Then-President Trump was eager to talk in May 2017. Having been elected in 2016 by giving voice to what he called the “fake” unemployment rate on the campaign trail, and therefore mobilizing millions of the disaffected uncounted by that official ratio’s official definitions, it was enough to put him just barely over the top. To continue with the agenda, to keep his promise (or appear to; depending upon your affiliation), one of his first priorities had been what everyone calls “pump priming.”

Trump sat down with The Economist magazine in May 2017, early in his term, for a lengthy interview selling them on what was to be his “stimulus” plan. It quickly devolved into a war of interpretation between the President and the mainstream media adamantly opposed to him, focused entirely on the words used during the discussion rather than the substance of what had been discussed.

Worded clumsily, sure, and Trump was thereby accused of claiming that he came up with the expression “prime the pump” as if he had been expecting an interviewer from the orthodox, Keynesian The Economist to not know the idiom or its common use.

Ironically, it did not come from John Maynard Keynes, either. Though the phrase is most often associated with his name – correctly – Keynes never wrote it in his General Theory.

Nowadays, Economists have another term they generally use for basically the same deficit: hysteresis.

Either way, however articulated, the concept is universal and relatively simple (and thus doesn’t really need the fancy wording). It’s akin to inertia, as I described a long time ago in piecing together why there would be a President Trump in the first place:

That was the entire point of the “Q” in QE; suggesting to the public that there was mathematical “science” to the whole thing. Monetary experts wielding enormous technical knowledge could precisely recite and then harness forces to defeat and overcome hysteresis – the idea that an economic factor or even the whole economy requires a “push” in order to get it moving. Thus, QE was proclaimed as the precise calculation that would both figure exactly the resting force on the economy keeping it down and then the means and quantity of force (monetary) required to overcome it.

That it hadn’t accomplished either of those things led to, and partly explained, the recovery-less recovery which then spun off into Trump (as well as the showing for his left-sided twin, Bernie Sanders).

This was the fakeness behind the unemployment rate from which now-President Trump early in 2017 was intending to escape. Pump priming, hysteresis, whatever, the “stimulus” idea was to use the fiscal power presumed possessed by federal government authorities to clean up after the ineffectiveness leftover by the Federal Reserve in its tunnel-vision QE madness. If the Fed couldn’t do it, then Treasury would – as if Obama hadn’t actually tried.

Needless to say, no surprise The Economist had been Trump’s first planned stop to sell the plan; an utterly conventional outfit practically tailor-made to blindly accept every last conventional bit of it. They didn’t care about the language controversy, over-eager instead to encourage the effort and its quick, forceful adoption (becoming December 2017’s TCJA followed shortly thereafter by The Economist’s this-didn’t-age-well cheer section).

If by 2016 and then 2017 recovery had been thwarted by some powerful stopping force for all that time, resisting several large conventional means (including Obama’s ARRA) all along the way, how would even more standard means successfully answer that same force? It wouldn’t.

It didn’t.

The 2017 “stimulus” hadn’t done much at all. Contrary to accepted dogma, at the same time The Economist was writing so positively about its prospects the entire global bond market began betting right against it (first higher dollar, then curves twisting, finally proof in 2019). If you have to keep doing this stuff, this stuff doesn’t really work.

Sour, not soar.

If you have to keep “priming” the “pump” year after year after year, we aren’t talking about Keynes, Trump, pumps nor priming; not really. Chances, most probabilities, simple are not on your side – which means they aren’t on our (the real economy’s) side, either.

But there remain those who can’t believe in such things (conventional Economists, for instance, have instituted a mathematical prohibition on permanent shocks in their statistical models, meaning worldview). Furthermore, they attempt to marry this worldview with actual market outcomes otherwise outright contradictory.

If the 99th prime to the pump hadn’t been enough, surely it will be #100?

