While we consider the PPI’s view of inflationary pressures as overstated by simple arithmetic and the math of commodities, there’s no denying that producer prices have risen by a substantial amount. The question, the whole issue, is why. If it is truly because price pressures are building and have grown close to breaking out in systemic fashion, then that would indicate the sustainable trend more consistent with the term inflation.

In order to reach that threshold, producer prices must become consumer prices otherwise disaffected businesses are left holding the bag. Needless to write, that’s the opposite. Such a case very quickly turns depressive, disinflationary if not in the extreme – firms that can’t pass along input costs to their customers will be threatened as to their bottom lines.

And the bottom line in that situation is when the business sector caught between the rock of producer prices and the hard place of no pricing power can only release the burden by over-governing what they can control, meaning costs therefore labor.

Producer prices are up, as noted, but not yet to such that extreme. Consumer prices, either way, are not. The PPI rises at the fastest rate in a very long time while the CPI rises at the fastest rate since the not-very-inflationary 2018 period. This is definitely an instance when “highest in three years” undersells the disappointment.

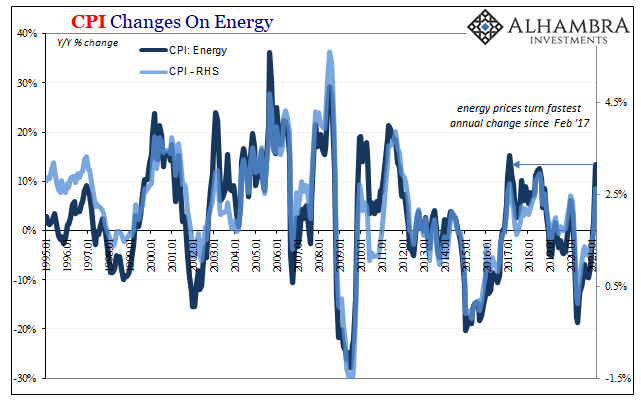

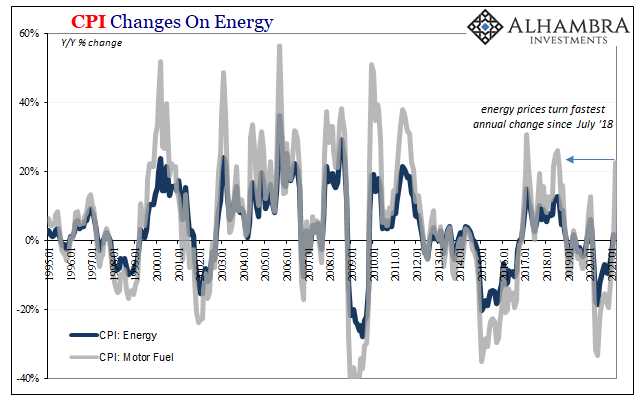

Start with base effects – comparing prices to March 2020 and the onset of outright deflation – and then go longer into oil and gasoline prices. The net result so far as the BLS can calculate is a headline CPI rate of +2.62% for the month of March 2021; again, the highest since the middle of 2018 back when Jay Powell was attempting to cheerlead inflation into existence because it was nowhere near a realistic possibility.

He’s now on this side of being rational (by accident, but still) because he can do the numbers, too. Much of that 2.62% year-over-year increase was pure gasoline; motor fuel prices last month were up 22.7% on average when compared to March last year. It sounds very 1970s-ish until you realize that gasoline prices had accelerated in similar fashion in that same year as Powell’s big mistake.

Hardly unusual, which is why energy prices are treated as the volatile piece of the consumer basket.

