We got another disappointing employment report last week. Well, that’s what everyone said anyway, that the complete WAG by the BLS that the US economy added 559,000 jobs in May was below expectations and disappointing. I suppose it is a tad disappointing but I find it hard to lament the fact that a half-million Americans found jobs last month. There are strange things going on in the labor market right now and I don’t think anyone really knows what will happen over the next few months. For a while, there was this expectation of a boom as everyone went back to work and play but that seems to have faded with the reality of this recovery from the biggest supply shock in history. Everyone seems to still be thinking of this as the standard recession and recovery cycle just like all the others we’ve had in my lifetime and my father’s too. But it isn’t and we shouldn’t be expecting it to stick to the script written for the demand-led recessions of the post-war period.

My wife and I enjoy fine dining and we are lucky to live in a small town with a plethora of options. Our town is a unique place with an official permanent population of about 30,000. But the non-permanent population is what makes it more than it appears on the map. It is a major Thoroughbred winter training center and the home of the Thoroughbred Racing Hall of Fame. We also host multiple major steeplechase races each year as well as numerous show jumping and dressage competitions. The oldest polo league in the US is here and the second oldest golf course. The main polo field is named after the founder whose surname of Whitney is more often associated with a certain Art Museum in NYC. And Julliard has a presence here in association with the Joye Cottage (owned by that Whitney and then a Vanderbilt), a bit of a misnomer since it is the largest private home in the state. Point being, there are a lot of wealthy people here and they want fine dining. So, for a town of 30k, we have more than our fair share of good places to eat.

I bring all that up not to brag about the town where I grew up (and am very happy to be back to) although that is easy to do. I bring it up because those fine dining and drinking establishments we’ve come to love have a problem right now. Our favorite hotel has no head chef and is looking for a head cook as well. The wait staff is getting a bit surly due to long shifts. We ate at a fairly new Italian restaurant last night (owned by another Miami refugee who had a celebrity swarmed place in South Beach for years) and the bar was closed because they can’t find a bartender. I jokingly offered to take a turn and I’m pretty sure the owner was ready to accept my offer. The man is obviously desperate because he can’t fully open until he finds someone who can make an old-fashioned (us southerners do like our sweet cocktails). We aren’t talking here about low-paying jobs either. That head chef position is offering nearly six figures and the head cook job about $50k. The Italian place was offering $20/hour plus tips for a bartender. And our town, unlike some other places in the country, is fully open. The 7-day average of new COVID cases in our county is 2.

So, why can’t these businesses find workers? The obvious answer is generous unemployment benefits but that seems too easy and trite. Our Jeff Snider says people have stopped looking for work because they know it is a waste of time. But that obviously isn’t what’s going on in my town. And these few jobs I mentioned are not the only ones available here. Major employers in our county include a large, well-known nuclear engineering facility, several major multi-national manufacturers, and a University. But here’s one thing I left out about my town. The unemployment rate is 3.6% and that is double the low set in September 2019. And when you scroll through the unemployment rates by metropolitan area on the BLS website you find that we aren’t even that unusual. The best in the country is Logan, UT with an unemployment rate of just 2% and #2 is Huntsville, AL at 2.2%. Lincoln, NE, Provo, UT, Ames, IA, Birmingham, AL, Idaho Falls, ID, Manchester, NH, Omaha, NE, Salt Lake City, Topeka, Fargo, Appleton, WI, Rochester, MN. All these places have unemployment rates less than 3.3%. Hey, here’s Manhattan at 2.6%. Oh, wait, sorry that’s Manhattan, KS. New York-Newark-Jersey City is 8.2%. If you look down the list of places with higher than average unemployment you find a bunch of places in TX (shale isn’t working right now), places around NYC, Chicago, a whole bunch of places in CA, Las Vegas, and Los Angeles way down there at 377th in the country at 9.9%.

