Last week I was contacted by two clients seeking information about cryptocurrencies. One was my godson, 12 years old and just getting started in investing. So far, he’s bought Nintendo and Roblox (the latter against my recommendation but what do I know about video games?). But last week he said he wants to buy a cryptocurrency. He first mentioned Dogecoin but I sent him a link to an explanation of its joke origins and he laughed and said well maybe not that one. Let that sink in for a second. Dogecoin was too much of a joke for my 12-year old godson to buy. What does that say about the adults buying it? Anyway, I told him he needed to do some research and tell me why he wanted to buy a crypto and why he thought it would be a good investment. He hasn’t gotten back to me yet, but we’ve been through this with each of his previous two investments so I’m sure he’ll do the work. I’m just trying to establish good investing habits early and the most basic is knowing what you own and why.

The second person who called me was an 88-year old lady, a dear friend who has been a client for nearly 30 years. She said one of her girlfriends was trading cryptos and making a lot of money. This client is very conservative, but even she couldn’t resist at least finding out what all the hoopla was about. And she may be conservative but she’s a savvy investor. Her response when I explained bitcoin to her was, that’s it? As I said, pretty savvy; you don’t get to be a successful 88-year-old investor without a healthy sense of skepticism.

Call me crazy but I think if the cryptocurrency mania has penetrated the 12-year-old and 88-year-old psyches, it may have just about spread as far as it can. I could certainly be wrong. I’ll let you know if any 6-year-olds call me.

Speculation is rampant right now across a variety of markets. Forget for a moment why there is a lot of speculation; it doesn’t really matter. I think a lot of investors get hung up on the whys and don’t pay enough attention to the whats. The what right now is speculation and it’s everywhere if you just look. Blank check companies (SPACs) are taking companies public that the traditional IPO market wouldn’t touch, a joke cryptocurrency is up 5 times in less than a month and commodity charts have almost all gone vertical. Copper is up 12% in the last month and it’s lagging the field. I saw an article recently that argued, apparently seriously, that since the last two bear markets were so short all future ones would be too. And I saw this headline on CNN last week:

These TikTok stars built a VC firm backed by Anthony Scaramucci and the Winklevoss twins

The article is about Josh Richards, a TikTok influencer who has, with the assistance of the above-mentioned adults (a term used loosely in this case), started a venture capital fund and raised $15 million. He is 19 years old and from the pictures, I saw I’d guess he needs to shave about once a month. He’s very cute and I’m sure he has no problem getting a date which seems to be the primary driver of his TikTok popularity. He’s got killer abs too. The problem is…he’s 19 years old. Let me say that again. He’s 19 frigging years old, too young to have finished college. Too young to have experienced a bear market. Hell, too young to have experienced a correction. If an investor decides to give this lad money to invest, they deserve to lose every nickel. And if a professional investor gives any client’s money to this whiz kid, they deserve to lose a career. This is where we are on the speculative spectrum. They haven’t handed out free lunches like this since Jesus fed 4000 people with a few loaves of bread and some fish.

Stocks have been expensive for a very long time and it has been hard to stay invested or to get that way if you’ve been out. But until recently, stock valuations were high, not crazy, and there wasn’t this public fascination with investing and trading. It is the emergence of the speculative factor that has me concerned. Yes, stocks seem expensive but we don’t know what future earnings will be. Maybe we really will have a boom that lasts for years, maybe we will get another roaring 20s as I’ve seen some predict. The bond market doesn’t agree with that scenario but maybe it’ll come around to it. Anything is possible and I never try to predict the future. But the speculative frenzy gives me pause. And I think it should you too.

That doesn’t mean that I’m about to sell our entire portfolio and get long gold, bonds, and canned goods. We don’t do all-or-nothing investing here. But I do think it makes sense to start looking for the markers that generally signal the end of a bull run. For us, that means keeping a careful eye on credit spreads and other indicators that tend to act as early warning signs. It is when things look the best – and spreads right now are the tightest they’ve been since 2007 – that one should be the most vigilant. There is no sign yet that they are about to widen and they have been tighter in the past so it isn’t time to do anything yet.

One last thing to consider is that there is nothing in the economic data or markets that points to a recession right now. Not the yield curve, not credit spreads, not the CFNAI, or any of the other broad economic indicators. Bear markets are generally associated with recessions but that isn’t always the case. There have been plenty of corrections that approach 20% but never quite break the barrier to full-blown bear market. But down 19% hurts every bit as much as down 20% no matter what you call it. And with markets as overbought as they are now, what might have been a routine correction in the past may well get classified as a bear market today. Just as an example, if the S&P 500 were to drop to the 50-month moving average, a level it has visited 4 times since 2012, the total loss would be over 30%. And you could still look at that chart and call it a long-term uptrend. It’s a long way down to the long-term trend.

