Awash in “stimulus”, but none able to dent a semiconductor shortage which is purportedly the reason for production woes. In the US and many other places around the world, governments have gone nuclear, with America’s federal authorities dropping checks with abandon. This has created, according to some, everyone in the media, a red hot economy right on the verge of massively overheating.

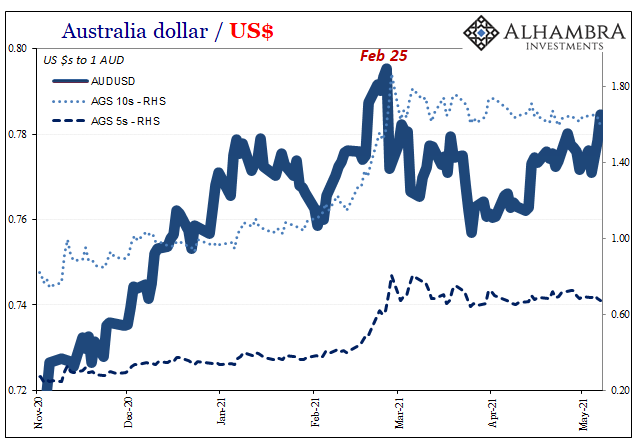

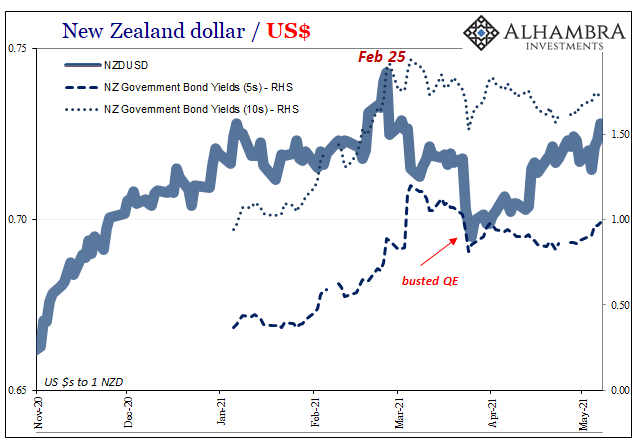

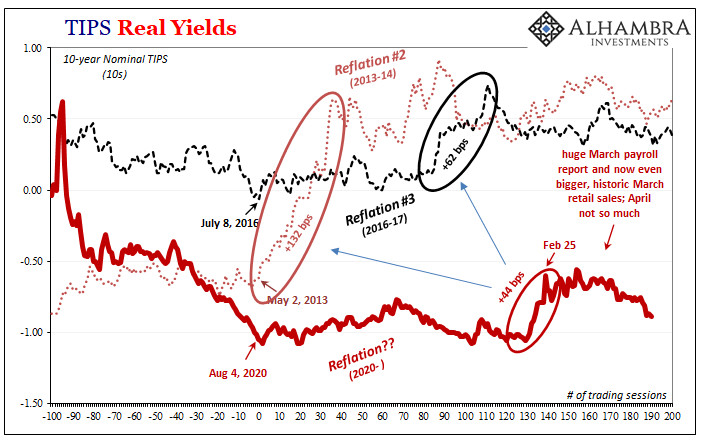

Bonds just aren’t buying it, and that was long before today’s payroll report. The US goods economy might be experiencing a sugar rush, that’s not the whole ballgame. In addition to services, there’s a global factor underlying the non-reflationary global yields of late (often synchronizing them before economies).

For all that is purportedly going right domestically, if there are planetwide considerations embedded within major interest rates regimes there’s any number of sharp contrasts by which to measure the relative relevance of that single segment in the single economy. To that end, we needn’t look far from our borders to find evidence for the less-than-fiery element(s) to the bond skepticism.

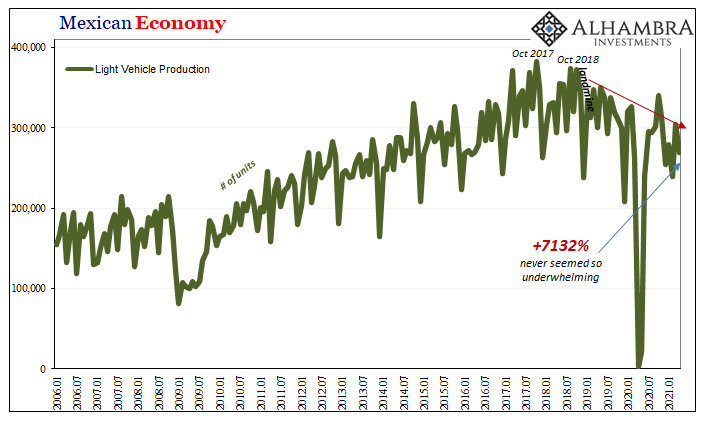

Mexico.

