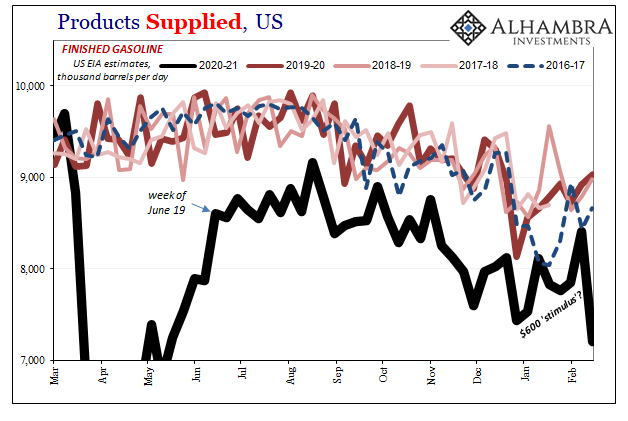

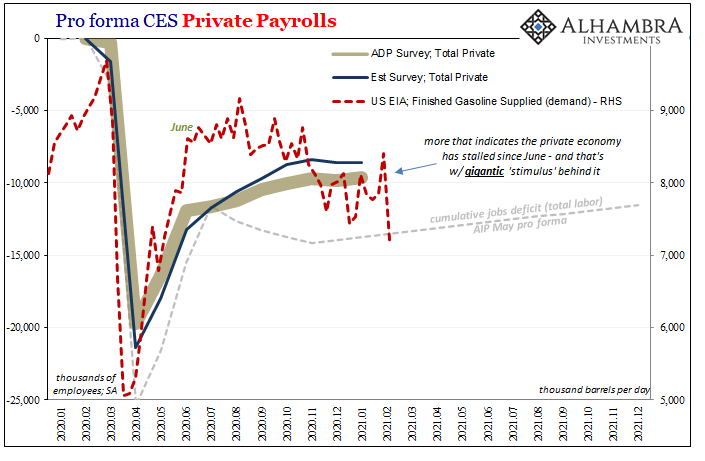

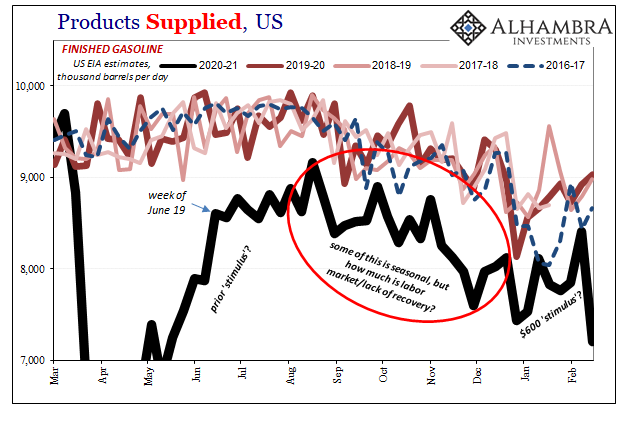

For a couple of weeks, the $600 payments from Uncle Sam seemed to have found their way into the tanks of Americans driving their automobiles a little bit more than they had. According to the US Energy Information Administration (EIA), the total amount of gasoline “supplied” by the domestic marketplace reached 8.4 mbpd the second week of February. Like retail sales, pretty compelling correlation to that last dose of fiscal-ity written out of Treasury the end of last year.

The latest weekly number dropped considerably. Undoubtedly weather-related, the question is how much effect from the temporarily frozen middle sections of the country.

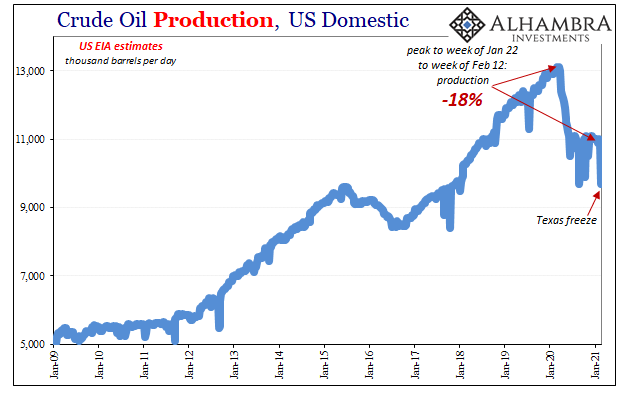

The good news, such that it can be classified that way these days, is that this Polar Vortex tornado shut down a good piece of domestic energy production, too – preserving the basic elements of what is driving crude oil prices vertical. This supply squeeze continues unabated, increased by what happened in Texas, as producers have held down production even as WTI resurrected like the mythical phoenix. They have yet to signal any rush to ramp back up, perhaps spoiling the blackened bird’s ascent.

What that means is clear extrapolation; so long as production remains incredibly suppressed, the oil market overall can continue to – at best – modestly rebalance. It hasn’t quite yet, still future tense; the end of COVID is being projected alongside some semblance of normality in the real economy.