National statistics in a place as diverse as the US often obscure more than they reveal. I see some market commentators scoffing at the idea of a worker shortage but in some places it is real. Generous unemployment benefits aren’t a problem in a town with 3% unemployment like mine. And certainly not in some of these places with unemployment rates of 2 or 2.5%. As for the places with still high unemployment rates, in some cases the reasons are obvious. Texas, despite a concerted effort to diversify its economy, is still dependent on the energy industry. You might have heard the shale oil industry is having some problems right now and it shows in the unemployment rate in El Paso. As for CA and NY, I’d say their problems are mostly self-inflicted but that’s just my own internal bias showing. There is a lot we don’t know about how the economy is changing and will continue to change because of COVID. My town and a lot of small and mid-sized cities would benefit from some internal migration from the large cities where work is harder to find. Will that happen? It certainly seems like it should but a decision to leave your home and move somewhere you don’t know is a difficult one, to say the least. We’ve all read articles about remote workers relocating to small towns and cities too and that’s a trend that seems likely to continue. Will it, now that companies are bringing workers back to the office? There’s no way to know yet but the implications for real estate, commercial and residential, urban and suburban, and rural, could be huge.

There are certainly remaining supply-side issues in the economy which is what we should expect in a recovery from a supply shock. Our politicians have from the beginning of the COVID pandemic responded with traditional demand-side tools. We propped up incomes for people who didn’t need help as if they could keep spending if they just had the means. But the problem was a lack of things to spend on, not a lack of cash. The result is a larger pile of private savings funded by a larger government debt load. These types of one-off tax cuts (which is essentially what the stimulus payments were) have never worked; the majority of it always gets saved. I’m not sure how many times we have to do something that doesn’t work before the idiots politicians stop doing it but apparently we haven’t reached that limit yet. We copied the Japanese approach to monetary policy with QE even after it failed and continues to fail there. Bernanke’s argument was that they didn’t do it fast enough or big enough. Well, here we are nearly a decade into QE here and…it isn’t working. Now our policymakers are set to copy the Japanese again with a big infrastructure spending plan. The Japanese did this repeatedly in the 1990s starting with a government debt about 66% of GDP. Now it is over 250% and it still hasn’t worked. Our politicians apparently believe that, again, the Japanese just didn’t go big enough. Our infrastructure may need an upgrade but it isn’t an economic revival plan. If the Biden administration really wants to help the economy maybe they could provide some relocation incentives to get workers from where they are to where they’re needed. Or maybe I shouldn’t pretend to know what the economy needs either. As I have said many times, don’t just do something, stand there.

