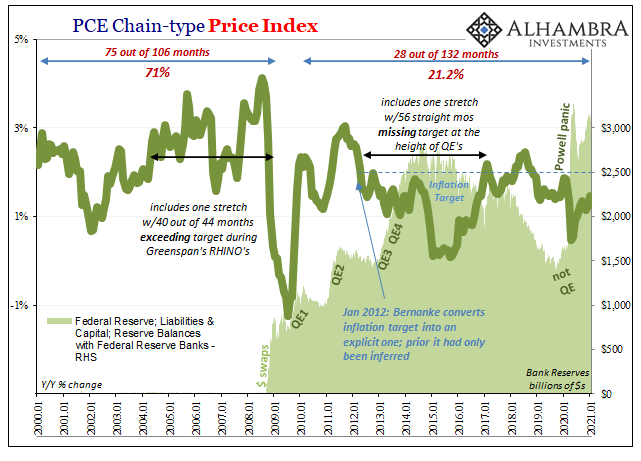

According to the Federal Reserve’s preferred inflation measure, the PCE Deflator, consumer price pressures remained muted in January 2021. No surprise, given the absence of inflationary conditions contained within the prior released CPI report for the same month, as even the contribution from surging oil prices was noticeably minimal in both.

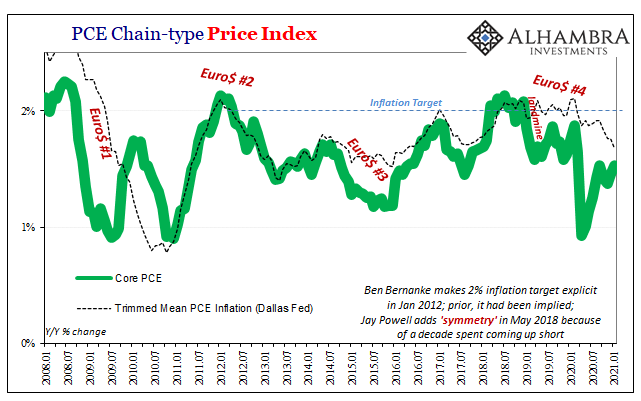

The Bureau of Economic Analysis (BEA) today said that broad consumer prices as derived from PCE data increased 1.45% year-over-year last month, accelerating modestly from December’s 1.26% (and 1.15% during November). The so-called core rate, removing food and energy prices, gained 1.53% in January 2021 when compared to January 2020. That one was up just 8 bps from 1.45% in December.

Forget about any flood.

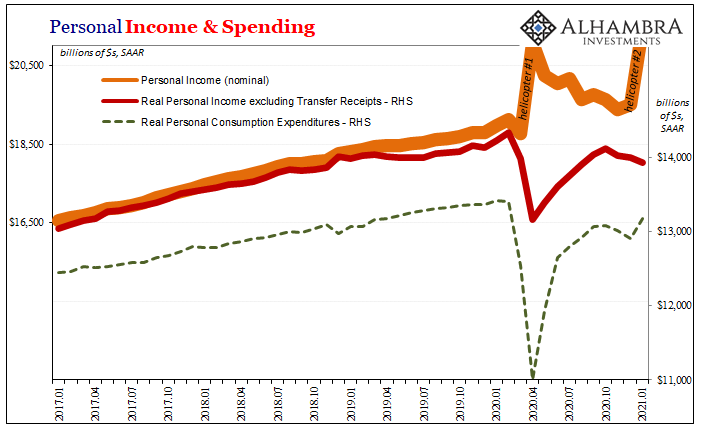

These figures are taken from the first full month when the second of the government’s helicopter payments ($600) had been made. Those transfers clearly show up in the BEA’s Personal Income and Spending data, also released today, having pushed monthly income up by a full 10%!

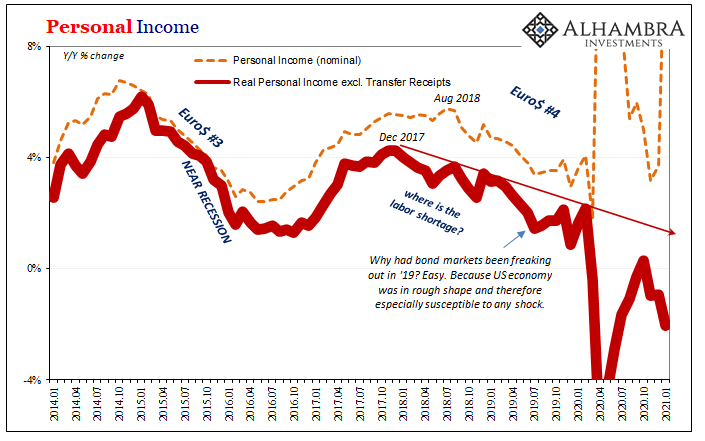

Low inflation, however, is instead being extracted from the fact consumers still prefer not to spend this windfall. Income from private sources, excluding transfer payments, declined for the third straight month in January (which in the past has been used by the NBER as an important indication of recession; then again, the US and global economy hasn’t yet escaped from the last one).