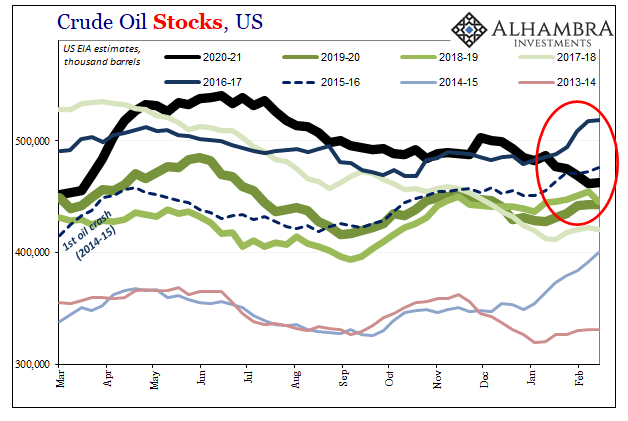

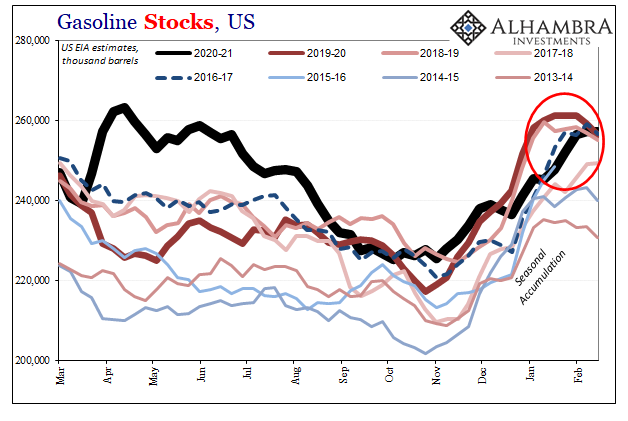

There is some basis for thinking this way, and not just “stimulus” faith. Crude oil stocks have come down during what would otherwise have been a normal period of seasonal accumulation. From record levels despite huge production cuts, to near record levels and suppressed production for as long as foreseeable.

Gasoline is still a problem, though, especially given indicated demand even when picking up in January and early February.

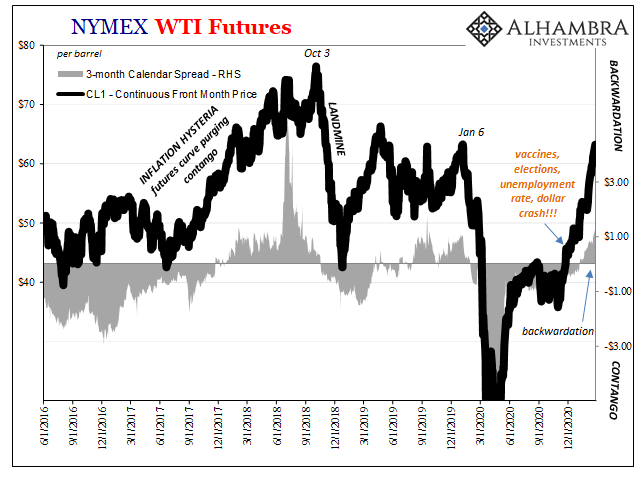

Growing backwardation (incentivizing use rather than storage) at the front of the WTI curve indicates that the market isn’t too concerned with these radically more positive forward projections of physical balancing – even if they are only scheduled for forward arrival.

Obviously, the prospects for more Uncle Sam payments are being traded as having the same effect as those prior transfers. The danger, therefore, lies on the gasoline chart (below) in between them; what happens when, not if, these payments run out? If it ends up being like last time, between summer and the end of last year, when the government stops paying the physical product stops moving (as much). Dependent upon the politics of stipends.

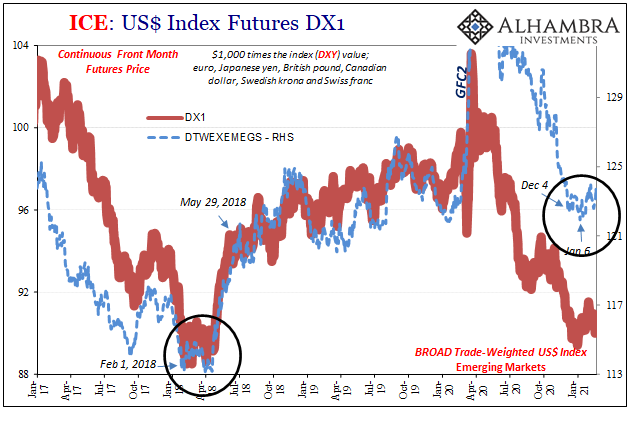

The assumption here, as well as many other markets, is that recovery shows up before this matters; or that recovery will show up because the US government somehow isn’t Japan. Increasingly priced for what seems perfection, though what about the dollar?

What we know from 2018 experience is that WTI can keep moving higher, like long-end UST yields, even as dollar problems (like those discussed yesterday) crop up and then proliferate negatively around the world. This seems to depend upon the extent of focus any potential Euro$ #5 might have on the domestic system; during Euro$ #4, oil prices wouldn’t succumb until October 2018’s landmine, and during Euro$ #3 it took about six months, too, before WTI plunged like long UST’s and CNY already had.

Thus, beyond the potential Euro$ #5 (assuming we really are out of #4), which is only just potential at the moment, there would also be complications arising from these other domestic factors where the physical fundamentals aren’t actually yet back to balance – it’s being presumed they’ll get there uninterrupted before anything else might go wrong.

And largely based upon Uncle Sam.

The government’s stipends have an impact, no doubt. Lasting impact? That really is another question.

Stay In Touch