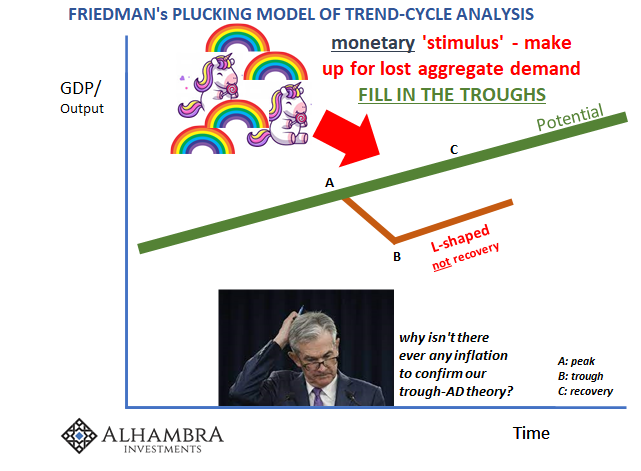

Is there a charmed fiscal number that unlocks the inflationary promised-land? Central bank Economists have spent more than a decade in the West, two in Japan, desperately seeking the magic number QE. Though their own research is substantial and conclusive that LSAP’s like QE don’t work, and never have, officials conclude instead that it always comes up short because it wasn’t ever enough (or left alone long enough).

This isn’t really about consumer prices one way or the other. Inflation, rather, is the signal that economic health has been established and done so in a way that reflects a strong likelihood of being sustained.

Shoved aside by COVID overreactions, though central banks weren’t out of the game (QE’s did get massively upsized), over the last year they have been and continue to be overshadowed by fiscal authorities. Particularly in the US and Europe, monetary policy is so last decade. The twenties, at least their first year, these belong to government treasuries. That’s what they’re saying, anyway (stimulus-phoria).

But what did all that prior government aid, spending, stipends, grants, loans, and tax cuts accomplish? By the count of real GDP, as discussed yesterday, a whole lot of the familiar “jobs saved.” Maybe.

It’s hard to imagine, though, how it might have been worse. As of the end of 2020, the employment deficit remained greater than at any time since the Great Depression. Not just in terms of the 10 million jobs which disappeared and have yet to come back, but now another 1.6 million payrolls that would’ve happened if last year didn’t happen.

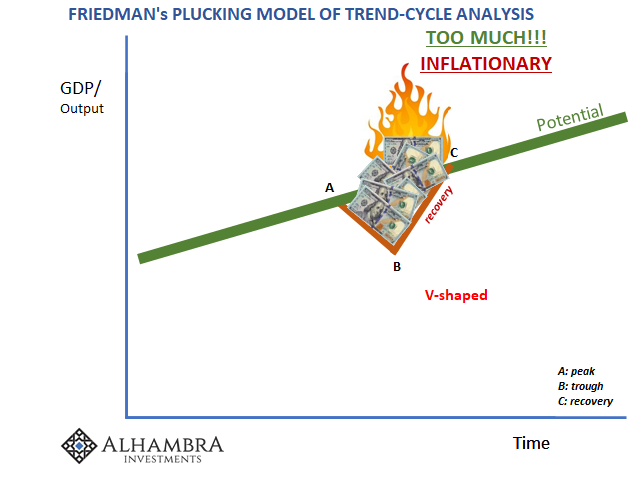

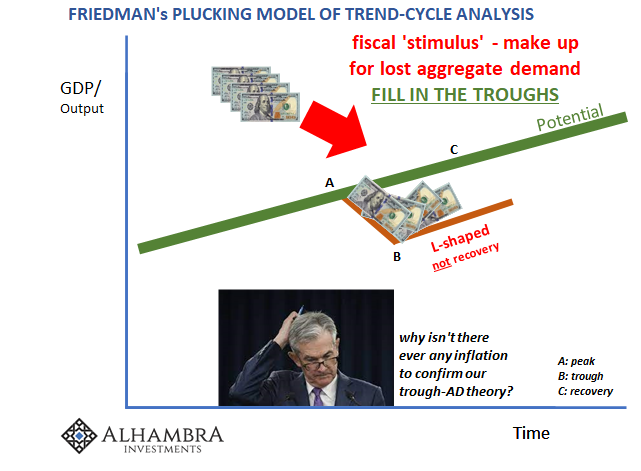

For fiscal authorities, that was the point of much if not most of the spent “stimulus.” If the private economy suffered so massively, then Uncle Sam would fill in the gap; fill in the trough – and risk going overboard. Thus, it has to be absolutely sickening to fiscal authorities doling out thirteen-digit numbers only to find how consumer spending continues to track private income regardless of any level of aid.

No magic number yet achieved.