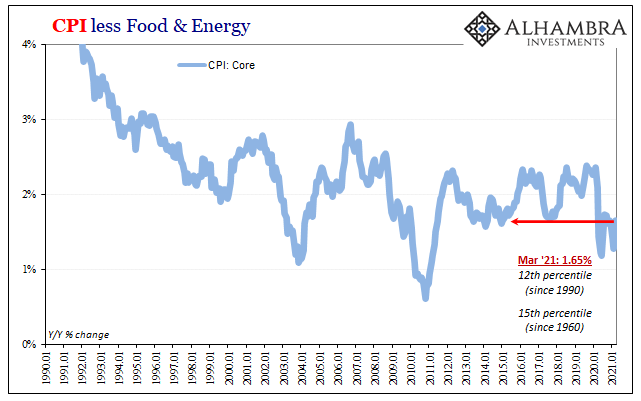

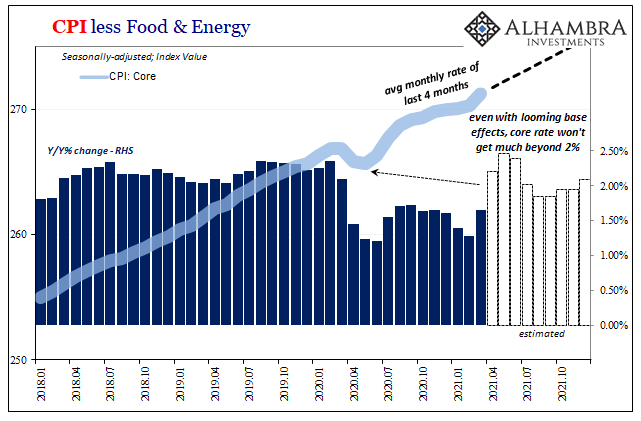

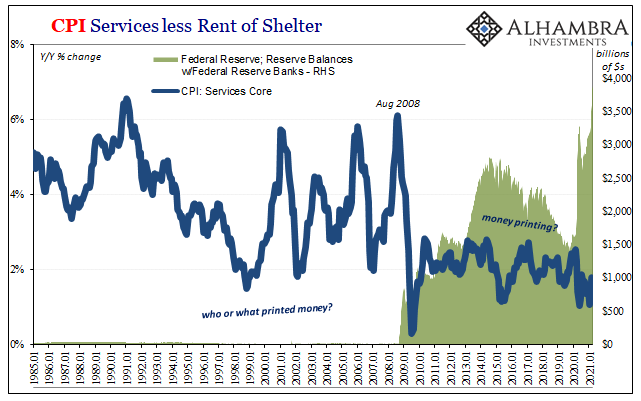

Outside of what goes into most vehicles, consumer prices continue to be incomprehensibly tame (at least when compared to “monetary” aggregates like M2 or the Fed’s bank reserves). The so-called core CPI, stripping out volatile food and energy, gained 1.65% year-over-year, up from a near-series low of 1.28% in February. All that did was push the rate from among the lowest in its history to slightly better than the lowest in its history.

At the current seasonally-adjusted pace, the core CPI won’t get much better than 2%, maybe pulling up close to 2.5% by May from base effects – and that’s with those at their most favorable (to the inflation case).

The entire set of CPI data is splashed through with disinflation despite what seems to be everything in the world aligning toward meaningful acceleration; it certainly has been described this way.

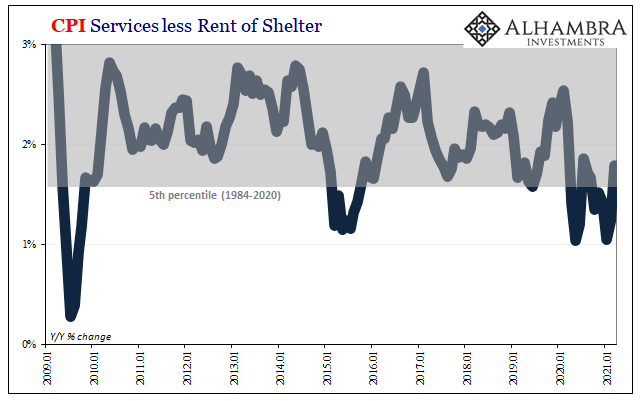

The core services CPI index “leapt” 1.79% year-over-year, for example, “surging” from February’s dismal 1.23% which in reality looks like this:

Even when you zoom in close, even with base effects, 1.79% remains among the lows; entirely too consistent with the onset of March 2020’s yet-unsolved recession with no paradigm-changing boost in sight.

About the only factor March consumer prices did not have on their side was a full month of the $1400 helicopter model – though the funds were released it wasn’t a completed calendar for Uncle Sam. And that’s the only “downside” from the expected consumer price expectation; half a month with federal direct-to-consumer installments.

The impression anyone gets is that there can’t be a rational thinker who doesn’t think inflation is a foregone conclusion; given all the cash thrown around and other disease-related positive developments, supposedly this thing’s only a matter of time.

