Huge miss. Whopping dud. Maybe it wasn’t nearly that bad?

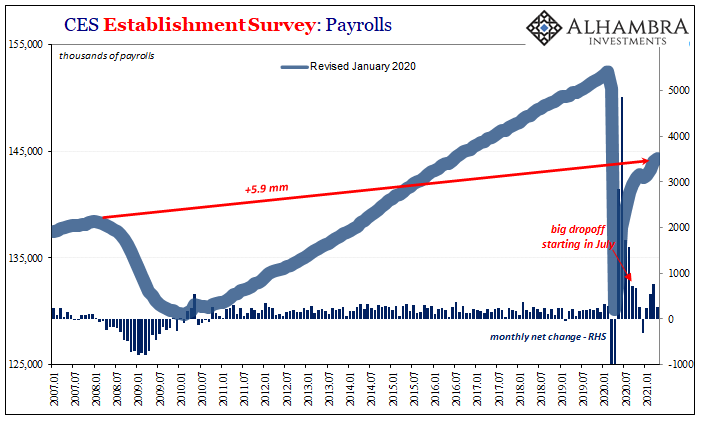

The consensus forecast had called for payroll growth in April 2021 of something like +980,000, in line with the previous blowout estimate for March. In the updated batch, first that prior one was revised downward to just +770,000 and then the latest guess put the current month at a seemingly awful +266,000. That’s the big disappointment.

While two consecutive months nearer a million would’ve been a much clearer reopening signal, taking the actual totals the average still works out to a bit more than +500,000 for both. That number is right in the same area as our informal, unscientific “model” had been suggesting based upon both jobless claims as well as JOLTS turnover mining for comparisons.

In reconciling all three data points to each other a month ago, I observed:

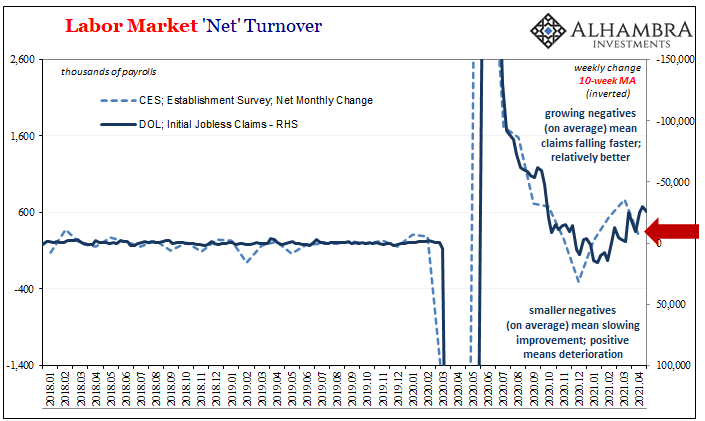

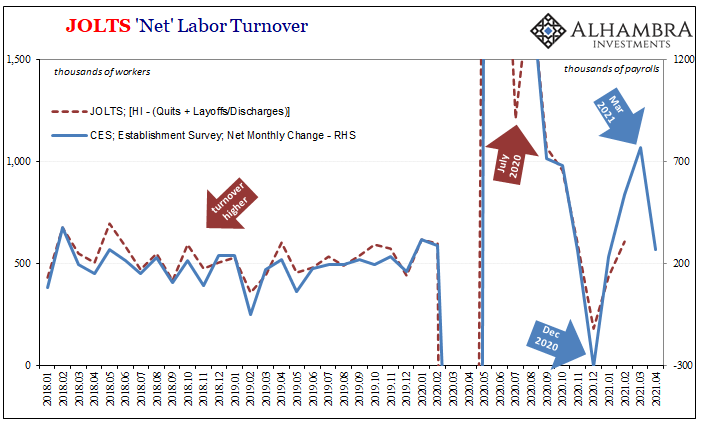

While on the surface it may seem as if jobless claims and the Establishment Survey are looking at completely different economies, they aren’t actually as far off as maybe first pictured given their respective results and how those results are changing over time. However, there does remain some level of disagreement as to the degree which imprecise estimates cannot directly solve…All three of these employment estimates show that the labor market in 2021 is absolutely improving. Two of them (JOLTS, jobless claims) pose serious questions as to whether it is enough. The other (CES) is becoming more of an outlier (at least in February-March 2021), particularly for any sense beyond simple non-economic reopening.

What happened for April payrolls (CES) is that it is no longer the outlier; it came back down into that reopening range already plotted by the others. Again, the two-month average works out close to what jobless claims and JOLTS were indicating, as I said just yesterday before the BLS threw a wrench into what had been before today clear and spectacular.

And while our approximate comparisons using jobless claims (or JOLTS) for “checking” on payrolls doesn’t quite get upward to 900,000 (more like 600,000), at this point they’re all in the same ballpark which is, again, definitely Reopening 2.