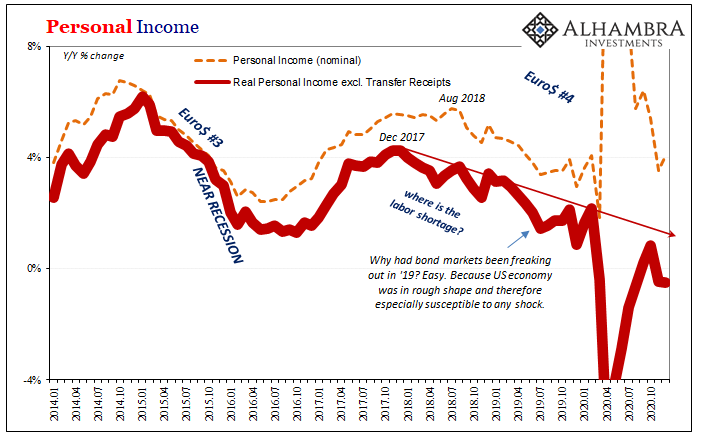

It is yet another abject lesson in the permanent income hypothesis, pretty well proved by this point. If there were any remaining doubts, according to the BEA today in follow-up data, private income (excluding transfers) had declined for two straight months to finish last year while still substantially short of the prior peak. Making for an especially awful Christmas season, these figures completely corroborated and consistent with the employment (and unemployment) data entering 2021 in reverse.

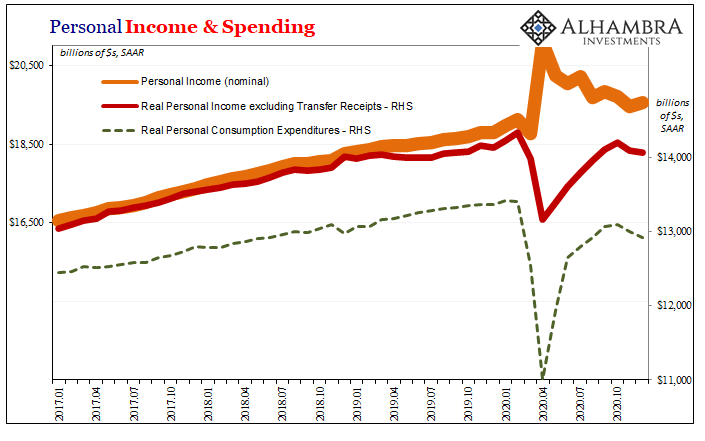

And personal spending, in real terms, has likewise declined in those same months. American consumers, as rightfully fearful and uncertain workers, follow the lessened track of permanent income rather than conveying their wallets toward Treasury’s groping for a magic number.

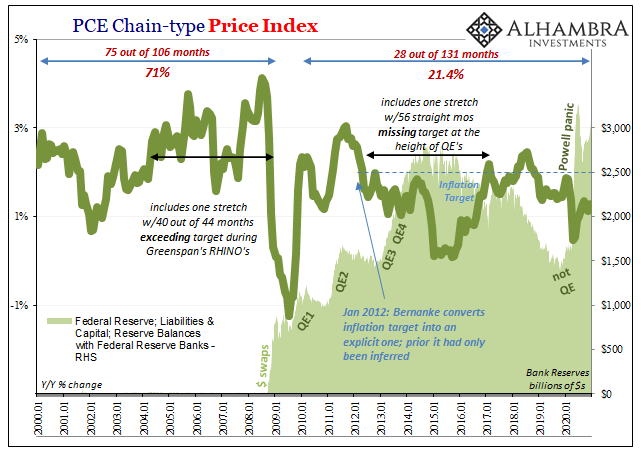

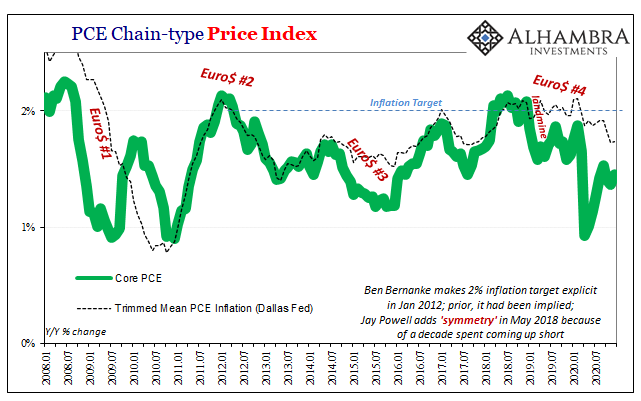

Therefore, very briefly, little more needs to be said at this stage, there’s no inflation to be discovered, no monetary ember yet burning brightly to convey the fruits of such magic. Only coldness even after ten months of “massive” “money printing”, wartime levels of government expenditures and deficits, in the end the Fed’s preferred consumer price indications haven’t budged; the headline PCE Deflator increased just 1.28% in December 2020 when compared to December 2019, a very gentle acceleration as oil became less of a drag (vaccine-phoria), while the core rate no more than 1.45% and like the CPI among the lowest rates.

Even the Dallas Fed’s trimmed mean PCE estimate is catching up to this downside.

If there is a magic number, it isn’t within the grasp of either side of officialdom. Fiscal spending isn’t permanent income, and QE isn’t even the slightest money printing which could create some out of nothing.

Stay In Touch