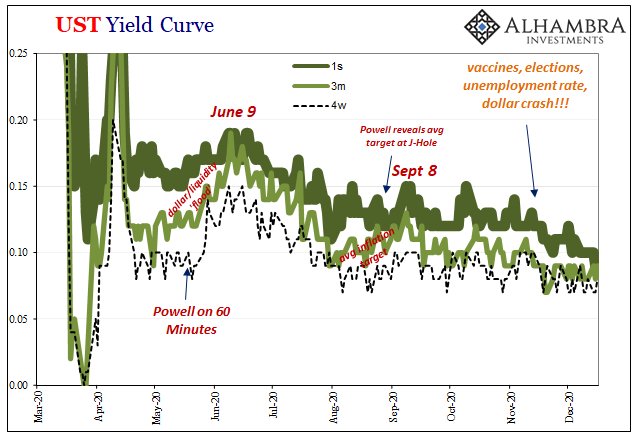

A few days before all that, the 10-year US Treasury yield had sunk back down near its crisis extremes. On August 4, the note finished trading to rate just 52 bps, less than the previous record low close set March 9.

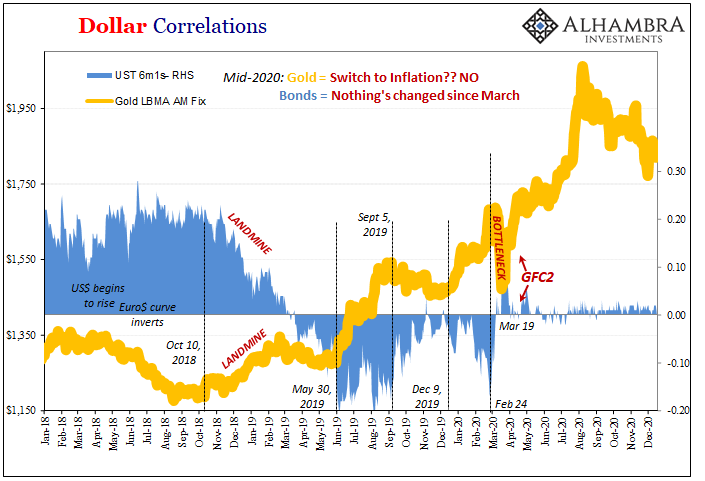

Since early August, gold and the long end of the yield curve (as well as the shape of the short end) have merely continued their close coincidence of inverse behavior. It just isn’t a coincidence, of course, the mainstream view of gold is almost all backward and has been for a very, very long time (like everything else when it comes to money, finance, and economy).

Dating back more than two years now, gold prices have been pushed higher by deflationary expectations like those embedded within lower and lower risk-free rates represented in the longer UST’s. Gross financial distress of the global dollar shortage kind, totally the opposite of the inflationary flood we keep hearing about.

Gold is actually rising instead on concerns that central banks and governments around the world will fail in their collective efforts to support already deflationary economies…As always, money-less monetary policy comes down to ridiculous, easily disproved deception. Other than that, there’s nothing else in the official central banker toolkit. Realizing this, you might then understand exactly why gold and bonds are being bid concurrently in this way.

Now that gold prices are falling, you hear very little about them – in favor of the increasingly ridiculous BOND ROUT!!!! resurrected by this Inflation Hysteria #2 which suddenly can’t include rising gold prices.

Curious.