Never has a 7132% annual increase come up so small. Yet, according to Mexico’s Instituto Nacional de Estadística y Geografía (INEGI) light vehicle production during the month of April 2021 totaled 269,180 units. Back in April 2020, when Mexico’s carmakers had decided to shut it all down near completely, the number was a bit lower, 3,722 in the final count.

The difference, a better than 7000% annual gain which doesn’t tell us all that much. Instead, compared to April 2019, production levels were still more than 10% short; that’s a pretty sizable gap for the boom.

This is where the semiconductor bottleneck gets inserted; of course production is still down, it’s been said, because global producers in Mexico like everywhere else can’t get enough chips to complete assemblies.

Of the major automakers, only Honda (that I’d been able to find) had gone so far as to announce full shutdowns disrupting its schedule. On March 17, the company said it was furloughing its Celaya plant offering a variety of reasons:

The company said that decision was made because of the lingering impacts from Covid-19, congestion at various ports, the global semiconductor shortage and severe winter weather over the past several weeks.

Cold in winter, why throw that one in here?

At the time, the spokesman said that during April the company would make up for any lost production once one or all those things cleared up. Honda in early April, the 5th, announced that all its North American plants would reopen including the one in Mexico.

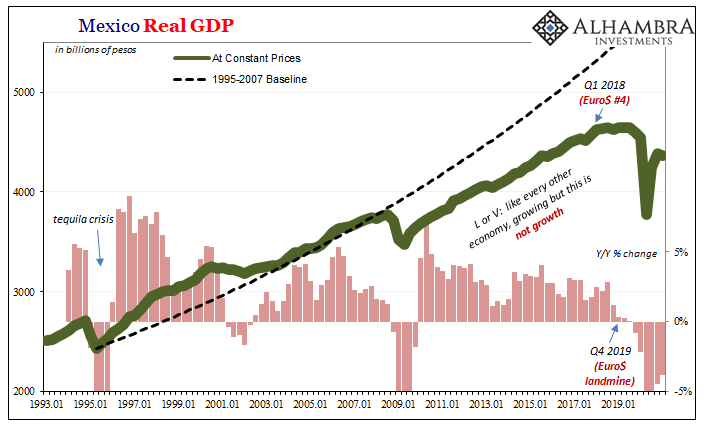

There had been any number of similar type excuses offered for the same sort of manufacturing weakness the several years before 2020’s COVID arrival. The fact of the matter in Mexico, like a whole lot of other places around the globe, is that the 2020 recession merely extended and worsened a relatively severe one already a year or more old.

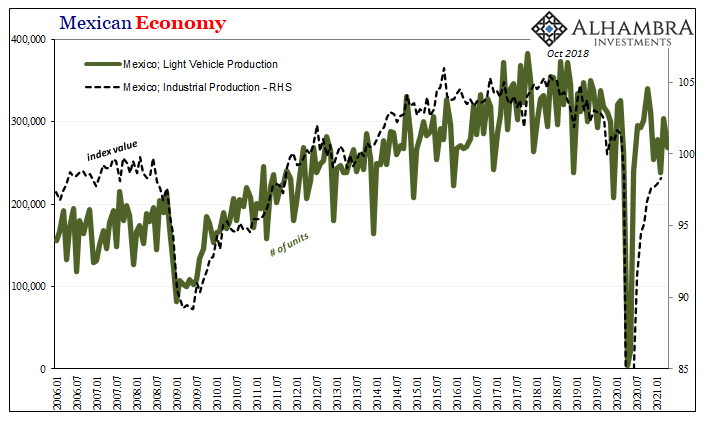

You can see it in Mexican autos, a key contributor to overall industrial production which itself heavily influences the overall direction and intensity of Mexico’s entire economy.

Even if Honda or any others had been able to find sufficient semiconductor supplies, how much would they have added to production volumes during the four months of 2021 so far? Getting back up over 300,000 steady would certainly help the ailing system, but would still reflect the prior trend and “whatever” it had been driving the Mexican economy south for all that time beforehand.

This “whatever” might therefore still be the unsolved wrench in the machinery of exchange.

It makes for quite the contrast: the US goods economy is juiced up by Uncle Sam, while normally many of those, perhaps too many, who produce much of those goods aren’t deriving the full benefits from it even if imports into the US have surged.

From the local side of the border, in a very narrow context, inflationary prospects might seem legit. On the other, the same deflationary weakness which had thwarted and confounded (for reasons never explained) the previous inflation story just a few years ago (now long forgotten in fleeting mainstream memory).

Sure, here is just one instance but Mexico is hardly a lone anecdote, an outlier. That’s the point; global factors even if supply chain related, looking around beyond the transitory reach of Uncle Sam’s helicopter you quickly and easily find and figure out it is the US goods economy which is the outlier.

Stay In Touch