I’ve been getting that question a lot these days. How high can rates go? It is asked in a way that seems to imply that the answer is obvious – not much. Why? The answer is almost always the same; the Fed can’t and won’t let rates go up. If they did, it would kill the economy and raise the interest cost of the government. They can’t let that happen so they’ll implement yield curve control and keep long-term rates from rising. The Fed is believed so powerful that their mere promise to buy bonds to cap yields would stop the selling by any and all other bond owners.

I suppose that is possible but I have my doubts as to whether the Fed would even attempt to control the yield curve as they have in the past (during WW2 and for six years after the war, most recently). The holders of Treasuries back then may have felt some patriotic duty to hold their bonds that today’s holders surely do not. Not only are about a third of Treasuries owned by foreigners, but even the ones owned by Americans are not generally owned directly. Americans today surely don’t own bonds because they feel any patriotic obligation to do so. Could the Fed stop a tsunami of determined selling? Well, of course they could, but at what cost? I am certain of one thing; if the Fed needed to and did stop long-term rates from rising, something else would fluctuate instead. There is no free lunch. In the post WW2 period, after price controls were removed, inflation rose 18% in 1947 and 10% in 1948. And the Fed kept the 10-year pegged at 2.5% until 1951. As I said, something else will fluctuate.

Let’s take a different view of the potential for rates. As I’m sure you’re aware the yield curve has been steepening of late. The 10-year/2-year spread has widened recently to 1.42% from negative in August of 2019. In the past three recessions and recoveries, the curve has steepened to at least 2.5%. If the 2-year rate stays at current levels and the curve steepens to 2.5% that implies a 10-year yield of roughly 2.65%. Is that going to happen? I have no idea but I think it makes sense to see that as the potential even though there are significant differences between today’s steepening and past episodes (I’m not going to go into all that in this update but suffice it to say that rates aren’t even going in the same direction as past steepenings).

The bigger point is that you shouldn’t assume you know what the Fed will do or what the effect would be if they tried. One thing everyone should have learned over the last decade or so is that even the Fed doesn’t have a clue how their policies will impact the markets or the economy. Besides, as I’ve said many times, you don’t need to know the future to be a good investor. You just have to observe and analyze the present in a reasonable way. Assuming that this steepening will be similar to the past three is probably a reasonable – if far from certain – assumption. Bonds are very oversold presently so I would not be surprised by a near-term rally. But the trend for rates is up and it probably isn’t over.

Investors are anticipating better economic performance this year and markets reflect that view. Rising inflation and growth expectations have pushed interest rates higher as investors sell bonds and gold to buy more growth-sensitive investments – stocks and industrial commodities. While the move in bonds feels rapid it has been building for months as have the moves in other markets. We added small-cap and emerging markets last year in response as momentum shifted. In late February we shifted to small-cap value as the re-opening trade gained momentum. We are also seeing a shift in the dollar – now in a short-term uptrend but neutral long term – which prompted us to reduce our gold position. We didn’t need to predict anything to make those moves, just observe markets and respond.

I don’t know if the markets will be right about future growth and inflation. Markets are efficient, not infallible. And there seems to be a pretty big difference between what bonds are expecting versus stocks and commodities. The nominal 10-year Treasury rate rose 9 basis points last week while the 10-year TIPS yield rose 4 basis points. Yes, that is as insignificant as it sounds. Why did rates rise? The simple answer is rising inflation and growth expectations but the moves are small. I keep hearing that there is going to be a boom once everyone gets a vaccination but I’m having a hard time finding it in the place I’d most expect it. The direction is right but the level is still pretty anemic.

