All the signs were there, starting with the fact that the Fed and ECB together had supposedly the flooded the world with digital money yet a palpable “something” was really off. Ben Bernanke’s central bank had unleashed both ZIRP and QE, the latter of which had finished up a couple months before. In Europe, Jean Claude-Trichet’s outfit was “highly accommodative” in its own right if not quite as openly as their American counterparts.

Then, on Monday May 3, 2010, Trichet and the ECB’s Governing Council issued a notification that it was, well, decidedly ominous:

The Governing Council of the European Central Bank (ECB) has decided to suspend the application of the minimum credit rating threshold in the collateral eligibility requirements for the purposes of the Eurosystem’s credit operations in the case of marketable debt instruments issued or guaranteed by the Greek government.

In other words, the repo market was increasingly rejecting Greek sovereigns on reasonable collateral terms. Unable to source suitable alternatives, apparently, financial firms in Europe pleaded with the ECB to open up its emergency operations to take in the stragglers; can’t pledge in repo, pledge it to the ECB.

In order to do that, officials would have to lower their collateral minimums. Which they did; really not a good sign.

Just three days later, Thursday May 6, at about 2:32 pm EST, US stocks began to a truly frightening plummet. Though it lasted only about 36 minutes in total, it was at first like a scene from October 2008 all over again. Though share prices would recover, this “flash crash” would become a poignant reminder of the unexpectedly fragile situation. Where was this Greenspan put?

The following Monday, May 10, Trichet unveiled the ECB’s newest emergency rescues: a Securities Market Program (SMP) to buy troubled debt (though sterilized, so not QE), several auctions for euro funding (LTROs), and, curiously, to reactivate dollar swap lines with the Federal Reserve.

In other words, feces all over the fan blades.

Not a “euro crisis” but a eurodollar crisis more and more centered on Europe. As we say around here, repo problems simply suck the liquidity out of everything – it hadn’t been a Greek debt problem, instead a global collateral shortfall. Banks stuck with non-negotiable Greece weren’t just struggling borrowing euros.

The much larger issue was how this all had taken place…in early 2010. The first Global Financial Crisis (how was it global, again?) was still very fresh in everyone’s mind except those who took Bernanke at his “money printing” word and had been looking forward to peace and quiet and inflationary acceleration again. It became clear, no such distinctly nonrandom good luck.

Before it ever really got going again, the monetary system had sputtered exposing the real truth – there wouldn’t be a recovery because the money to finance it wouldn’t belong to any central bank. In reality, they don’t have any; even when they change collateral terms.

After the ECB’s return engagement Ben Bernanke was forced into one of his own later on in the same year; the US economy began to seriously sputter, too. How was this given that these were “European” problems? Neither Chairman Ben nor his staffers or successors have ever really said.

In lieu of a legitimate explanation, they just did another QE that November (first hinted at when Bernanke appeared in Wyoming in August 2010).