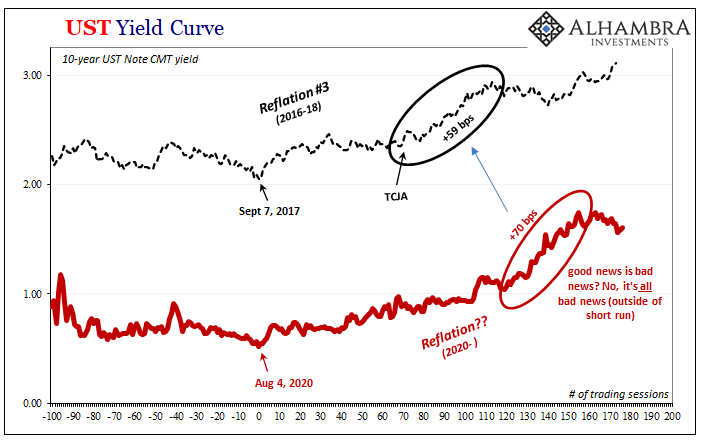

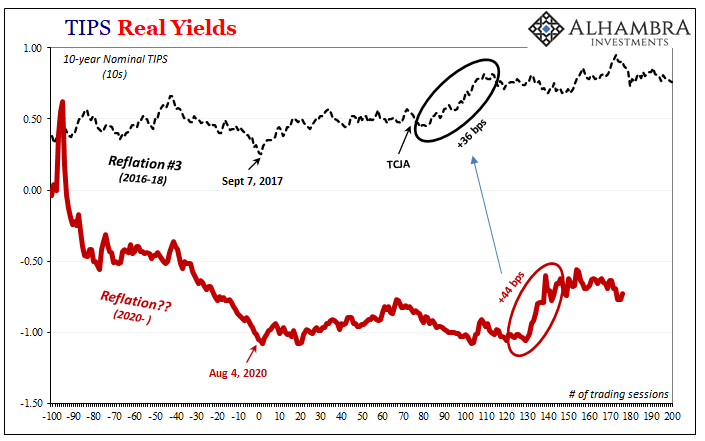

Not only this, we are led to interpret interest rates as if this would be the case; that rates rise on the anticipated success for pump priming but then fall as positive economic outcomes and trends necessarily suggest less need for additional “stimulus” in the future (the so-called “good news is bad news” argument). Seriously, some say that rates go up (reflation) based on expectations this stuff works, but then fall when that stuff appears to start working as if the market becomes disappointed over how success will mean less stimulus – as if stimulus itself is the market’s operating discipling, it’s whole object.

Huh?

Here’s what I mean, a very good recent example attempting to bridge the divide between last week’s “enormous” economic data and the bond market being bid rather than sold by response:

With rates traders still amazed at the shocking bond market response to Thursday’s blockbuster economic data, Rabobank strategist Richard McGuire chimes in and writes that the Treasuries market has undergone a “notable” change in the way it reacts to U.S. data since last year, with Thursday’s stellar economic reports seen as reducing the odds of aggressive fiscal stimulus.

You would think instead how the Treasury market might react to stellar economic data and further leap toward reflationary selling (rising yields); after all, stellar economic data is the whole point. The market is not led around by promises of more government freebies, it is waiting (patiently) for the day when the economy unambiguously no longer needs them.

If, on the other hand, the market foresees more of the heavy arbitrary hand of “stimulus”, that’s a very solid indication that hand and what it had offered has not, nor will, overcome hysteresis; it could not have primed any pump, just the issuance of a lot of inappropriate names and confusing interpretations.

Thus, the current situation easily explained: for now, anyway, the market sees the latest “pump priming” (including Trump’s final) as little other than the same type and character going back to when all this started therefore on the same long run path. Possible positive effects limited to the short run, leaving unanswered the only question demanding every issue.

Lots of government, then what? If your or anyone’s answer is “still need more government”, nothing has changed.

This is stubbornly low interest rates in a nutshell.

Given such an established pattern, skepticism shouldn’t require so much explanation. It is and has been thoroughly and empirically established as the baseline condition and expectation for nearing a decade and a half! The burden of proof has – beginning in late 2006 – swung all the way to the other side, it’s just that most people don’t know this.

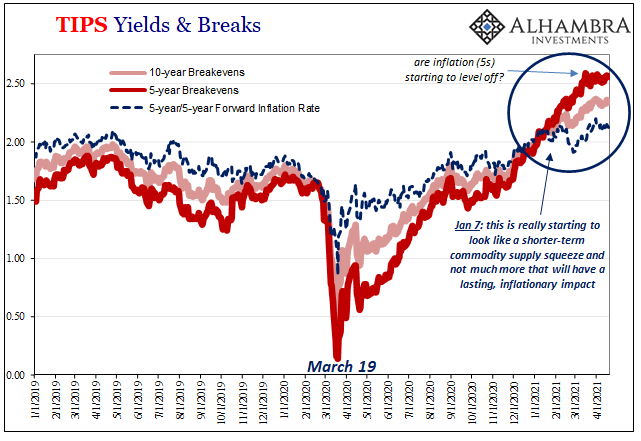

Further disinflation remains the consensus, if not in the media then certainly where it truly matters. Bonds, partly, yes, the real economy most of all. The “pumping” goes ever onward – and that’s the thing.

Stay In Touch