Yet, here we are with March 2021 CPI figures (which, we need to keep in mind, are constructed using older techniques and therefore actually represent a more buoyant set of baskets producing the upper bound for estimated broad consumer price levels) and even the gasoline comparisons are underwhelming; everything else is still just blah very much like the real economy.

That’s ultimately the point; while the media is universal and uniform about the certainty written into projected inflationary outcomes, those are in any rational consideration the outliers! On the contrary, global markets – orders of magnitude larger in number as well as on a different planet in terms of importance and track record – remain firm and resolute that even if consumer prices do flash some volatility over the coming months it won’t add up to anything more than that.

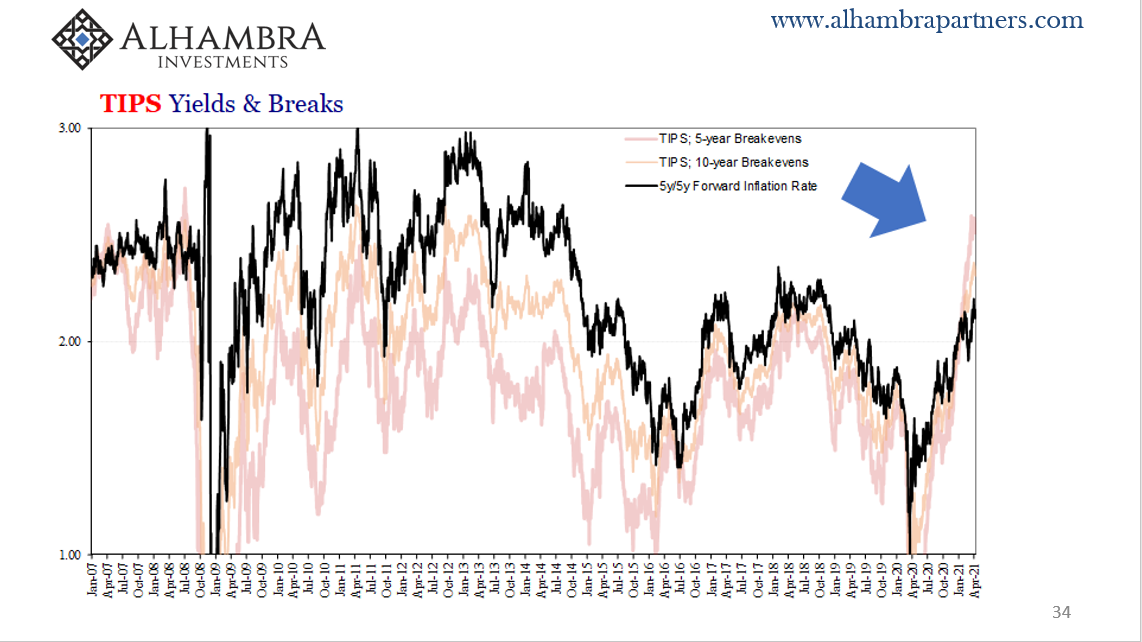

Market-based inflation expectations (and not just TIPS breakevens) are plotting economic potential that is entirely too familiar to the recent past, to recent circumstances. Given these CPI estimates being much 2018-like, and their relation to PPI figures, the true consensus opinion about lack of inflation continues undeterred even if consumer prices can’t; because, it appears, consumer prices can’t.