Economic Review

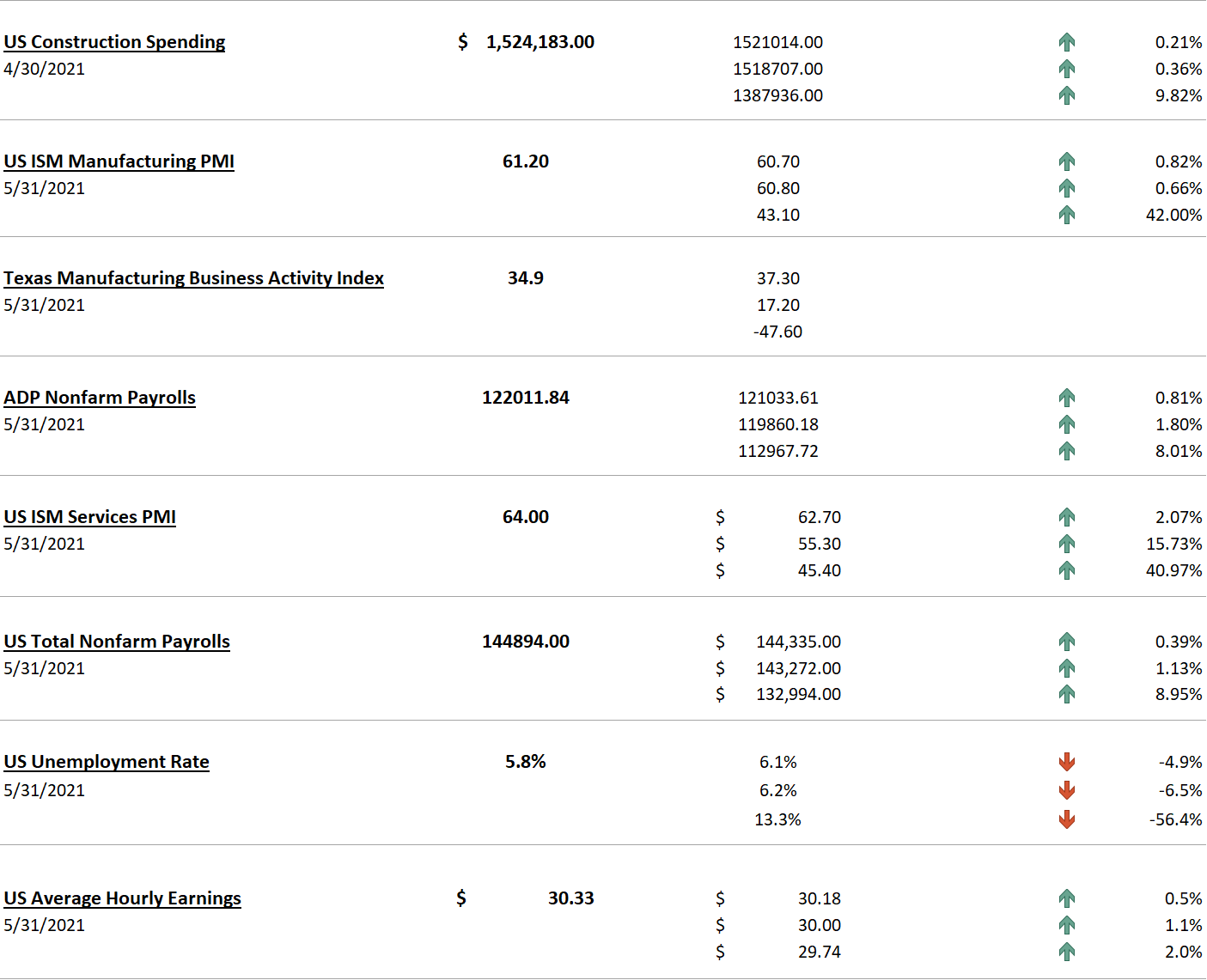

The economic data from last week was mostly survey-type data in which I place little stock. The ISM manufacturing and non-manufacturing surveys were both better than expected with the prices paid components still pretty hot. But it isn’t hard data and shouldn’t be treated that way. Construction spending was a bit disappointing too, although I’m baffled as to why since materials costs are through the roof (pun intended). The market reaction to the data was pretty muted. Bonds did rally after the employment report but the 10-year Treasury yield was down all of 2 basis points last week. Gold took a pretty big hit on the ADP and ISM data but got it mostly back on the BLS report. Crude oil did have a good week but that was more about supply/demand issues that are particular to that market. The copper/gold ratio fell 2.5% supporting the idea that the economy isn’t booming but also not falling apart.