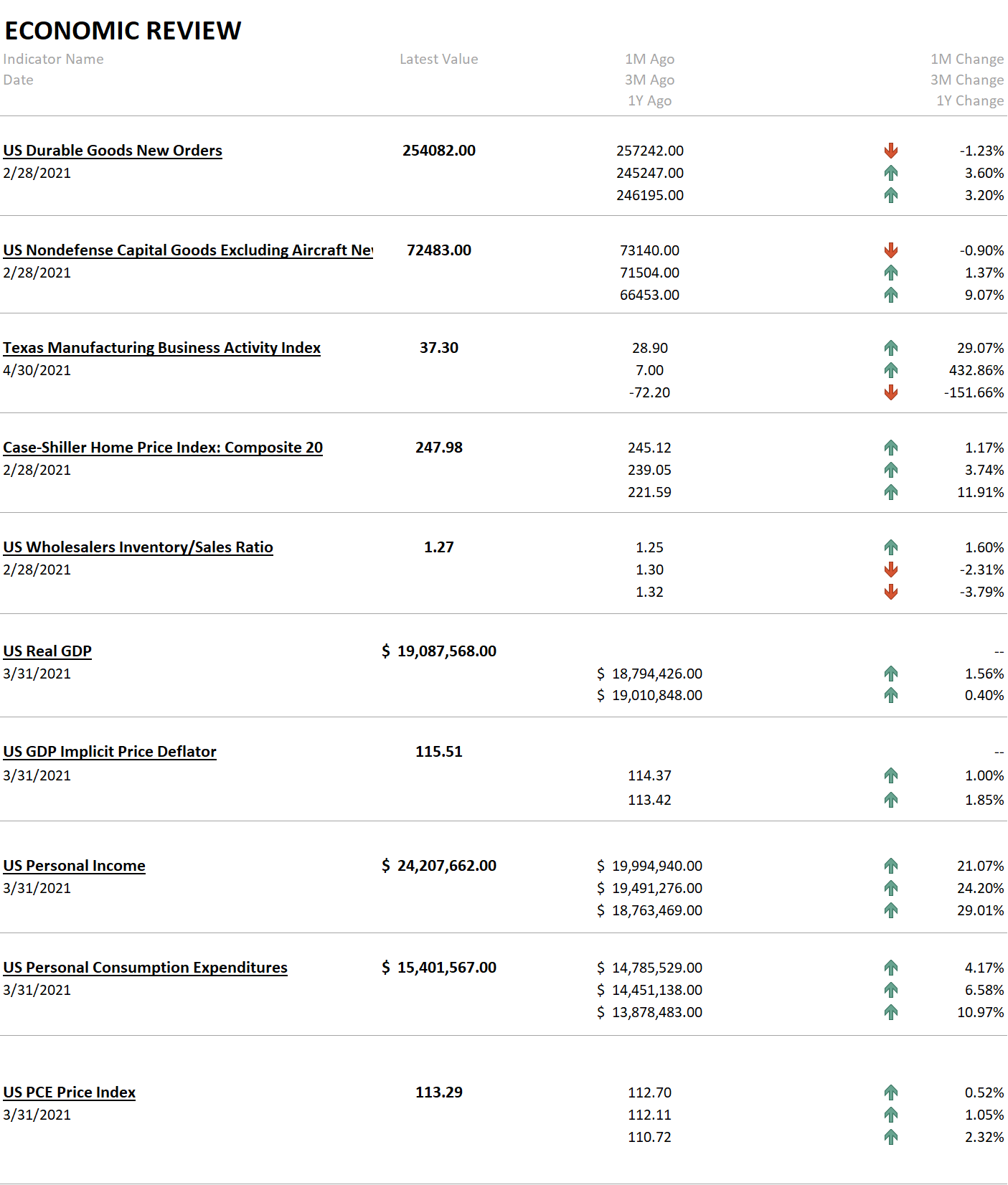

Note: Ignore the Durable Goods data below. For some reason, our data feed did not update this report. New orders for durable goods were up 0.5% in March, 1.6% ex-transportation. Core capital goods orders were up 0.9%. None of those are great although the capital goods orders were an all-time high.

