It was all over the news last week. Inflation has arrived. The CPI was hotter than expected. The PPI was even hotter. Import prices were up and export prices were up more. It was impossible to miss the inflation story last week. Stocks got the message and sold off on the hot CPI and finished the week lower for a change. Or at least that’s what I read in the press.

But curiously, there were two markets that didn’t seem to get the message: bonds and currencies. If investors were really worried about inflation, there is one really obvious thing they would do – buy TIPS, inflation-protected bonds. And yet, with inflation readings providing all kinds of headlines, investors didn’t do that. In fact, on the day of that much higher than expected CPI, investors sold long-term TIPS, the 10-year yield rising by 4 basis points. If inflation fear is driving markets, TIPS investors are curiously brave. Nominal bond yields also rose on the week but the 10-year breakeven inflation rate actually fell by 3 basis points. Yes, in a week defined by the financial press as being dominated by inflation fears, investors with actual money on the line demonstrated nothing of the sort. On the currency front, the dollar was up the day of the CPI print and on the week as a whole. Real inflation is not just rising prices but rather a loss of purchasing power, most easily observed in a falling currency. The dollar has been volatile this year, up about 5% through March and down about 4% since, but it is not falling as I would expect if inflation was really going to be a long-term problem. That could change but for now, if the dollar doesn’t fall, then this “inflation” will likely prove, to use the word of the year, transitory.

I don’t think you can even call this a buy the rumor, sell the news event. It isn’t like bonds had sold off recently and then didn’t react to this “news”. The bond selloff that started last August accelerated earlier this year driving the 10-year yield all the way up to 1.76%. But more recently, bonds have been moving the other way, the yield falling back to the 1.58% level. The move back up to all of 1.64% last week just isn’t enough to even warrant a comment except to say it isn’t worthy of comment. Bonds may indeed continue to sell off over the coming months as the recovery continues. That recovery though has been all I expected, advancing in fits and starts rather than the boom everyone else has been talking about. The emerging consensus seems to be that it would be a boom if the supply side of the economy would just get its act together, if all the lazy bums would get off the dole and on the payroll. Maybe. Or maybe people are just acting a little more conservative – especially with their money – after their near-death – or worse – experience of the last year. Yes, I know social activity is on the rise these days after being freed from the tyranny of the mask but my concern all year has been that we’d get a short burst of activity that faded quickly. It is way too early to be doing victory laps on that score but I do think there are still some holes in that post-virus boom narrative.

There are indeed a lot of jobs available if the JOLTs report is to be believed. And the employment situation is improving slowly but I’m not sure the pace is all that much affected by the extended and generous unemployment benefits. If you remember all the way back before the virus, there was a vigorous debate about the skills mismatch. There are a lot of job openings for which there are a limited number of qualified applicants. I do not believe that a year of on and off shutdowns has changed that situation. If a skills mismatch existed prior to COVID – and I realize that is debatable – it still exists.

There are, however, a lot of service jobs available right now as bars and restaurants open up and there is a limited appetite for that kind of work right now. But those jobs will get filled eventually by people who haven’t used their downtime wisely to gain more skills. Or by new entrants to the workforce. And even with high demand for their services, I doubt these workers get a pay raise out of this. If restaurants are forced by legislation to raise their hourly wages, they will find ways to recoup that cost. They’ll either capture part of the tip revenue or raise menu prices or some combination. Restaurants are already low-margin businesses and can’t just eat wage hikes through lower profits. I don’t think we should be looking to restaurants, bars, and other service industries to solve our employment problems (if indeed we have a problem; a long discussion for another day).