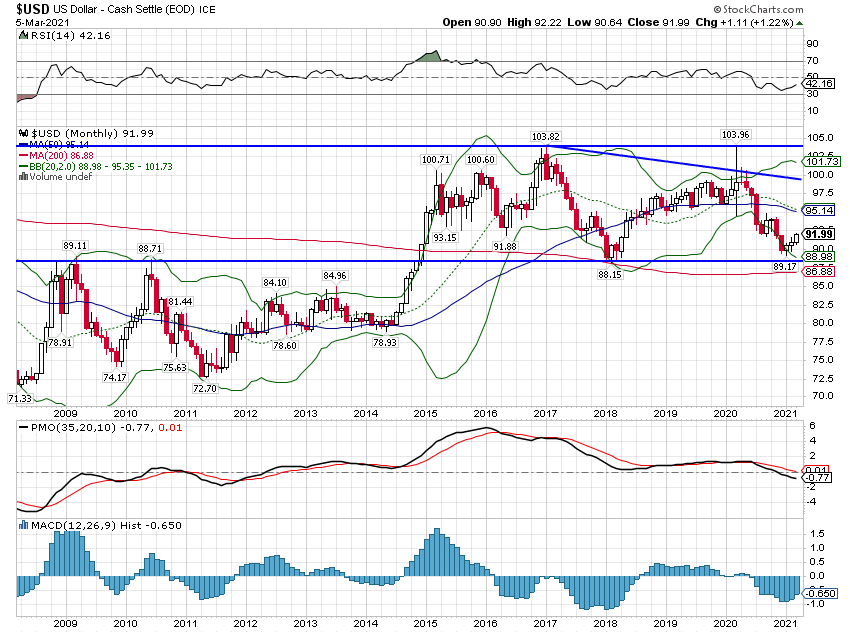

The environment has changed slightly to Growth Rising and Dollar Neutral. The short-term trend for the dollar is up but we are at the bottom of a range that has persisted for roughly 6 years. For now, I’m not willing to make any big changes to our portfolios based on this weak rebound. We did reduce our gold position but that was driven as much by momentum as the dollar. We would also normally make a shift to US growth in a rising dollar environment but that is being overridden currently by momentum which is heavily favoring value.

