Reopening 2 is definitely happening. The labor market, in particular, is sending off the same kind of signals if not to the same huge extent as it had during Reopening 1 in May and June of last year. The March 2021 payroll report was better than 900,000, and the one for April (last month) to be released tomorrow is expected to be in that neighborhood or better.

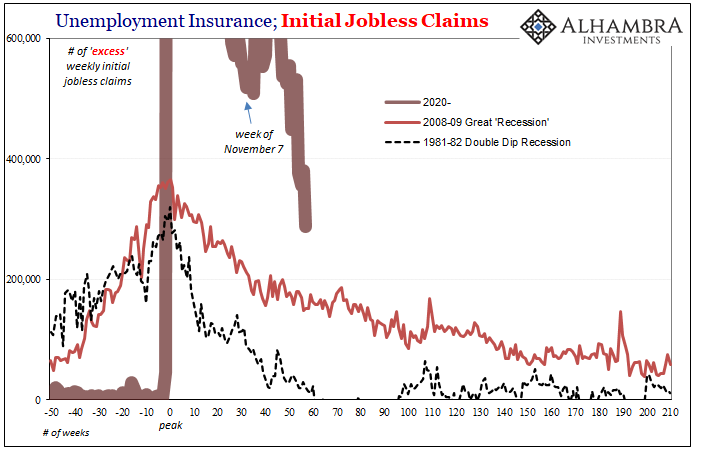

The jobless claims estimates, for example, they’ve dropped considerably since mid-April. Finally reduced to levels no longer equal to prior record highs, in the latest numbers for last week the Department of Labor believes just fewer than 500,000 initial claims had been filed. That’s a big, clear improvement consistent with the other data showing a sizable employment rebound.

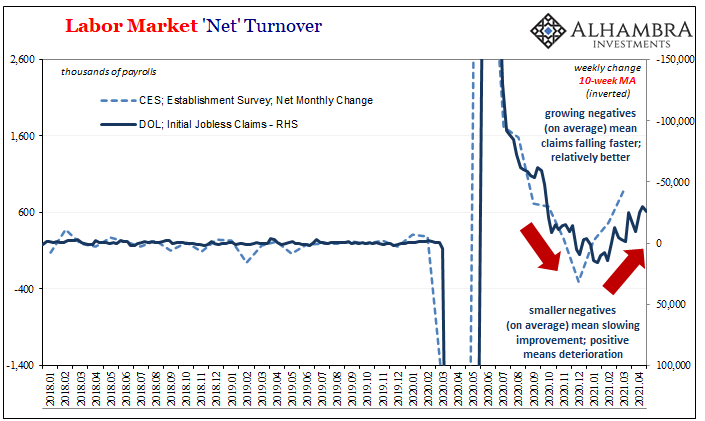

And while our approximate comparisons using jobless claims (or JOLTS) for “checking” on payrolls doesn’t quite get upward to 900,000 (more like 600,000), at this point they’re all in the same ballpark which is, again, definitely Reopening 2.

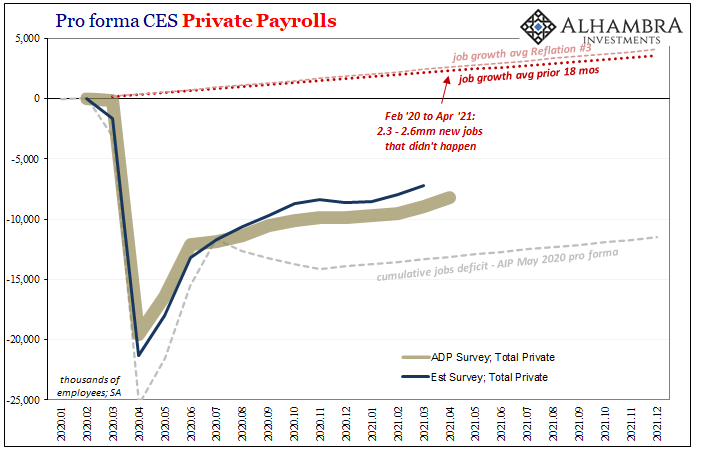

This ballpark also includes the latest ADP numbers for private employment released yesterday. Though somewhat disappointing (+742,000) compared to more robust expectations (+800,000), as jobless claims it wouldn’t be inconsistent with the same or more for private payrolls in tomorrow’s BLS jobs report.

In other words, by every measure the labor force is back on the right track at least so far as this second wave of reopening goes. Huge improvement in the numbers all around, including unemployment insurance claims which have declined for the same reasons.