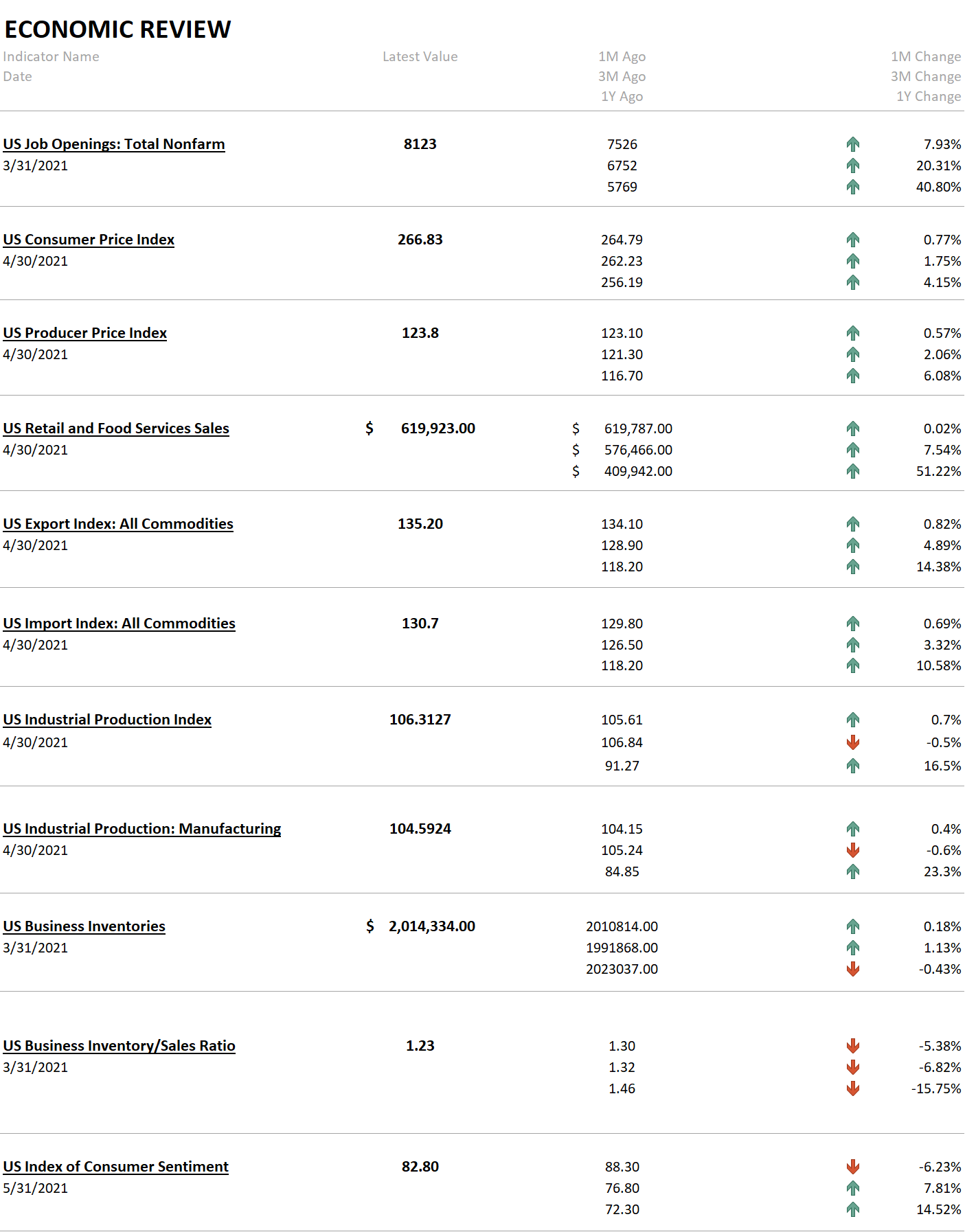

With the exception of the aforementioned JOLTS report – job openings up nearly 8% over the last month alone – most of the economic data released last week was not that great. Obviously, the inflation figures were hot but taken into context they are not a problem, certainly not yet. But they do represent I think a headwind to growth as higher prices do what they usually do and reduce demand. Indeed the last report of last week supports that view as Consumer Sentiment fell precipitously from last month. That is exactly what we should expect with volatile prices and uncertainty around inflation. There’s even a name for it – the Katona Effect, which posits that as price volatility increases, consumers spend less and save more and vice versa. It is named for the man who developed the consumer sentiment survey at the University of Michigan, the very survey that appears to be bearing out his hypothesis. The good news is that if the dollar holds up and prices stabilize, consumers should step up their buying.