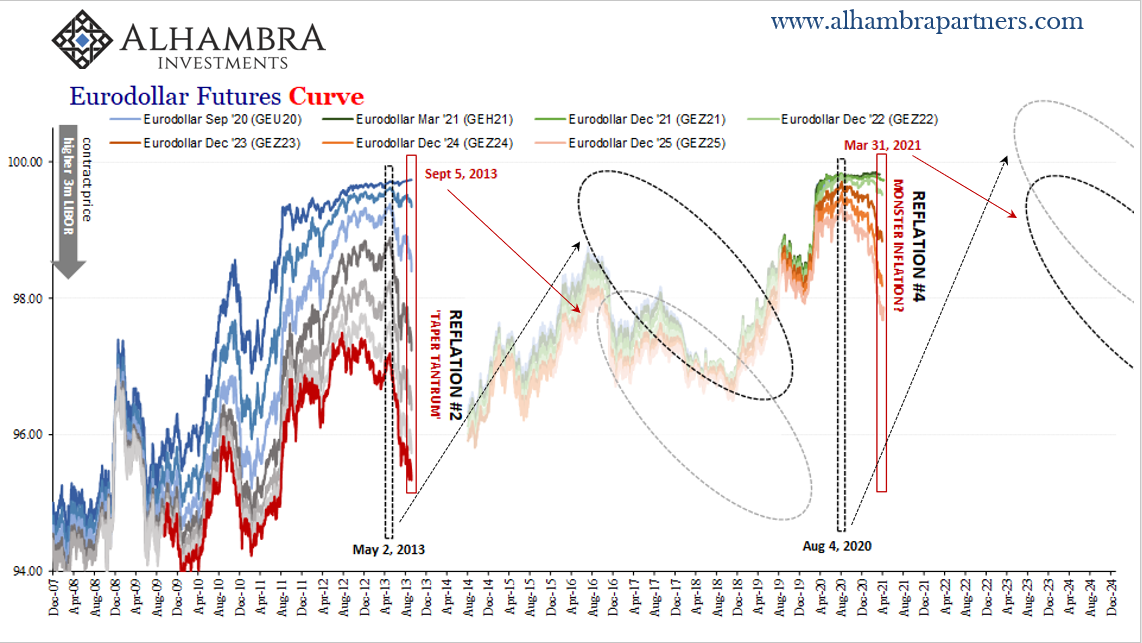

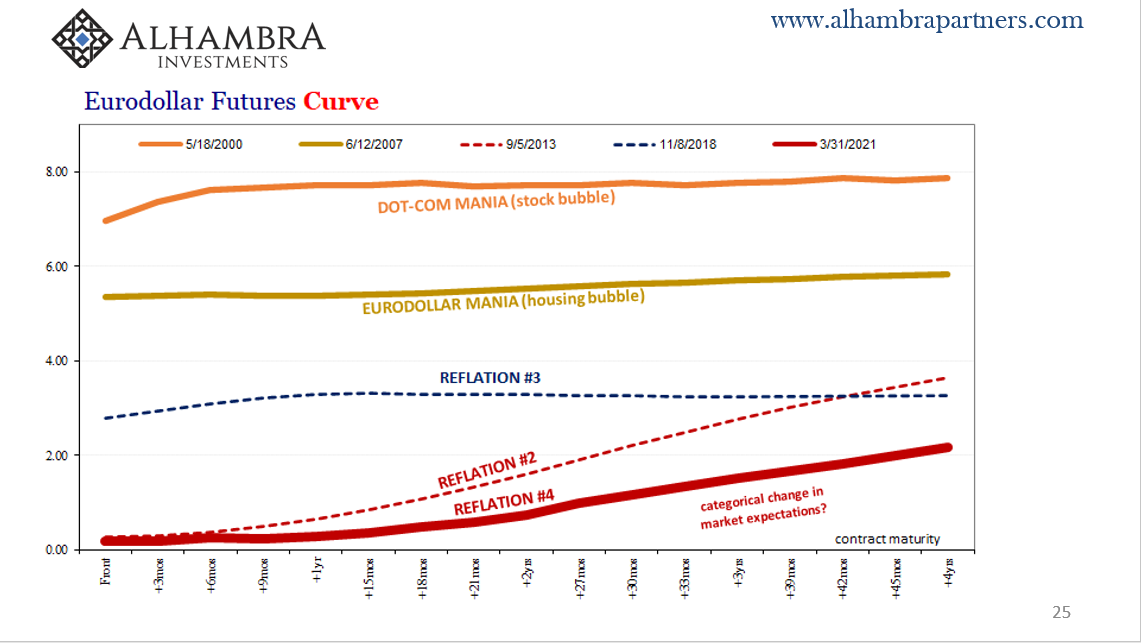

M2 to the moon, bank reserves following close behind, Uncle Sam’s simple arithmetic of 1400 times 350 million (more than a few million deceased are going to get paid, too), and this is it? From TIPS to eurodollar futures, UST yields to their German and Japanese counterparts, there is a remarkably consistent viewpoint over how the inflation debate is actually settled for now and the longer run future.

It was settled 14 years ago, as a matter of fact and there still isn’t a single thing other than emotional hardcases to indicate otherwise.

NOTE: slides below belong to my upcoming appearance, released Thursday 4/15, with Erik Townsend on MacroVoices where we will talk at length about what markets are indicating so far as inflation probabilities are concerned, including an extensive detour into just what it is eurodollar futures curves/prices actually mean.

Stay In Touch