He certainly is at least when compared to the usual beauty contest contenders like Bill Gross or Jeff Gundlach who typically flock to these occasions. Here we are in reflation again, so interest rates must have nowhere to go but up. Therefore, it follows, bonds are in for a world of hurt all because inflation is being let loose by a government no longer constrained by any sense of proportion.

The argument, at least, is as ancient as Buffett. One need look no further than the man’s father, Howard, who represented Nebraska in the House of Representatives in four non-consecutive terms beginning in 1943. A thorough critic of FDR’s New Deal, today he’d be classified as an inflationista and goldbug.

In May 1948, as the US consumer price index scorched upward to a better than 9% annual rate, Congressman Buffett wrote about what he saw as the inflationary aspects of a government whose payroll had reached 14,416,393 (FY 1947), up from 2,196,151 (FY 1932). And World War II was already several years finished by this time.

The natural check on such excesses hadn’t just been blunted, these had been obliterated entirely (gold confiscation). And they weren’t bond vigilantes, according to Howard, so much as aspirants to monetary soundness:

Before 1933 the people themselves had an effective way to demand economy. Before 1933, whenever the people became disturbed over Federal spending, they could go to the banks, redeem their paper currency in gold, and wait for common sense to return to Washington.

The disaster of paper money would ruin first the bonds then the currency before finishing the nation, he said. In so doing, Buffett the father would claim something Buffett his son would reiterate under similar circumstances in the far distant future.

I can find no evidence to support a hope that our fiat paper money venture will fare better ultimately than such experiments in other lands. Because of our economic strength the paper money disease here may take many years to run its course. But we can be approaching the critical stage.

The US never did, of course. In fact, the CPI’s spasm then already settling down was never more than it, and very quickly the economy and the supply-side inflation chokepoints dissipated leaving the baseline once more exposed. As for the dollar and government bonds, both equally supported by the deflationary characteristics still overwhelming even if leftover from a Great Depression by then almost an entire decade into history.

What Warren Buffett, the son, would say in the summer of 2009 was practically a reprint if painted upon a more modern background. Having the courage to equate what he called this Greenback Effect in a The New York Times op-ed with a butterfly effect better associated with the mathematics of complex systems (chaos theory) he obviously didn’t quite understand (Maybe it was just a rhetorical exercise? After all, his op-ed overflowed with awkward metaphors), oh man, so much currency cringe:

Unchecked carbon emissions will likely cause icebergs to melt. Unchecked greenback emissions will certainly cause the purchasing power of currency to melt. The dollar’s destiny lies with Congress.

Put forward in public as this grandfatherly guru, the logic – so called – in doing so goes like this: inarguably a legend in stocks, since we are all taught how stocks must be monetary, and what is inflation after all? If the guy is the premiere voice as to equities, he therefore must be the world’s foremost expert on inflation.

Except, no one who was in such a position would ever have said, “the dollar’s destiny lies with Congress.” This was his father Howard talking where both men’s views aligned with neither monetary conditions nor inflation.

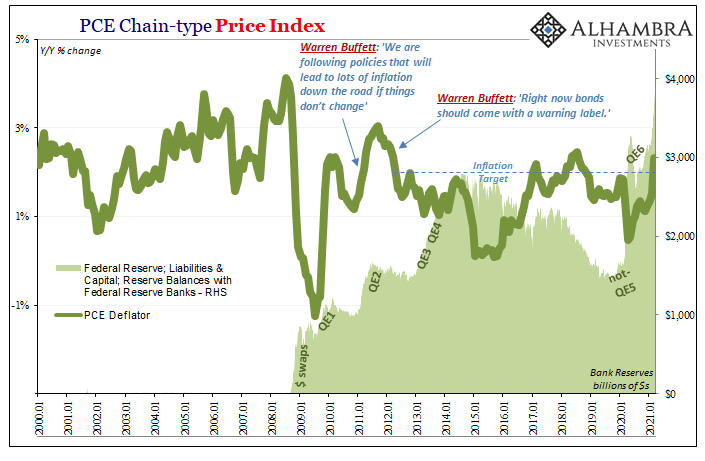

As the Federal Reserve in 2010 ramped up its “money printing” with a second QE (which should have been interpreted as a warning of continued deflation, not an inflationary excess) Mr. Buffett likewise amplified his own distaste and those same prophecies. Like Howard had said sixty-some years prior, you could hear Warren say, “just you wait”:

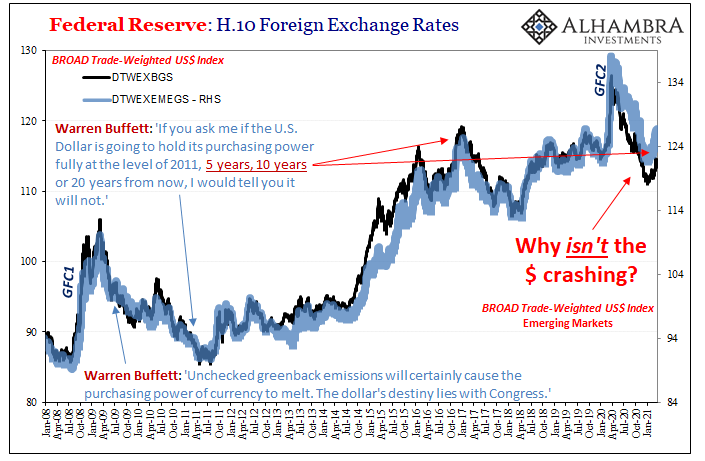

If you ask me if the U.S. Dollar is going to hold its purchasing power fully at the level of 2011, 5 years, 10 years or 20 years from now, I would tell you it will not.

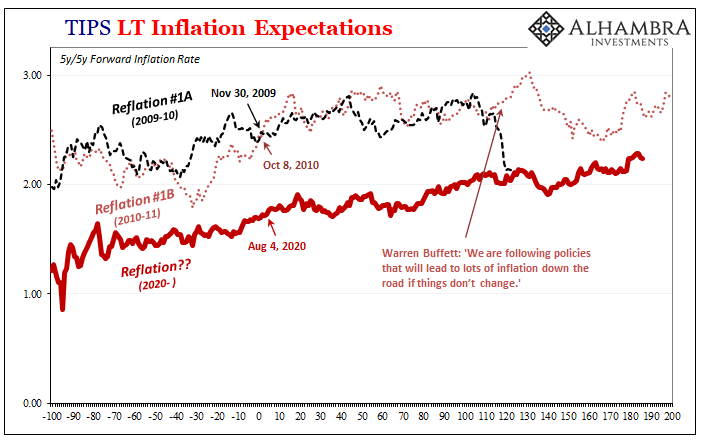

This was late March 2011, when three weeks earlier he’d already cautioned, “We are following policies that will lead to lots of inflation down the road if things don’t change.”