Two other reports warrant comment. First, industrial production came in weak again, a trend seemingly at odds with much of the other economic data. Jeff wrote about it earlier in the week and made some good points, namely that today’s IP level is actually less than 2014’s reading. There are obviously some issues in industries hit by supply shortages but I think the main culprit (which Jeff notes too) is oil production. I am not opposed to oil production but I’ve warned repeatedly over the years that relying on shale oil production for economic growth was not a good idea. It is true that overall IP levels today are no higher than in 2014 but the more shocking fact is that manufacturing IP is no higher than 2006 and less than 10% higher than 2000. Real estate and then fracking covered up a lot of our economic problems over the last two decades. Real estate is still booming and may still for years to come. But fracking is a different story I think. Too many lenders have been burned in the shale patch and it will probably take much higher prices to lure them back.

Second is the business inventory report which on the surface seems like no big deal, up just over 1% in the last three months. But the big news here is the inventory/sales ratio which fell to an all-time low of 1.23 in data going back to 1992. I suppose you could see that two ways. Either businesses are not willing to stock more inventory because they don’t think they’ll need it or they can’t rebuild inventories because of supply issues. Neither would seem to be good for near-term growth. It is typical to see this ratio fall after a recession. It is also fairly common before recession but we don’t have any other recession indicators pointing to trouble right now. And so, it seems more likely that inventory building could become a source of future growth but I think it will take time for both consumers and producers to recover from the shock of the last year.

The economic environment is unchanged again this week with growth improving and the dollar neutral. But both of those observations are under great scrutiny right now. The economic recovery is not exactly struggling but it appears it will be a choppier, more drawn-out affair than most assumed. But again we are interested in whether things are improving and right now they are. As for the dollar, it is again near the bottom of that range it’s been in for over a half-decade. If it breaks down there are major implications for investors and I don’t think most of them are prepared.