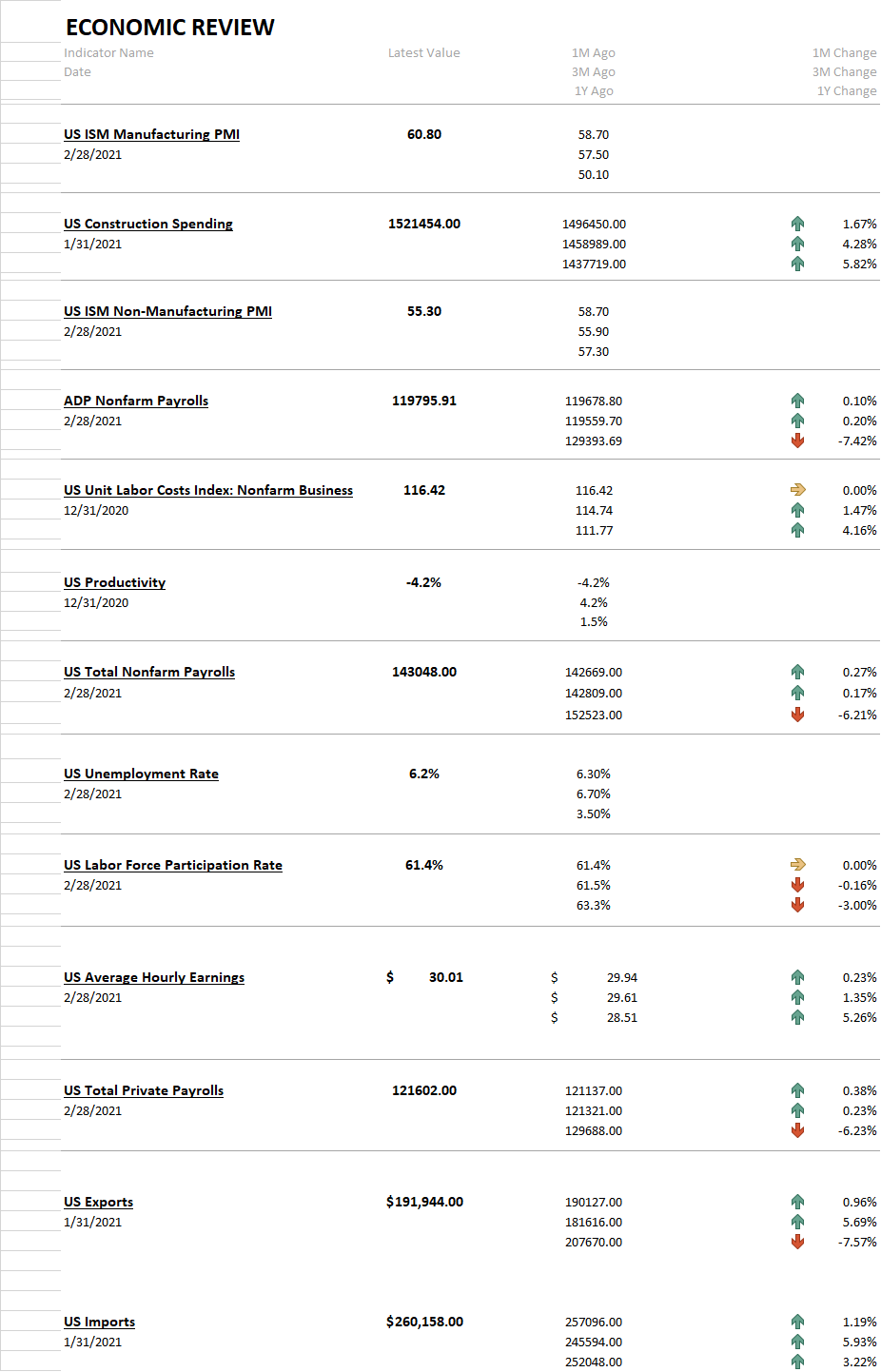

The economic data released last week was certainly taken as positive and some of it fits the bill. The ISM manufacturing index rose above 60. Construction spending was better than expected and up nearly 6% year-over-year. Imports and exports were both higher and imports are up about 3% year over year. The ISM non-manufacturing index was a bit disappointing but at 55 is still pretty good. The payroll reports were mixed with ADP disappointing and the official report looking pretty good, at least on the surface. There was an obvious re-opening tilt to the report with leisure and hospitality leading the way. What was disappointing was, well, everything else in the report.

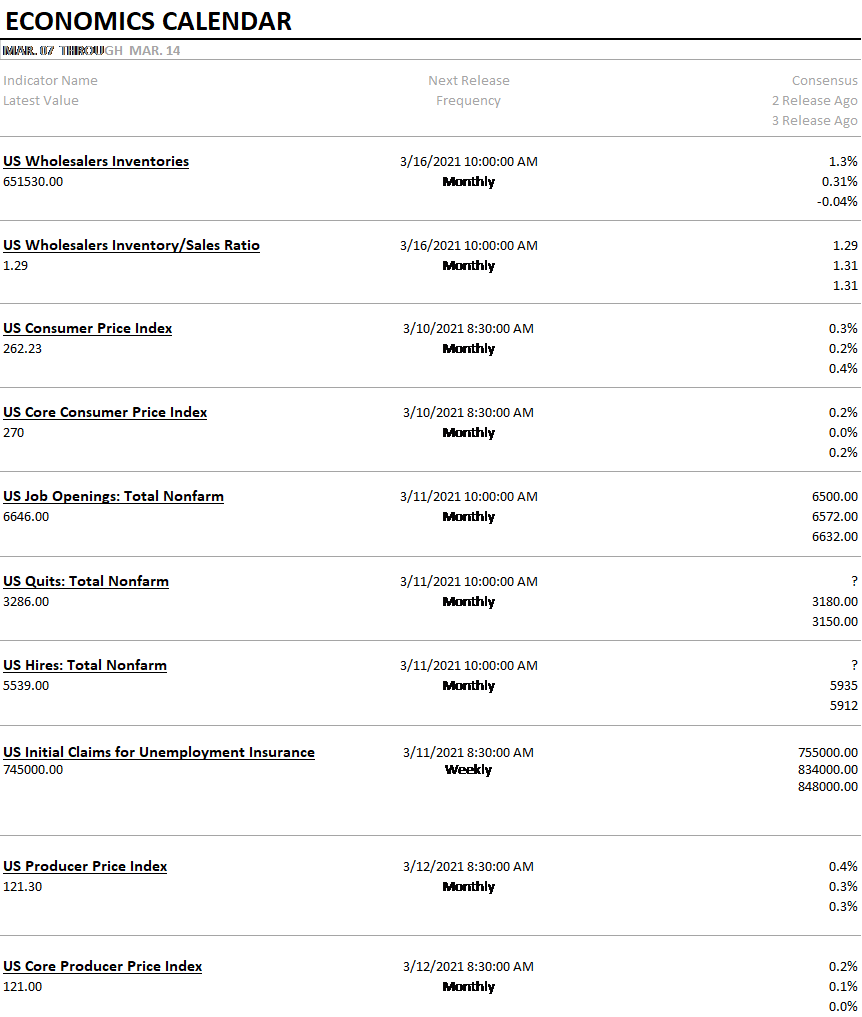

Next week’s reports will include inflation at the consumer and producer levels. Don’t be surprised if the reports are taken as too hot but don’t get too excited. This recession was different than past ones – a supply shock – and re-opening seems likely to raise prices in the short-term. That doesn’t mean it will last and it doesn’t mean it has anything to do with Fed policy. And the more important report next week is the JOLTS report. We need some good news on employment.