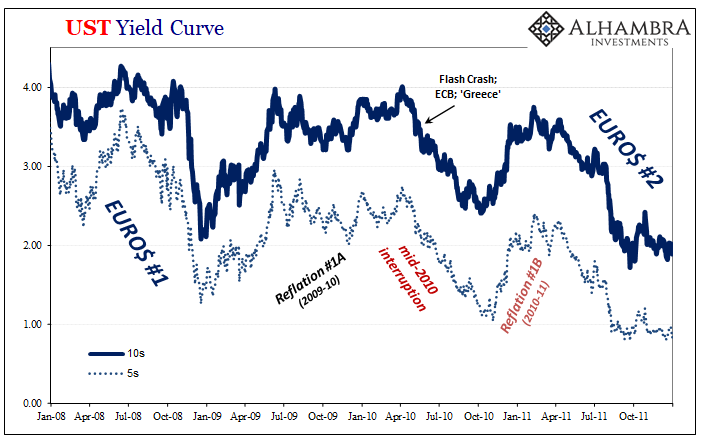

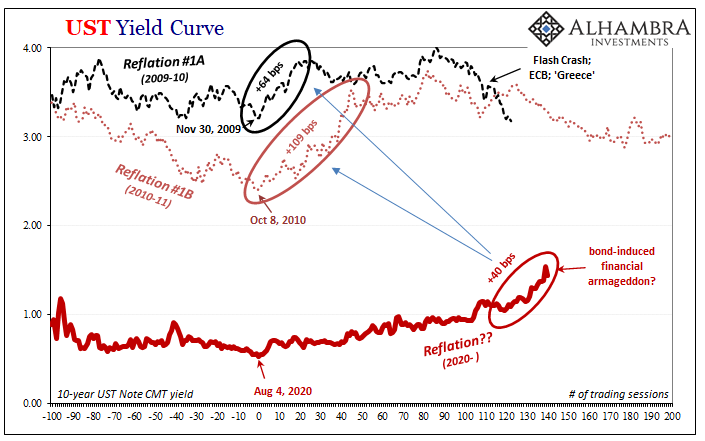

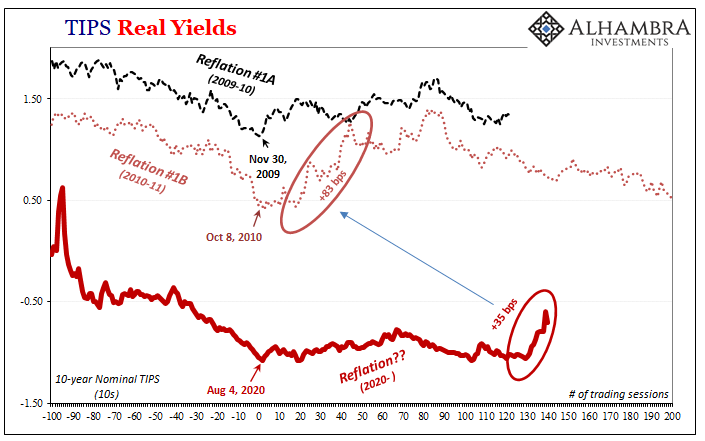

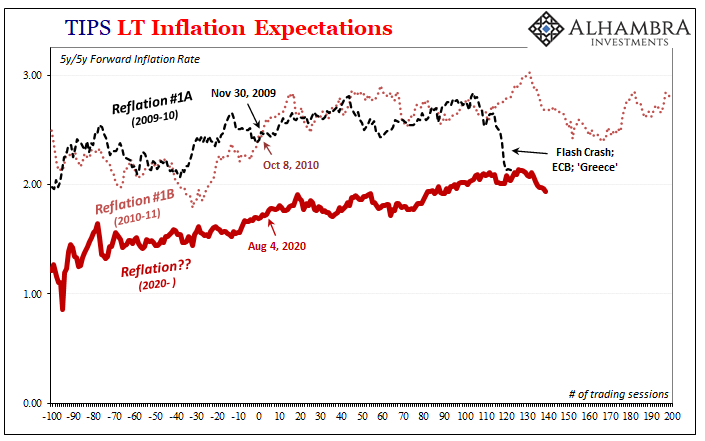

The result of that wasn’t recovery, either, instead an even bigger global monetary problem waiting for all of them – and us – the following year in 2011; Euro$ #2. But in between #1 (or GFC1) and #2 was this obvious dip or dent in the middle of 2010. Ostensibly Reflation #1, split in parts by what had been a real warning about how it wasn’t going well; Reflation #1a and #1b?

In the Treasury market, the result was pretty substantial volatility. Yields up a lot, then down a lot, back up a lot, and then the next plunge. Inflation expectations up, down, up, and then no dice. You get the point.

My purpose here is both a reminder about volatility – that even in “safe” instruments like Treasuries, wild swings have not been uncommon – also why these big moves happen in the first place; no recovery, no inflation, nothing effective about central bank policies that are truly non-monetary in nature. They predict inflation every time, only to see it fall back to earth.

As bond curves shrink, the volatility only looks bigger when it’s not even close.

In other words, they can fool some of the bonds some of the time into thinking reflationary, but never all the bonds all the time out into recovery. Eventually, inevitably, the warning signs are too loud to continue to ignore despite all the “money printing.”

So far as the current 2021 reflationary trend goes, we could only wish it was May 2010 again; the current market is staring way, way up at those depressing levels.

Stay In Touch