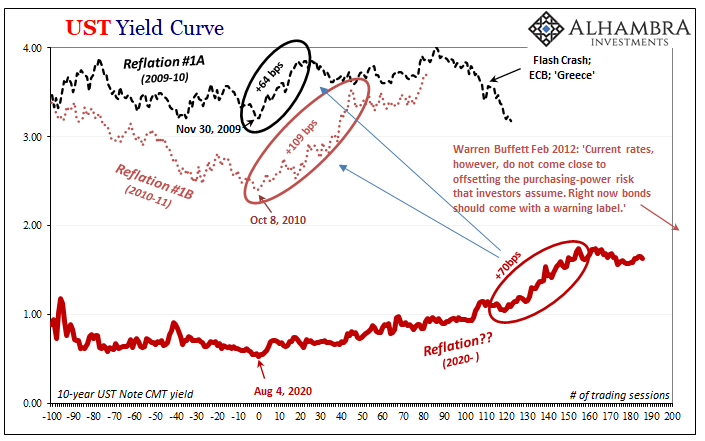

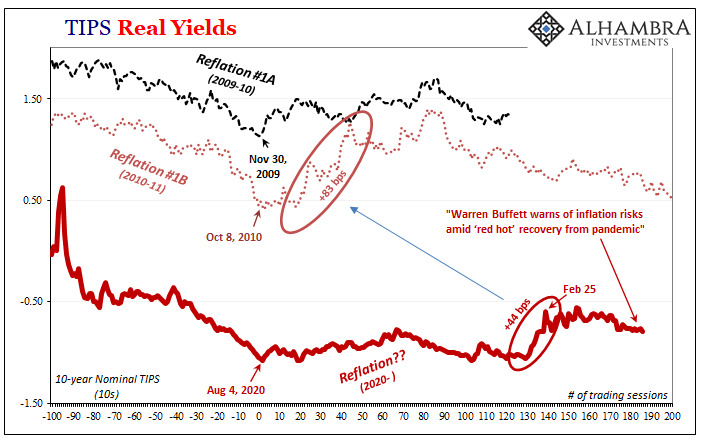

Even with the dollar moving somewhat higher rather than lower, and “transitory” inflation falling from then rather than rising, Warren Buffett remained undeterred into early 2012. In his company’s (Berkshire Hathaway) annual letter to shareholders written that February, the stock guy declared bonds, “[They] are among the most dangerous of assets.”

High interest rates, of course, can compensate purchasers for the inflation risk they face with currency-based investments — and indeed, rates in the early 1980s did that job nicely. Current rates, however, do not come close to offsetting the purchasing-power risk that investors assume. Right now bonds should come with a warning label.

The reason he gave for those low yields driving up risks was, on convention, the Federal Reserve. Everything Fed. That plus the federal government which refused to get its fiscal house in order, Warren Buffett had certainly channeled Howard Buffett to critical praise.

Science and real economy, not so much.

Rates, inflation, dollar, obviously, none of those things turned out. In fact, all three are related to the same thing which had so vexed and confused his father. The Nebraska Congressman was very sympathetically just demanding more widespread appreciation for the historical implications of reckless national finances. That much true in both cases; recklessness unmatched.

That isn’t good, but it also needn’t turn out badly exclusively in the inflationary, currency-busting sense. As we learned from the thirties, and some have started to appreciate of the global experience during the 2010’s, the specific monetary disease comes first not last.

The fallacy here wasn’t just the interest rate one, instead it was also in believing, specifically with regard to Warren, that a stock guy was the same thing as a money guy. Or that stocks somehow have any relationship whatsoever with money or even just barely resemble economic conditions as they really are.

The monetary system had decoupled from the stock market only starting in October 1929.

What that left of stocks was pretty much what John Maynard Keynes had gorgeously outlined in his General Theory (1936). The beauty contest.

We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees.

Stocks haven’t an inherent “value” so much as a social construct – no matter what the textbooks say about a “wall of worry” or “discounting mechanism.” Share prices are derived largely from what everyone thinks everyone else believes still someone else would pay. Earnings? Ha!

Which explains very well the Buffett fallacy undertaken, and, as we revisit and grossly overdo those same 2009 Fed and fed excesses, has come back around once again. In addition to blasting Bitcoin and crypto, Berkshire’s top man two days ago revisited the same inflationary thesis in commentary picked up and amplified by news media around the world despite the last decade having gone the opposite way without bothering to figure out, apparently, why it had:

We are seeing substantial inflation. We are raising prices. People are raising prices to us, and it’s being accepted.

Calling the economy “red hot”, he credited – who else? – still the same Fed and federal government for – just like 2009, or the thirties and forties – “rescuing” the system but in so doing putting it in danger of having done too much.

That may be true (at least for the federal government; the Federal Reserve, I suppose, might reach some theoretical limit for its puppet shows but that’s a trivial curiosity more than anything), but it needn’t be inflationary. It hadn’t been during or after the thirties and forties, and it sure hasn’t been since August 2007 and for countries all around the globe (global money, after all).

Both times the government (and to some extent the Fed) was able to take advantage of the background deflation to get away with what in normal times would’ve been soundly rejected by sound markets and money.

Warren Buffett may be more beautiful in this contest than Bill Gross or some other Bond King pageant contestant, and he has without any doubt earned his legendary status in stocks, yet the ugliness in real money and the real economy is not going away no matter how shares are priced.

You don’t have to take my word for it, I’m no authority on beauty; in bonds there’s no need for judges and gurus, there’s instead plenty of science and evidence stretching back at the very least to last century’s decade of the twenties.

Stay In Touch