Real Personal Income Excluding Transfer Receipts was revised substantially lower for the last six months before adding to the downward trend which began in November – consistent with rising jobless claims and stumbling then falling payrolls.

Regardless of so much fiscal and monetary “stimulus”, these hadn’t contributed much to the private income where private income was still 2% less in January than the same month last year.

As one consequence, nominal spending (PCE, or Personal Consumption Expenditures, includes both services and goods) was lower year on year, too. While outlays did rise month-over-month – like retail sales, or gasoline demand, a clear effect from Uncle Sam’s wallet – it was miniscule when compared to the scale of the stipends. Americans spent a little relative to how much in excess they continue to save.

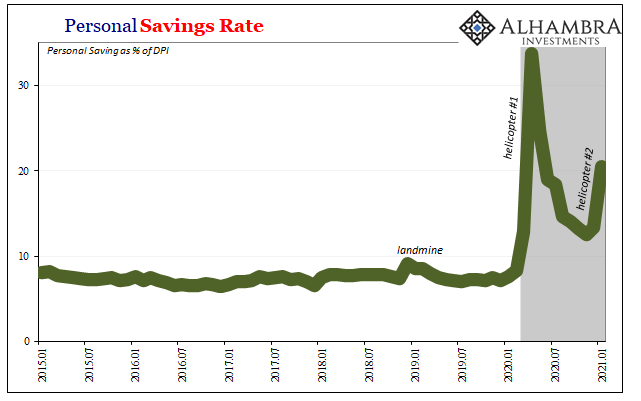

In real terms, PCE increased by 2% in January from December (far less than the 10% gained income) but that was still nearly 2% less than January 2020. The Personal Savings Rate jumped back above 20%.

Nominal income will decline again in February since the “other” piece of the last helicopter (the advertised $1400 “remainder” of the $2000 initially promised by the government during the last days of the prior administration) stuck in Congress would show up in March at the earliest. The more important data continues to be taken from the private sector and the labor market, the latter of which has seen mixed results this month (rising jobless claims in the first half, improving in the second half, but still at record levels).

Nothing, therefore, to either confirm or deny the emerging Goldilocks prospects:

The Treasury market is beginning to price scenarios – assuming no hitch in vaccinations nor re-acceleration in contagiousness – where the economy becomes largely COVID-free (assuming also governments accede to the data) at some point in the near rather than distant future.

Furthermore, it is being assumed there’s a decent chance Uncle Sam’s helicopter payments will be able to clean up or at least paper over any leftover damage from the deep and longer-lasting recession (when compared to initial “V”-shaped expectations).

Pandemic-free with the feds absorbing the majority losses is the Goldilocks scenario; and, despite the sell-off, it isn’t being priced as some sure thing.