The economic reports last week were generally good but that was largely expected and the market reaction was muted. GDP was up 6.4% and is now less than 1% from the peak in Q4 2019. Personal income and spending surged on stimulus payments but a big chunk of the windfall was saved as the savings rate surged to over 27%. Home prices continue to ramp higher, up 12% year-over-year but pending sales also picked up after last month’s downdraft. One disappointment was jobless claims which fell but are still in the 500s, which might explain that savings rate.

The environment is still rising growth and neutral/stable dollar. The dollar had a good day Friday and was up 0.5% on the week. It was down over 2% for the month but it continues to frustrate bull and bear alike. One thing to consider if you are long EM stocks. Absent a new downtrend in the dollar, EM is unlikely to outperform. We still have a position that we are monitoring closely.

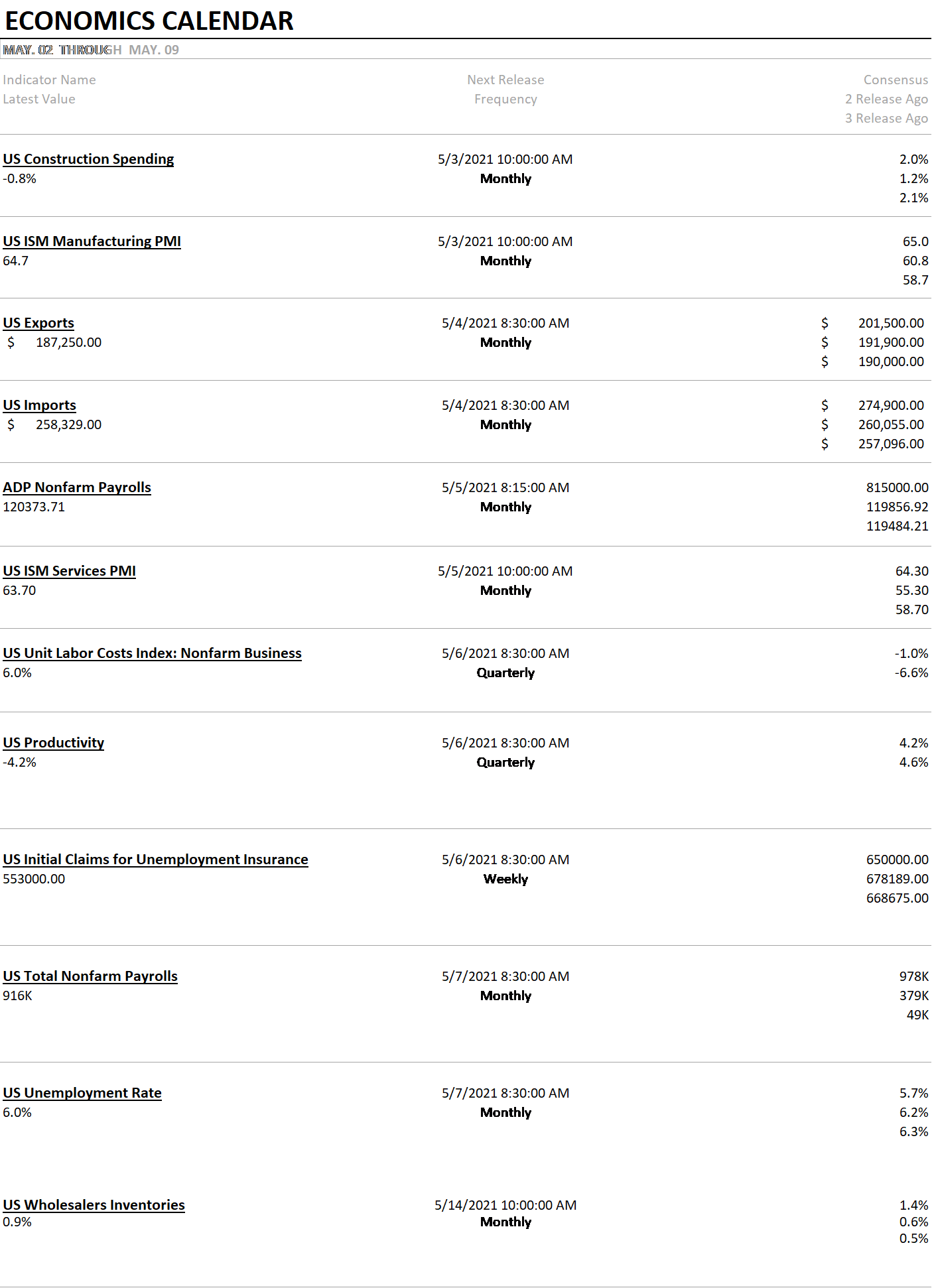

The calendar this week includes an employment report Friday where expectations are around 1MM new jobs. If that is already in the market – and I think it is – anything less is going to be hard to swallow. It will make for an interesting Friday.