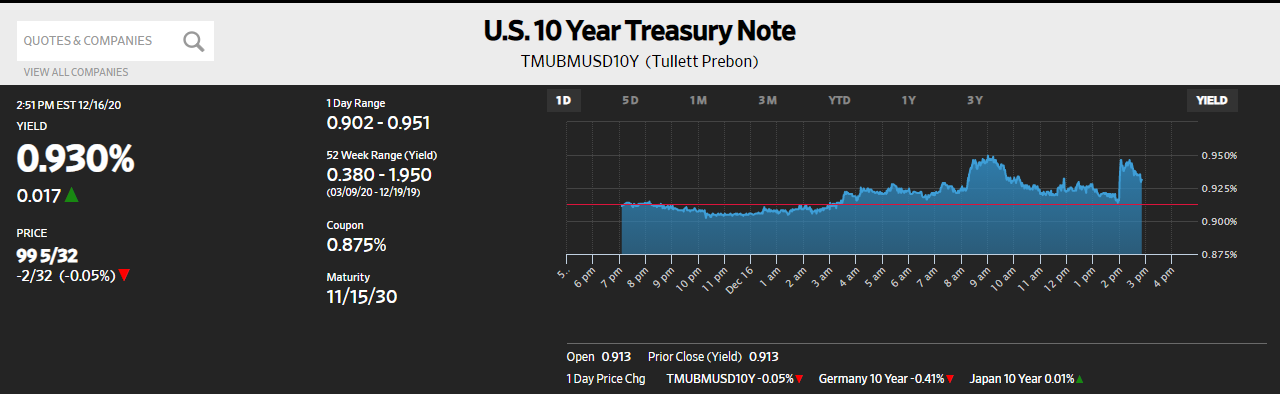

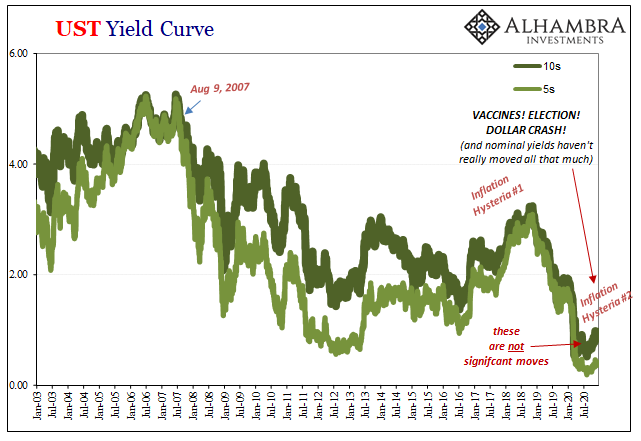

Even trading in Treasuries is about as un-inflationary as you might imagine. For all that’s supposedly going right right now, how is that longer-term rates haven’t really budged? Unbelievably tiny move. The 10-year note, for all this fuss and bother of late, vaccines and huge government stipends, it is all of 40 bps off its record close while basically the same as when Pfizer made its stunning vaccine public.

This barely qualifies as a market fluctuation, let alone a categorical shift in the Federal Reserve’s desperation direction.

Not for trying, mind you. While gold investors play off bond yields, speculative bond investors keep pounding Powell for Powell. There hasn’t been a single significant nugget of news the past few months that these shorts – betting on Jay getting something right for once – haven’t shorted more. And it hasn’t mattered what that news actually is.

Today, for example, there was two of these only hours apart (below)! First, earlier on in opening trading when “news” reached the pits of the federal government inching closer to a spending deal that everyone in the world already knows is going to get done at some point.

And then, more ridiculous still, another selloff attempt when the FOMC statement was announced and proclaimed not dovish enough. Or was it too dovish? In the middle somewhere? Good news was bad news? Or was this bad news which can be good news?

Doesn’t matter, because the shorts short on every bit of news regardless.

In reality, gold prices haven’t fallen all the much off their highs because Treasury yields haven’t come up much off their lows and seem to ably weather these storms of shorting whenever they inevitably show up. So much big stuff supposedly in the news, never much in the markets.

On the contrary, if there have been any serious developments they’re elsewhere – such as in bills. While attention gets drawn purposefully to make mountains out of those tiniest molehills out the longer end, where it really counts (where it really counted in March) there’s been increasing demand for the same collateral-center instruments. But you never hear a single thing about this:

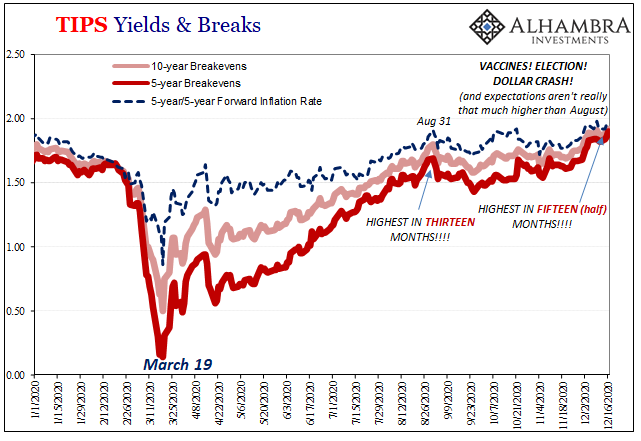

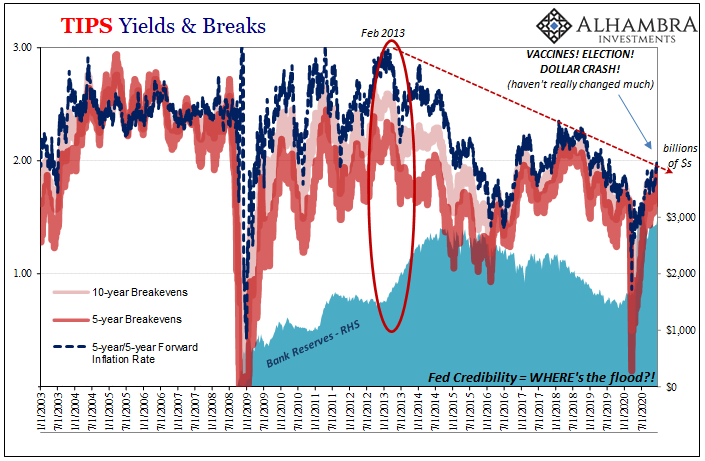

Despite this ongoing deflationary caution, because of the ongoing collateral concerns behind it, even inflation expectations (TIPS) have been similarly subdued. Like the small backup in nominal yields, inflation breakevens and rates have been touted and thrown around like some bullet-proof proof positive that the Fed’s finally hit its magic money number.

The inflation genie’s out of the bottle!

Typically, these are done by comparing inflation expectations today with inflation expectations earlier in the year, hoping no one notices the missing context.

That context goes something like this: inflation breakevens right now, moved upward a little bit on nothing more than oil prices modestly hoping for vaccines to deliver an immediate end to the nightmare, still expectations are about where they were in the middle of last year or August 2015.

Yeah, not exactly a fiery infernos of out-of-control monetary excess; on the contrary, August 2015, for one thing, that had meant CNY and Wall Street flash crash, the same things which add up to dollar shortages and more getting stuck in the other direction.

And that’s what this broader survey of markets actually indicates. Not just stubbornly high gold, persistently low nominals, inflation expectations that haven’t surged despite all the awesomeness piled onto WTI, just about anything else including interest rate swaps aren’t anywhere close to the hysteria.

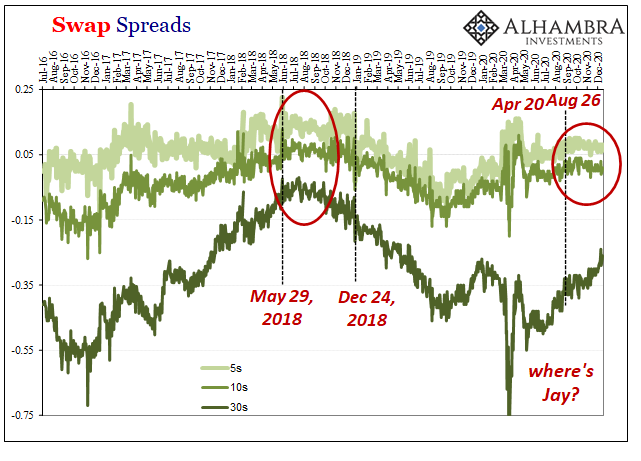

In fact, in the middle of the curve swap spreads have once more begun what sure looks like an ominous descent of the non-inflation kind. And interest rate swaps here is right where inflation – if it was real – would be showing up. Trillions in “fixed” income and balance sheet factors globally which, if the Fed had done anything close to what’s being said, you better believe these would absolutely require, nay demand, piling up in swaps (decompressing spreads).

The most you can say of any of these things is that right now it isn’t as bad as March/April. That’s not inflationary; it’s the lowest of potential standards possible. A small relative change that’s, par for the mainstream course, being blown way out of proportion.

Because those proportions aren’t ever included.

More to the point, there’s enough elsewhere to explain why this is; why the best that can be said is thankfully there’s no third GFC right now at this moment. However, that doesn’t mean these same deflationary and potentially textbook deflationary problems have gone away, they’ve just gone away from the media and mainstream commentary over-eager to put all this behind us.

Got to get back to loving the technocracy again. After the Bernanke debacle and the decade-plus spent trying to clean that up, and only sweeping it under the rug, the Federal Reserve can’t possibly fail this big, can it?

Haruhiko Kuroda would like a word.

Stay In Touch