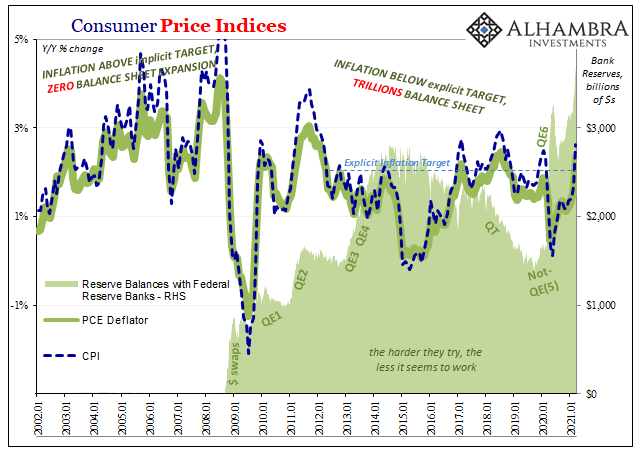

Trillions in “stimulus”, American consumers buying goods at a frenetic pace (in lieu of services), gasoline prices punishing, the start of favorable base effects, yet all those things couldn’t push the inflation rate much further beyond the Federal Reserve’s 2% explicit target. And remember, in order to meet the newly designed economic goals on the inflation side – average inflation targeting – monetary officials have pledged to let inflation go above by more than a little and stay above 2% for the situation to average out how they want.

According to the monthly estimates produced by the BEA (the quarterly figures were released yesterday alongside the GDP data), in March 2021 the PCE chain-type price index (seasonally-adjusted) was 2.32% more than it had been in March 2020 when it was already on its way down into GFC2 deflation. Compared to last February, prices are up almost exactly 2%, hardly the monster hiding supposedly in plain sight.

And that’s with the full weight on gasoline and energy.

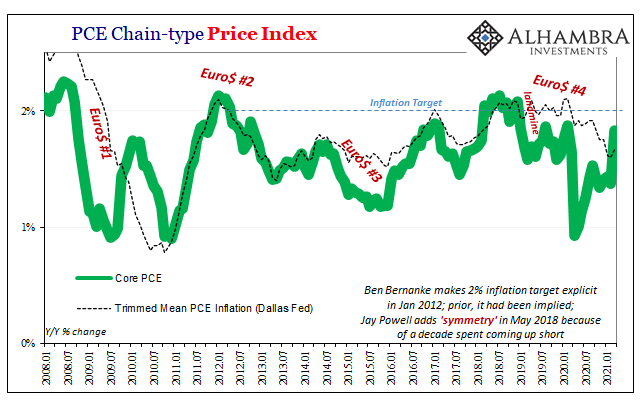

Without those, or food prices (yes, I know food prices are rising; but other goods prices are not rising near as much and the prices of many services are still being heavily discounted; inflation is not one or the other, it is sustained increases in all of them together), the core PCE advanced by just 1.83% year-over-year. Further establishing my parenthetical aside, the Dallas Fed’s trimmed mean deflator last month was up all of 1.67%, indicating, on balance, only a small proportion of consumer prices rising in the way most often described.

Everything else besides categories like food must instead be rising at rates that don’t even match up to the past few years; such as 2018.