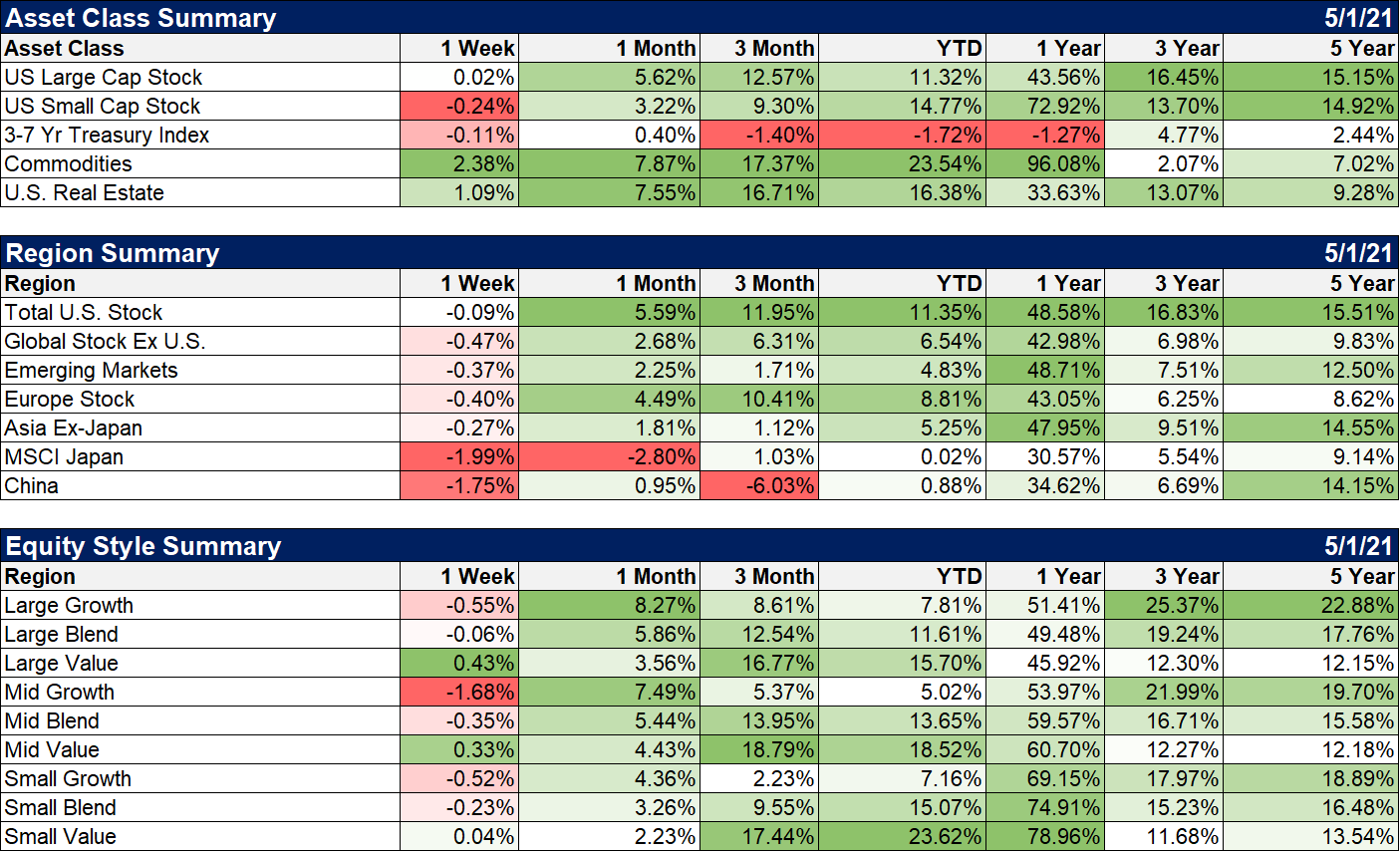

As I said above, markets didn’t react much to the data last week but commodities and real estate continued their recent outperformance. Stocks were down globally with China and Japan particularly hard hit. Value stocks returned to outperforming last week but it was a tepid move. I continue to see real estate and value (small and large) as areas that can continue to play catch up versus the S&P 500. That doesn’t mean they will go up necessarily just that they will do better than the S&P.