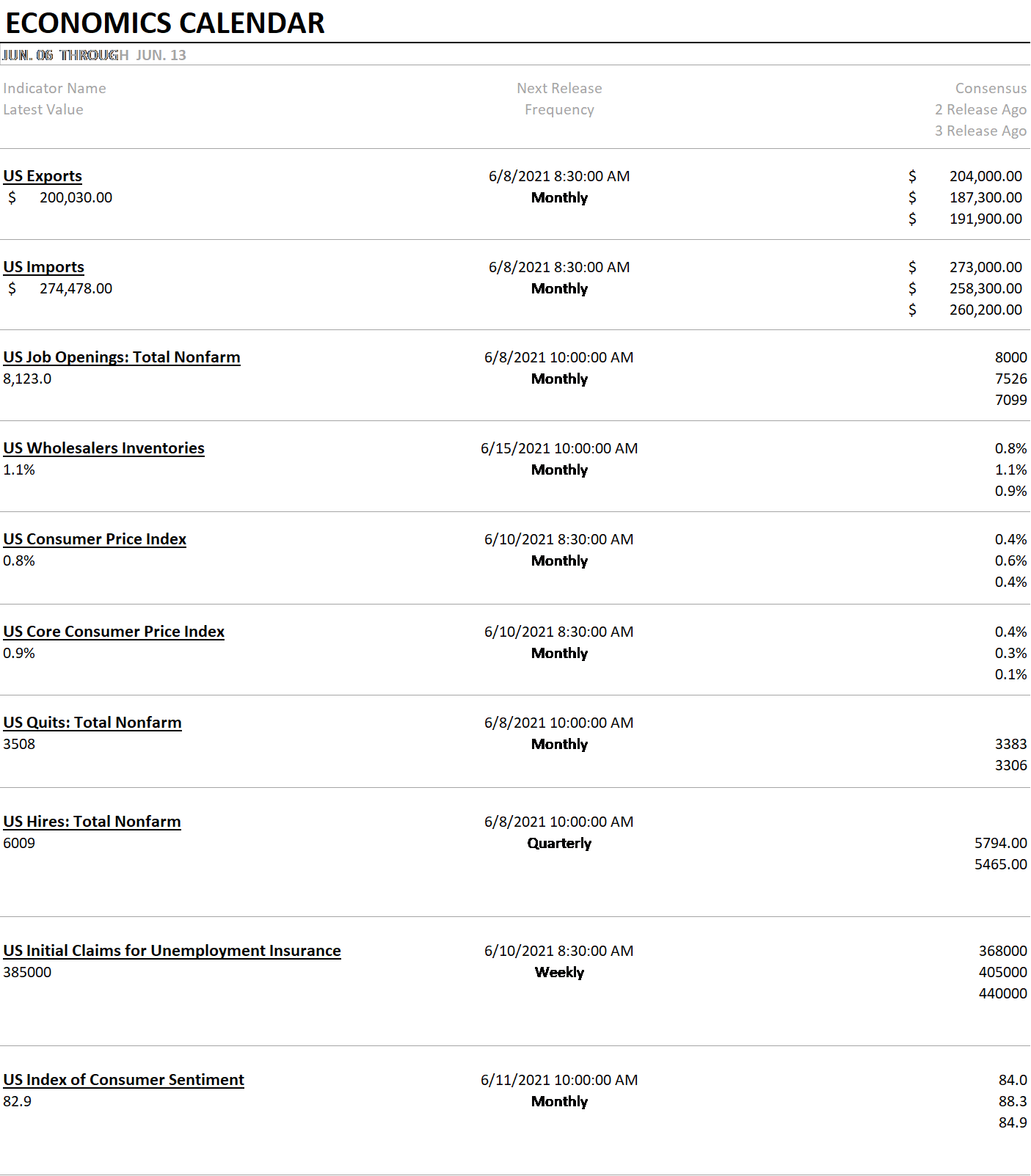

This week’s reports include exports and imports with expectations that exports will start to catch up to the recent surge in imports. I am firmly on the fence about that since the Biden administration seems intent on proving they can be even worse on trade than their predecessors. Trade wars are hard and we ain’t winning. The good news? Um, our trade partners aren’t either? Pretty slim pickings in the department if you ask me. We also get another JOLTS report so we can see how many jobs are allegedly out there that Americans can’t or won’t do. We’ll also get a peek at the latest inflation data which will show that prices went up as they have my entire life.