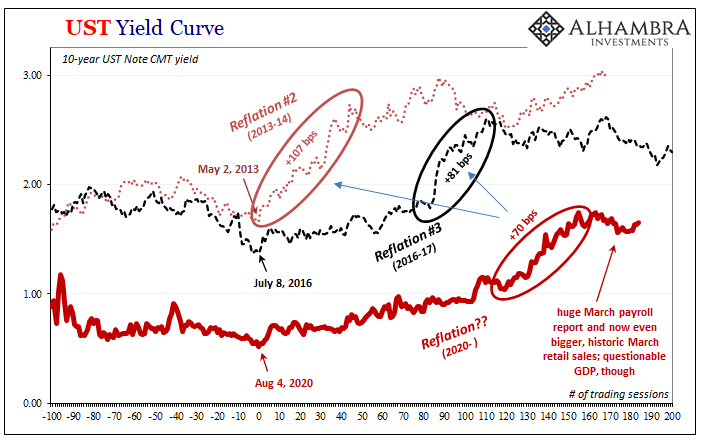

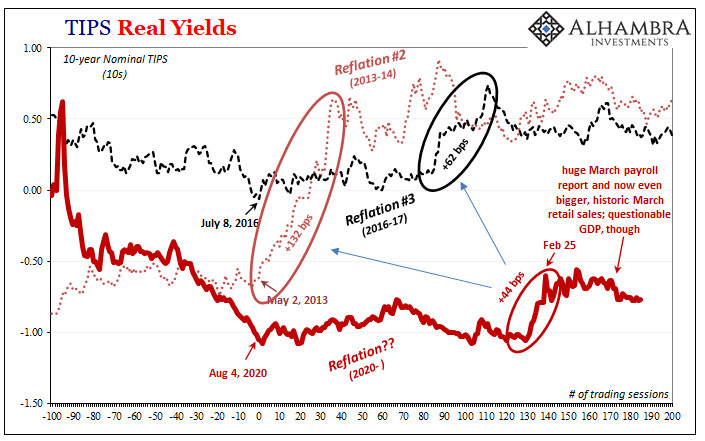

Prices continue to be exceedingly tame when, by all mainstream accounts, you’d think the consumer economy is on the cusp of double-digits like the second half of the seventies. There’s instead every reason, backed up by actual data, why bond yields haven’t budged much and, as much as it pains me to agree, Jay Powell’s view stands on a solid and reasonable basis (if only because he can and does blame COVID rather than acknowledging any part of GFC2).

Inflation comps will jump next month to their apex on base effects alone; with April 2020 being the deflationary bottom and only a minimal rebound the following month of May. Inflation is not the big problem, nor is it likely to be anytime soon.

What actually is continues to be unevenness where steadiness should have been completely installed. The US economy is to a substantial extent sheltered from the comparatively worse recession experience very visible throughout the rest of the world.

China most especially.

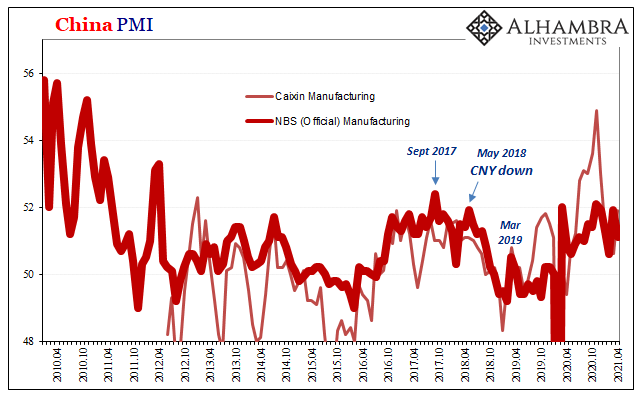

Even when their numbers are up, even way up, they aren’t actually good. Like US inflation, blatantly disingenuous interpretations of Chinese accounts are benefiting from base effects. But even in data where there are none, such as PMI’s, it is the clear lack of momentum and follow-through which stands out.

Late last night (in the US), China’s National Bureau of Statistics (NBS) reported that its manufacturing sentiment guess (PMI) dropped down to 51.1 in April. Down from 51.9 in March, this was – aside from February – the lowest since last summer. And Chinese manufacturing had been touted as one of the world’s bright spots, even if in large part due to COVID needs (things like PPE).

It’s not just the relatively low level but as much the volatility where, unlike US sentiment, the Chinese numbers can’t get all that high and even when they do manage a slight increase it doesn’t last. This is not the pattern of consistently hot economics produced by a robust global rebound.

On the contrary.

As much as America is importing goods, what must the rest of the world be doing if China’s Manufacturing PMI can barely match 2018’s highs after an immense outright recession there as well as everywhere else? And then only manage a month or two here or there at that.

This is, in fact, the very reason why that country’s authoritarian Communist leaders have developed (read: rebranded) their “dual circulation” concept (formerly “rebalancing”) – while further expounding their authoritarian nature – which outright states they expect the global economy to contribute very little even as the latter is claimed to be robustly recovering all over the place.