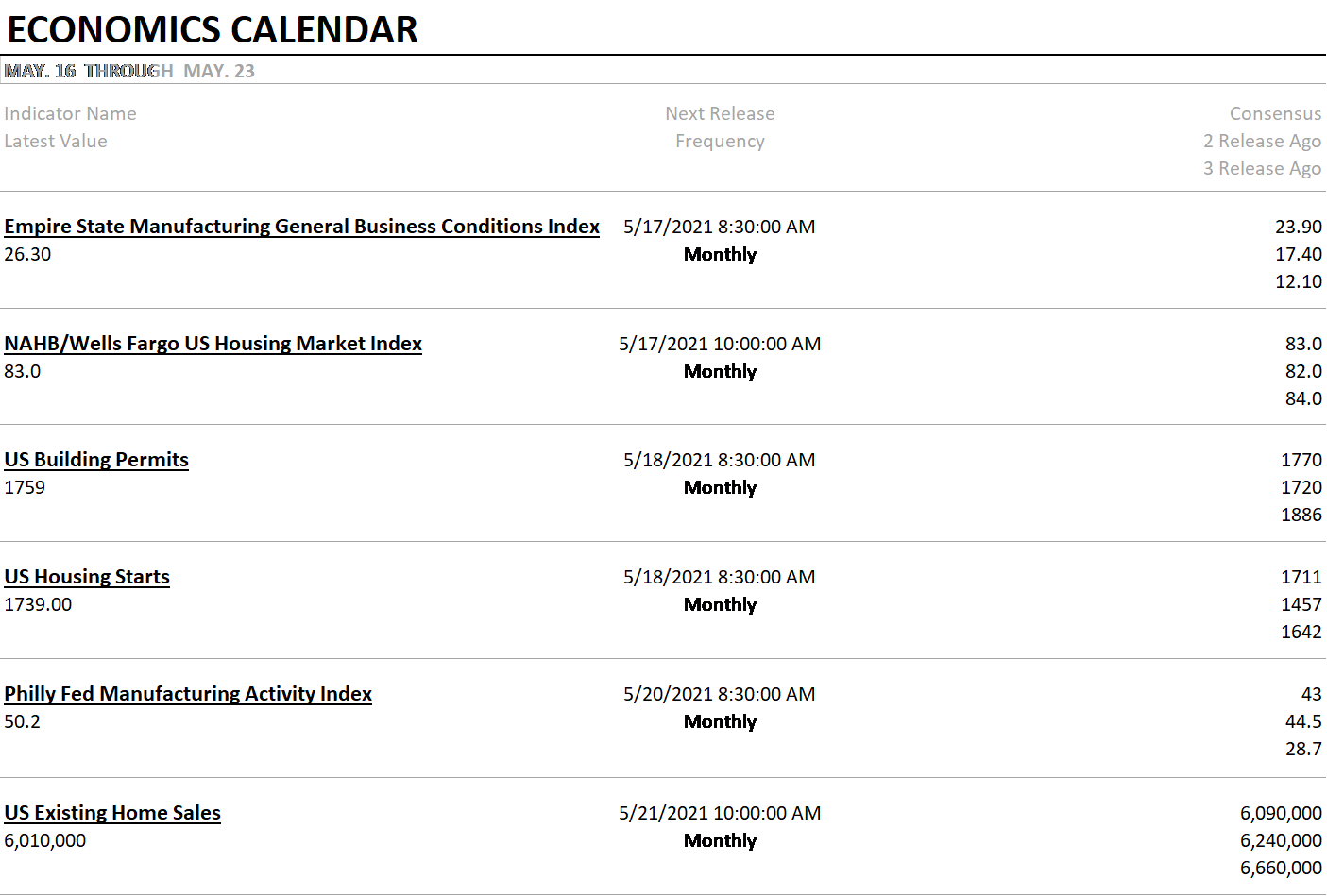

Next week’s calendar brings some Fed surveys and housing data. The Fed surveys are nothing more than sentiment surveys so I don’t put much stock in them but others do so they can be market movers if they are way off expectations. With most of these surveys sitting near all-time highs, I’d suggest that maybe a disappointment wouldn’t be that surprising. As for the housing market, I see no reason to expect much of a change in the short term with inventories as low as they are. If inventories rebuild quickly, prices might stabilize. If not, they probably won’t.