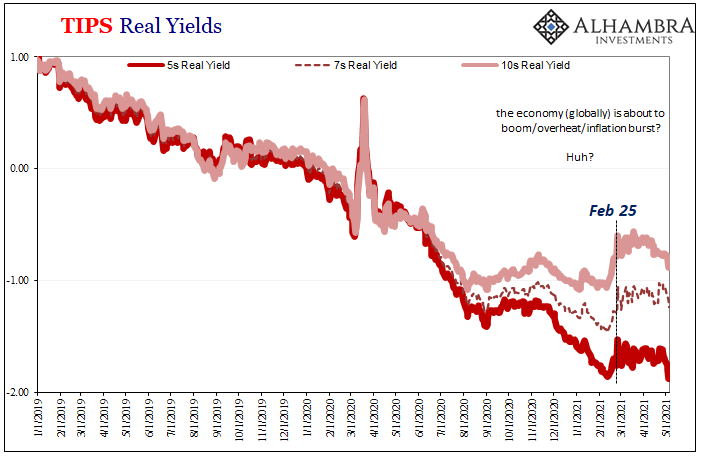

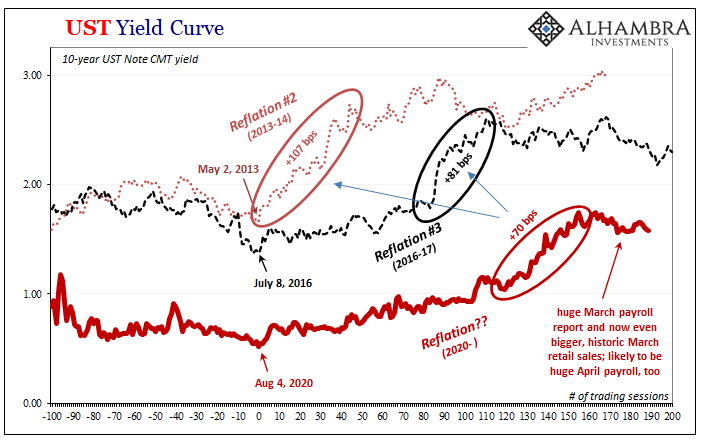

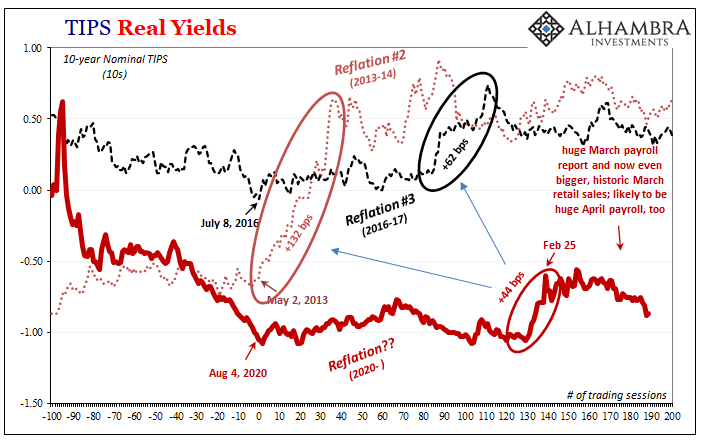

This, however, only further raises questions about the big discrepancy: bonds. Ever since February 24-25-26, at least for US “real” yields, the bond market has simply ignored one after another after another of these gigantic, rebound-affirming gains. Why?

Some will stay say – despite the mountains of central bank and academic (same thing) research conclusively demonstrating every last bit otherwise – it’s because the Fed is buying government debt (some of the same say “monetizing”) thereby depressing US Treasury yields artificially. If Jay wasn’t hugely into notes and bonds, they claim, interest rates would more closely resemble employment figures.

That’s a hard sell in the face of historical as well as scholarly evidence, even more so given TIPS real yields – a quasi-measure of growth expectations which, as you can see above and below, are and continue to be unbelievably depressed. Not only that, of late (as oil prices re-catch their pre-Feb 24 bid) real yields have gone the opposite way of what the employment rebound and especially its apparent implication would seem to have suggested.

There may be a couple factors to consider. The first, ironically, is our experience following the first Reopening. By itself, last year’s didn’t last very long (barely two months) as it was undercut by something – leaving the US and the rest of the world with instead multiple-season Summer Slowdown. Some say that was just COVID, lack of bond reflation then as now hints at other reasons.

Those may be the fact that reopening by itself doesn’t solve particularly difficult longer-run difficulties and deficiencies which may have formed by the recession and its size to begin with. In this specific possibility, once Reopening 2 runs its course, then what does the economy look like? It seems as if “everyone” has come to believe it looks like full and complete recovery (mainstream inflation certitude stemming from this).

Perhaps the bond market surveys the future as only it has been able and contrarily sees less-than-full recovery. That could very well explain what otherwise appears this reopening contradiction; no contradiction, just different periods of association.

Another factor in yields could also be the global one; that however well the US economy might appear to be doing right now when compared to the rest of the world (cleanest dirty shirt and all that) this actually doesn’t matter much at all even in the short run because over the intermediate and longer run if the rest of the world doesn’t pick up the US economy synchronizes itself with everyone else rather than the other way around.

While we focus on US payrolls and their wow factor, the rest of the global economy actually doesn’t look anything like them. In some respects, the American rebound is night and day different (see: our Southern neighbor Mexico, for one) which bodes unwell when consider the dimensions and implications of and for this global factor.

And all that is before factoring in what it was about February 24-25-26 that has kept such a stable lid on global yields in the first place.

Reopening 2 is finally here and it is good, maybe even real good. If only that was the only thing. We are still left to wonder, this far into 2021, OK, what’s next? Way too much uncertainty and risk associated with what should have been solved and answered almost a year ago.

Stay In Touch