Li Keqiang, China’s post-crackdown compliant number two, has said repeatedly (paraphrasing) that if the rest of world ever does boom again the Chinese will gladly take it, they refuse to place their head firmly in the sand. It’s such a low probability that it isn’t worth betting the regime on a chance already proven time again to be a real outlier. This leaves China with only its own economic devices, the internal economy.

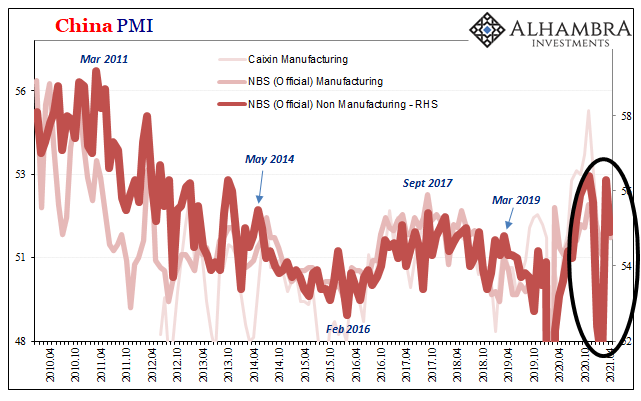

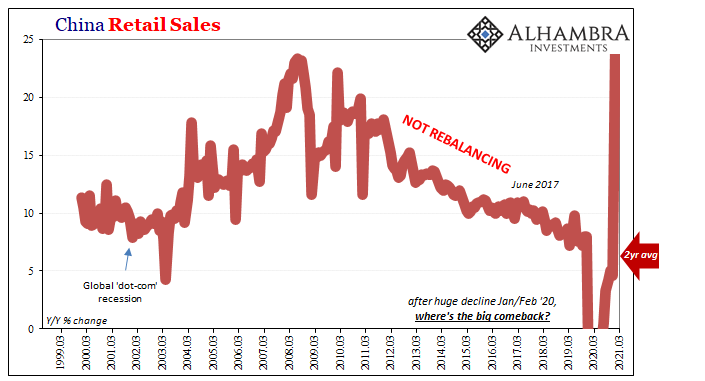

It’s not doing any better. Retail sales figures and now the NBS’s Non-Manufacturing PMI exhibiting the same volatility (from low highs) as its manufacturing cousin. The index had sprinted to 56.4 last November leaving the impression that China really was going to lead the world forward, only to collapse to 51.4 by February 2021, surging to 56.3 in March, and now back down to 54.9 in April.

To put that in perspective, this same index was around 56 in late 2013 only teasing those early hopes for rebalancing; it had been almost 60 in 2010 and 2011 the last years when China had legitimate claim to fulfilling the promises of being the world’s last economic hope for serious recovery. Nowadays, even after the biggest decline in its modern history, “sentiment” in its best months barely bests, again, 2018’s dismal highs.

And, also again, it can’t manage to stay at that comparison for more than a month.

What does one have to do with the other? US consumer prices don’t appear to have any relationship with Chinese dual circulation, or do they? Let’s ask the same question another way; why does Japan or Europe each so clearly bear the disinflationary or deflationary scars of the eurodollar no matter what “money printing” monetary authorities in either jurisdiction carries out?

It’s all the same. If the global economy isn’t going to recover fully, that’s the ballgame. What may happen is that certain parts of it, such as the US, may get a little bit further ahead than other parts, like Japan, but overall the established pattern is, well, established.

The problem with globally synchronized growth had never been the idea, no issues with the first two words of the phrase. It just hadn’t been actual growth; globally synchronized, absolutely. But if what’s globally synchronized is only reflation, and barely minimal reflation, that’s the story going forward.

It’s not that we here in America need China’s economy over there to become truly robust in order to create inflation on this side of the Pacific; it’s that if the Chinese system ever does achieve something like that we could then sincerely propose how global conditions must have changed sufficiently such that we might finally see inflation as recovery confirmation here and everywhere else.

Unless we start to honestly see globally synchronized growth then this is what we get; it’s all we’ve gotten from August 2007 onward. From tame US inflation to frankly concerning Chinese data points, why aren’t bond yields moved much at all. Rates in the US or anywhere else haven’t really changed because the rebound from COVID isn’t actually different.

Stay In Touch