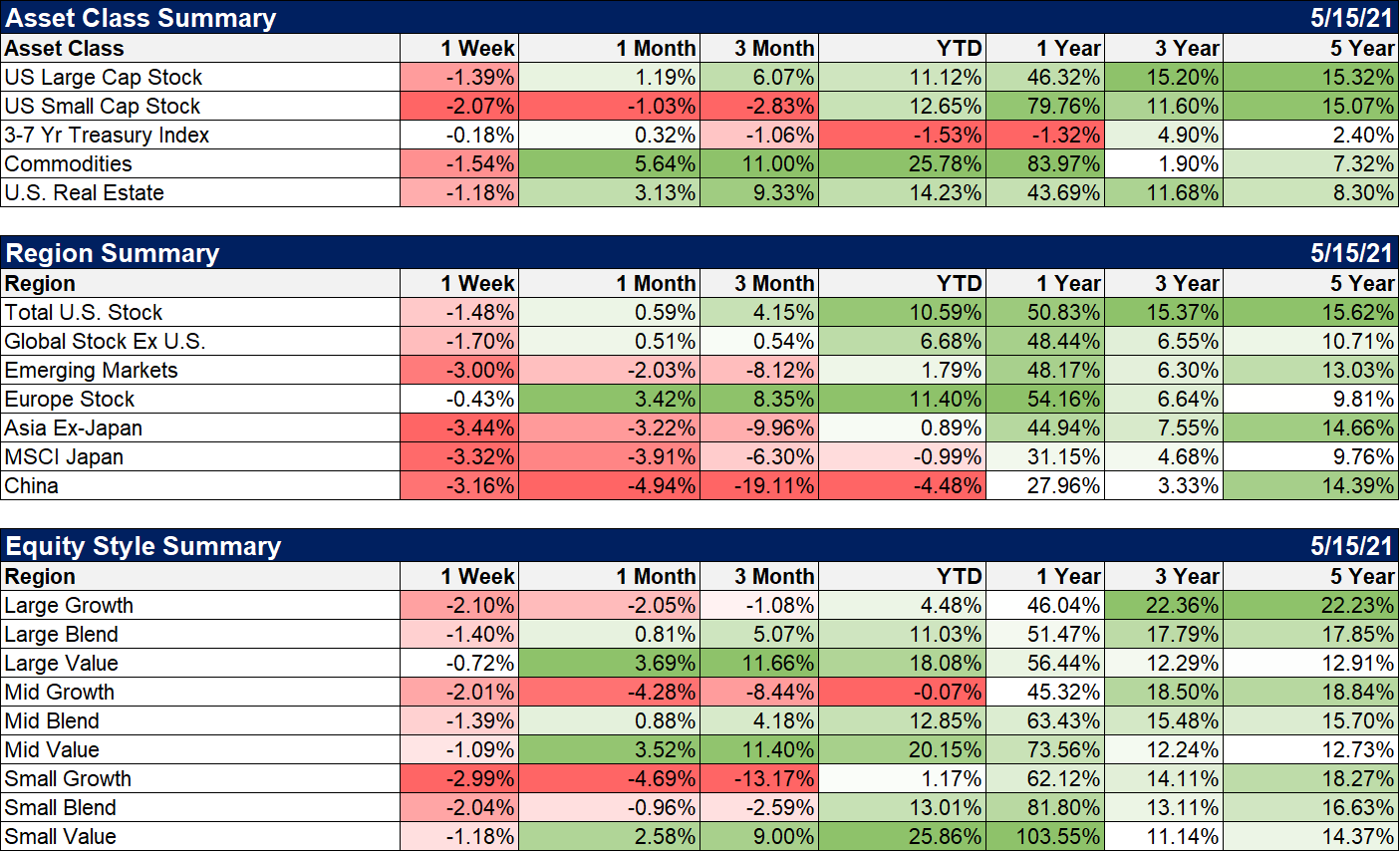

As I said, stocks were down last week although it would have been a lot worse if not for a big turnaround at the end of the week. Value continues to outperform but it was down too last week. International markets were generally weaker than the US although Europe managed to beat. Of note too is the recent strength in Latin American shares (not shown below). The ETF for the region, ILF, was actually flat last week and outperformed the S&P 500 by 1.25%. That continues a short-term trend that started at the beginning of the month. We recently trimmed our EM exposure but that was more about Asia (China) than anything else. I am intrigued by the region and Brazil if the dollar does get in a more sustained downtrend. Sentiment on the region is in the bano and the Real, Mexican Peso, and Chilean Peso appear to have stabilized. Here’s a thought experiment: how would most people react if you told them you were buying Latin American stocks? I think you know the answer to that. Interesting isn’t it?

I don’t include gold in this weekly chart but it does deserve a mention this week. Commodities were down last week but gold managed a slight gain. Gold started a weak uptrend against stocks in April (that may be accelerating) but it now appears to be turning higher versus the general commodity indexes. That is interesting and could be pointing to a slowdown in economic activity. It could also be an early warning that the dollar is going to break through the bottom of that long-term range. I really don’t know what it means yet except that it really bears watching.