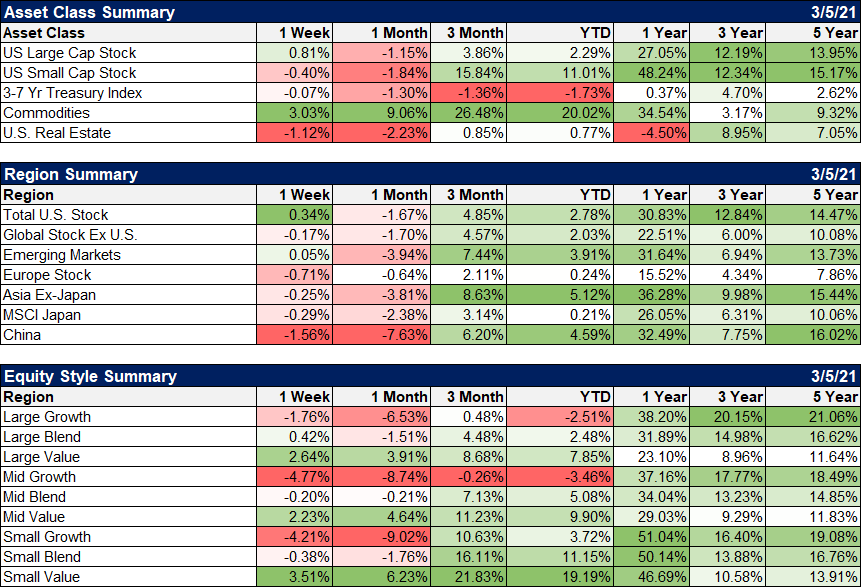

It was a volatile week but US stocks still managed to squeak out a gain. EM was up slightly but Europe and Asia were slightly lower on the week. The big winner was commodities as it has been all year. Commodities are actually up more than stocks over the last year now.

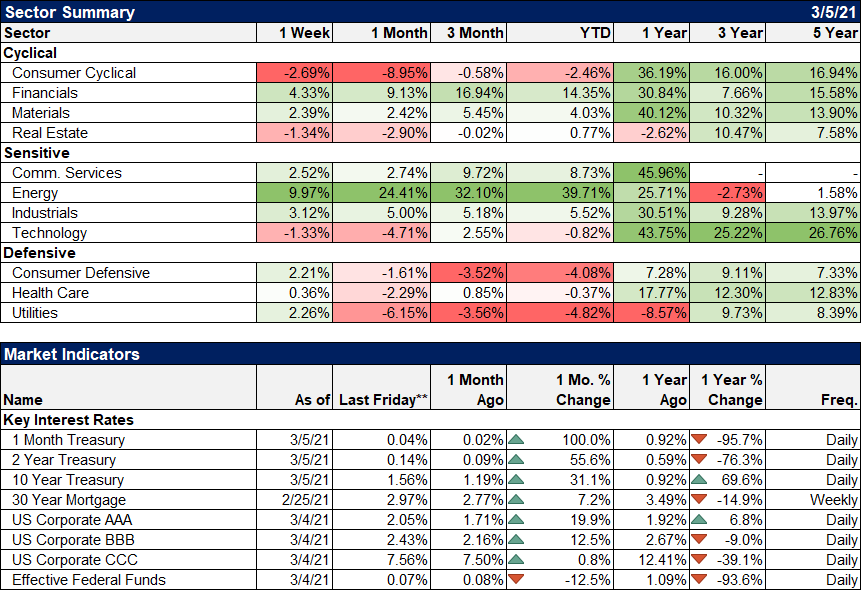

The real divergence was between growth and value. US stocks were up but growth stocks were not. Small-cap value was the big winner, up 3.5% on the week while small-cap growth fell 4.2%. This divergence is being driven by the belief in an economic resurgence as vaccinations proceed and the economy opens up fully. We see this in the sector performance as well as Financial, materials, industrials, and energy all posted health gains last week.

The dollar’s direction is a very important indicator for us and our investment process. The recent turn higher is due to a shift in relative growth expectations. The US is seen as improving more rapidly than the rest of the world. The most obvious comparison is with Europe where governments seem to be having a very difficult time getting vaccines in arms and we continue to see rolling lockdowns as outbreaks flare up. But I think the more important comparison is with China which last week announced some pretty subdued (for China) growth expectations. The Yuan has also recently stopped rising although we haven’t seen any significant weakening yet. This is, for now, just a source of concern, a little heartburn for your portfolio manager. But it definitely has my spidey senses tingling.

Joe Calhoun

Stay In Touch