What that leaves us data-wise is now all three agree with, “pose serious questions as to whether it is enough.” In other words, even with this headline miss, payrolls are still in the reopening category if being somewhat less bombastic about it.

The rest of the data agrees on both counts; the labor market continues to be propelled by fewer restrictions while at the same time it only adds more questions about why it isn’t going so much better. The last part is more and more likely due to economic factors beyond the non-economic pandemic responses and release.

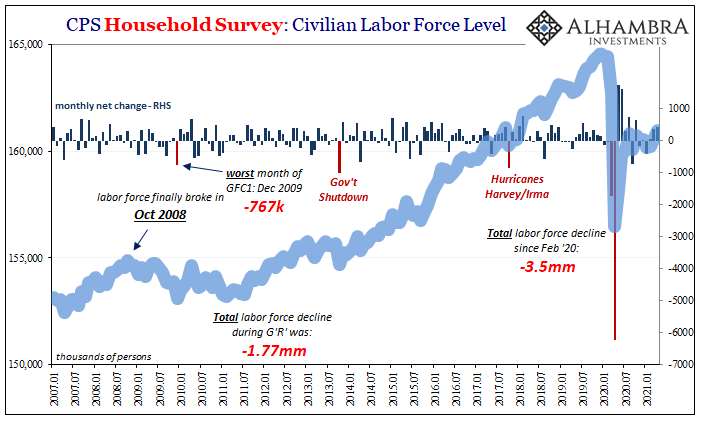

An example: the unemployment rate ticked up a tenth to 6.1% because of the simple unemployment math. The Civilian Institutional Population was presumed to have added an even 100,000 in April from March, while that new hundred thou plus 330,000 entered and re-entered the labor force; LF rising by +430,000 in total. Of those, 328,000 reported (Household Survey) to have found or returned to a job while the remaining 102,000 were classified as unemployed and added to the 9.7 million from March.

Because the 102,000 more unemployed went into the much smaller numerator and then divided by the much larger labor force denominator, even though it added the full 430,000, the net result was a seemingly negative result, the unemployment rate going up a fraction.

But that increase in the labor force was the largest since last October (participation rate rising 0.2 points), as we’d expect with a looser, friendlier labor market month. Even the 102,000 jump in those classified unemployed meant that many more Americans began looking for work again even if last month they couldn’t (yet) find it.

The alternate metrics of “hidden” unemployment likewise all improved where the main unemployment rate did not. The U-6 rate, for instance, dropped from 10.7% in March to 10.4% in April primarily because the estimated number of workers who would report being stuck in part-time jobs for economic reasons declined sharply (by nearly 600,000 in just this one month).

But – and you knew there was “but” – the fact that these numbers are as limited including the big headline miss once more indicates that beyond reopening, the actual underlying economic growth which ultimately matters here, there’s just not much more of it.

The major economic sector most affected by the non-economics of pandemic politics has been the leisure and hospitality of the luxury service economy. With those establishments granted more operating windows in various states and locations, waiters and bartenders made up more than half (+187,000) of the overall April pickup. Another 127,000 at hotels, gaming places, amusements, and other recreation-style businesses.

Like a few months ago, just about all the job gains of the non-economic variety.

On the other side, in professional and business services, the tally of temporary workers dropped by a substantial 111,000 (as more typically happens during any recession rather than recovery phase) while business support services apparently shed 15,000. Add to those an 18,000 decrease in manufacturing workers (despite red hot goods) plus a 15,000 drop in retail trade employment and then no change in construction (all seasonally-adjusted monthly changes).

Non-economic: good not great; economic: wait a minute.

If anything, the resulting volatility in the headline rate adds more to existing (bond market) doubts as to whether all of this will be enough. What’s really going on and what the economy looks like once the pandemic and the disruptions directly caused by it, all finally end.

For the overheating, red hot, inflation-is-the-primary-danger-because-the-economy-is-not-just-recovering-it-is-on-the-verge-of-rolling-boil, that’s where answering those questions will apply first. It may be that the economic disappointment to April’s payroll figures are transitory, a one-time (though this isn’t the first time) slip, or instead perhaps an indication of the American side of global economy factors.

Either way, we’re right back to last year. Reopening is good, but that’s just never enough by itself. And if reopening while good isn’t nearly so good, certainly not quite as good as it seemed yesterday, then that tracks into the territory of more purely economic circumstances.

Because of this, you should expect to see a whole lot more mainstream stories, a ton more going forward, each and every one writing up anecdotes about which will assert the return of the LABOR SHORTAGE!!!! to “explain” all this. The inflation case demands nothing less; if there are questions in labor numbers, and there are a bunch, just like 2017-18, then it must be that businesses can’t find enough workers. I’m sure there were a few published already today to respond in kind to the big headline miss.

Stay In Touch