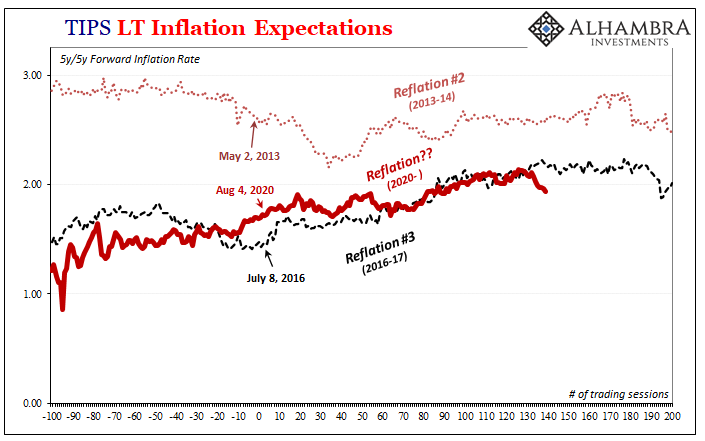

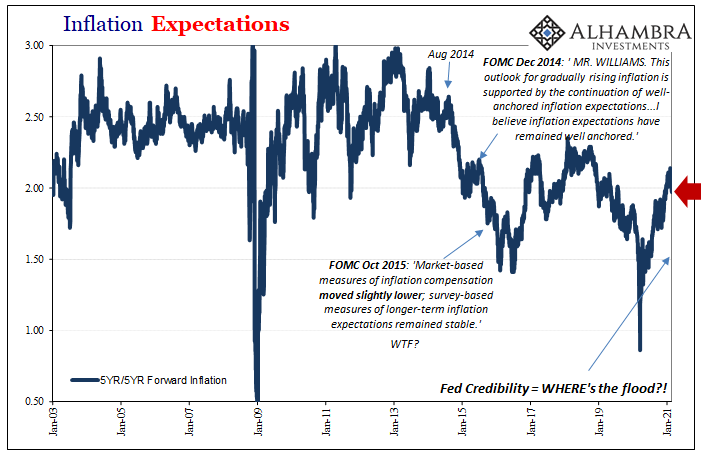

It’s “just right” because on the one hand there is the “too hot” possibility where inflation does get out of control spiraling upward toward some Great Inflation 2.0 which would be a dangerous further wallop of misery to last year’s (and ongoing this year) devastating contraction. Fortunately, there isn’t any indication that’s anything other than a low maybe even trivial probability (in either the current inflation data or market-based inflation expectations).

On the other hand, the “too cold” scenario, that’s where the economy despite Uncle Sam continues to drown in deflationary negatives driven from an unfixable labor situation that can’t get going any further than it did in 2020 (only about halfway back); long run economic damage simply too much to overcome in a prolonged and painful road forward. It is this we see in the current data, so markets – including the long end of the Treasury curve – are repricing the balance between “too cold” and “just right” with a slight, not large, tilt toward “just right.”

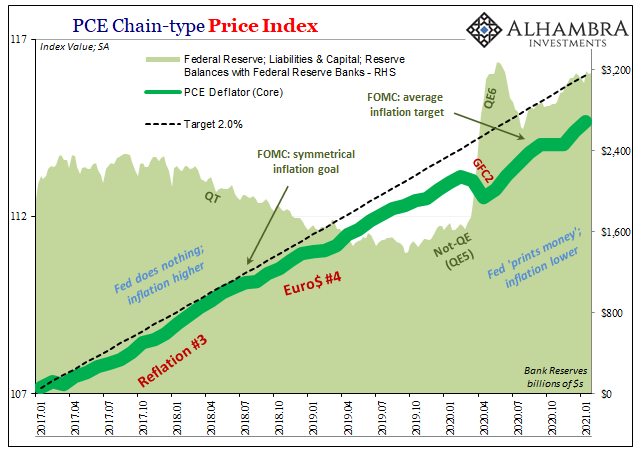

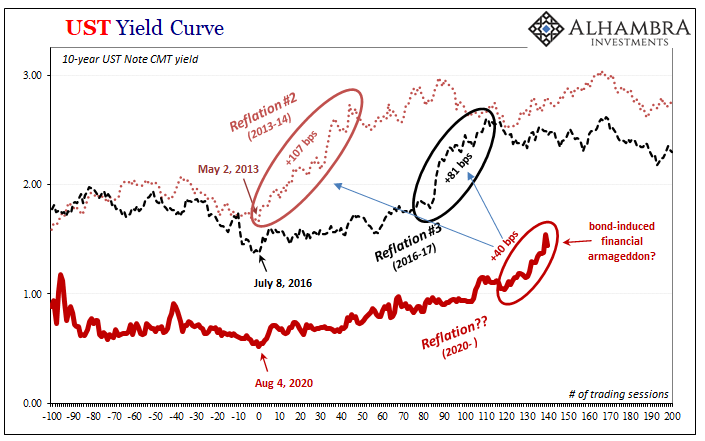

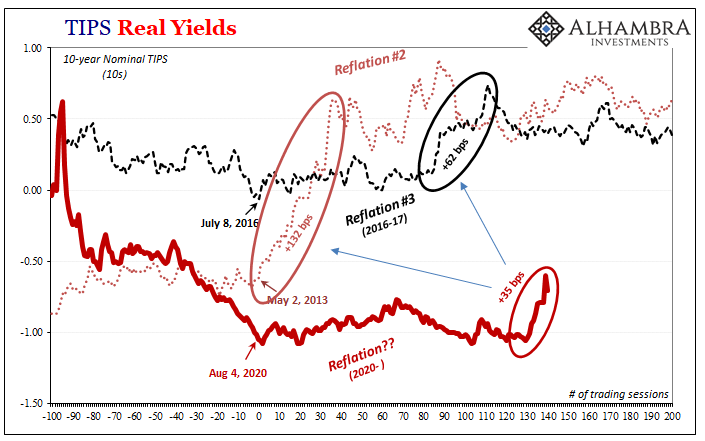

This is also why, to this point thus far, the current reflation trend remains well short of even Reflation #3 which had been the weakest of any of them.

Uncle Sam can lead Goldilocks to water, bribing her to reach into it with TGA dollars, but can those helicopter payments really get the three bears to act upon their (presumed) spending thirst? Again, data so far says no; markets are a touch more optimistic than they had been certainly in December.

Stay In Touch