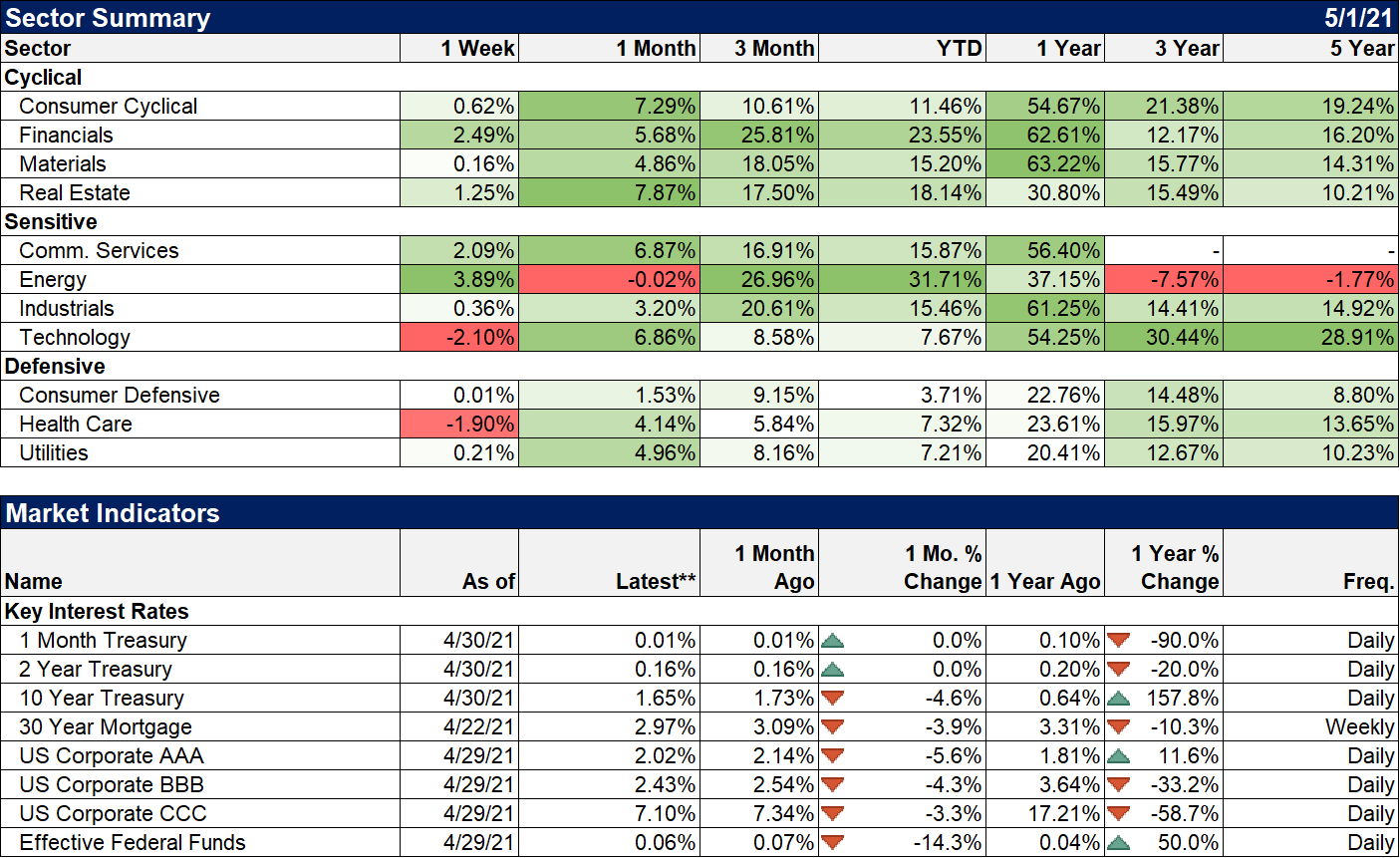

Financials and energy were the big winners on the week as you might expect when value outperforms.

So, have we reached peak speculation? Heck if I know. I’ve been doing this a long time and I’ve seen some wild markets in my time. I knew the 1999 market was highly speculative and it went further than I ever thought it would. I still have emotional scars from trying to short Yahoo in that nutty market. I knew the real estate market was crazy in 2005 but it kept going higher too. Neither of those ended well though, and I think this period is more speculative than either of those. The hangover from this, whenever, it comes, is going to be monumental. On the other hand, Jerome Powell, at least rhetorically, seems to have no interest in removing the punch bowl from this party. One does wonder, though, whether hair of the dog has a shelf life.

Joe Calhoun

Stay In Touch