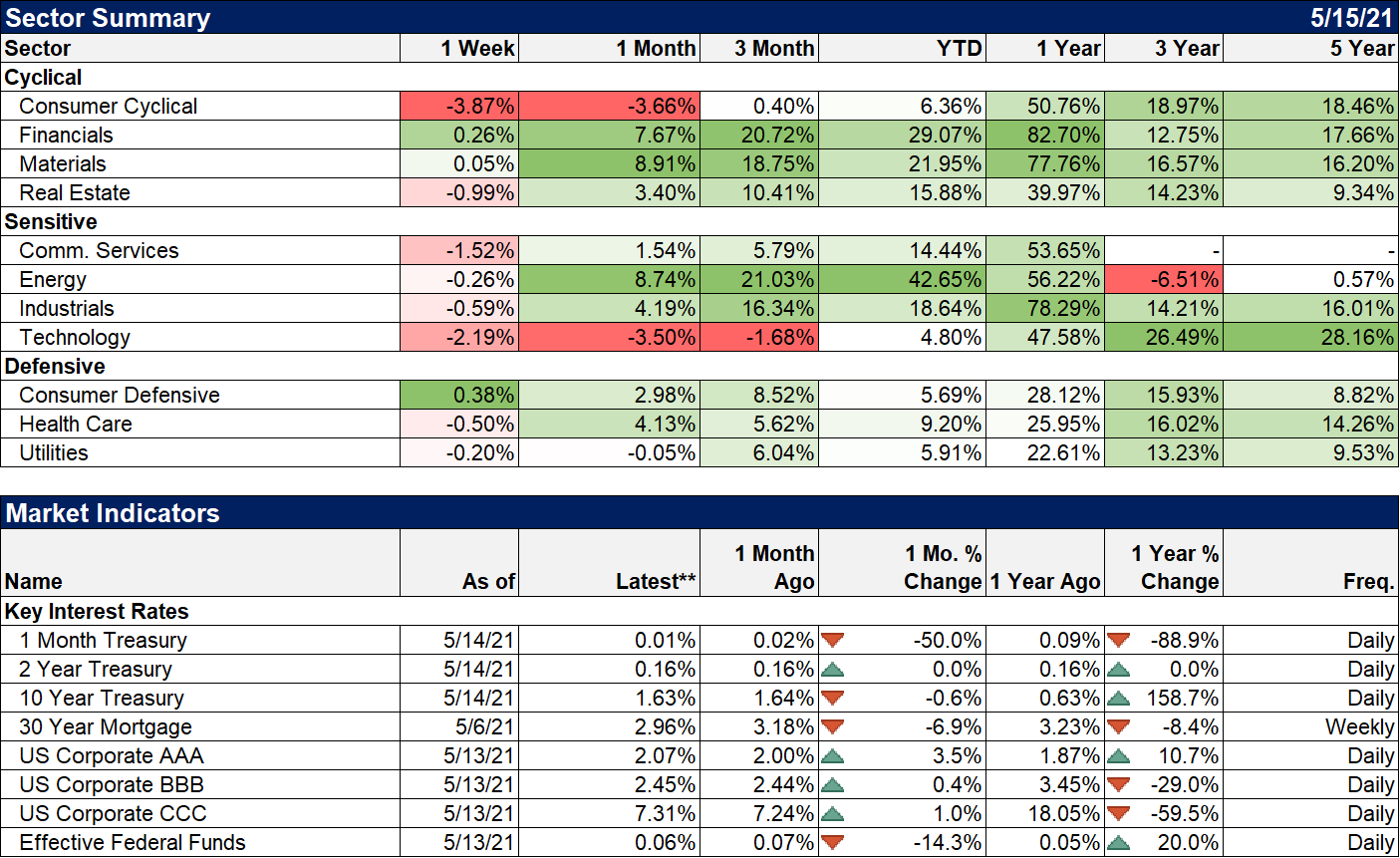

Kind of a confusing picture in the sectors. Cyclicals were down hard but financials and materials, also economically sensitive, were up. Consumer defensives were up to which I think puts the win in the economic slowdown camp. But one week does not make a trend so we’ll have to wait to see if this means anything. My guess is no.

Prices rise for lots of reasons but inflation is not about just some random price hikes. Inflation is a sustained drop in purchasing power, a fall in the value of money. A falling dollar has investment implications way beyond just what might happen to bonds or TIPS. And if there are market/investment implications there are also economic growth implications. And in the end, while most economists fret about deflation, it is after weak dollar periods we are most vulnerable. The weak dollar of the 70s and its implications are well documented but I’d just remind everyone that the S&L crisis followed the massive devaluation of the dollar in the late 80s. And of course, the 2008 banking crisis was preceded by a weak dollar period that ran from 2002 to mid-2008. It is the rapidly rising dollar periods (deflation) we fear because they indicate a lack of global dollar liquidity. But it is those weak dollar periods, when investment is diverted to real assets from intangibles, that leads to the sub-par growth periods that follow. That was true in the early 90s and obviously over the last decade. A strong and stable dollar is exactly what we need to induce recovery. As I look at the trajectory of economic policy in the US – monetary and fiscal – I fear we won’t get it.

Joe Calhoun

Stay In Touch