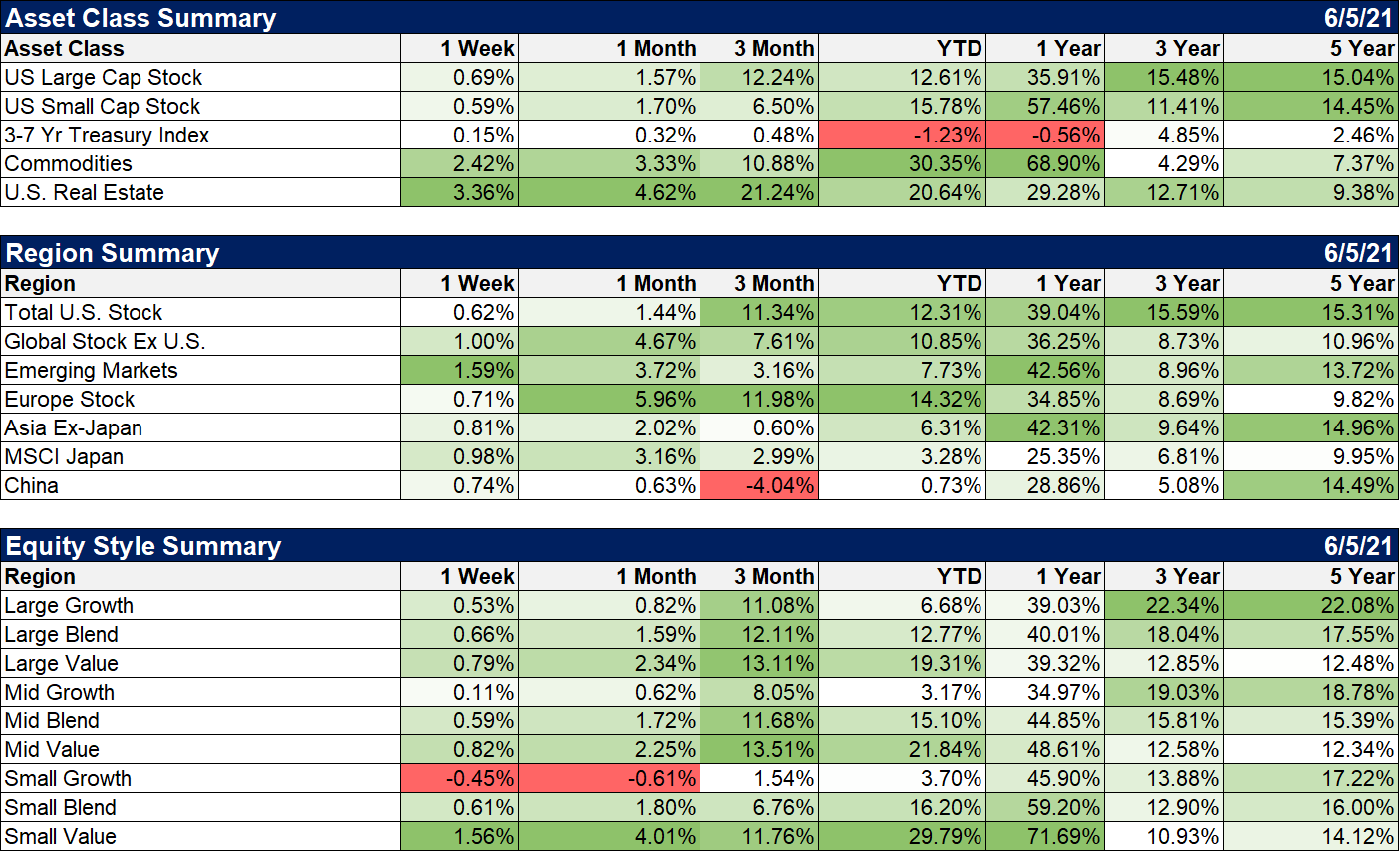

Real assets continue to lead the way in markets with real estate and commodities out front over the last month, 3-months, and YTD. And commodities have nearly doubled the return of the S&P 500 over the last year. Non-US stocks also had a good week with EM stocks up over 1.5%. Interesting and not shown here is that it is Latin American stocks moving the needle in the EM space. Brazilian stocks were up 7% last week and the Latin American ETF over 5%. Value stocks returned to the lead last week too. LC Value is now tromping Growth by nearly 3 to 1 YTD.

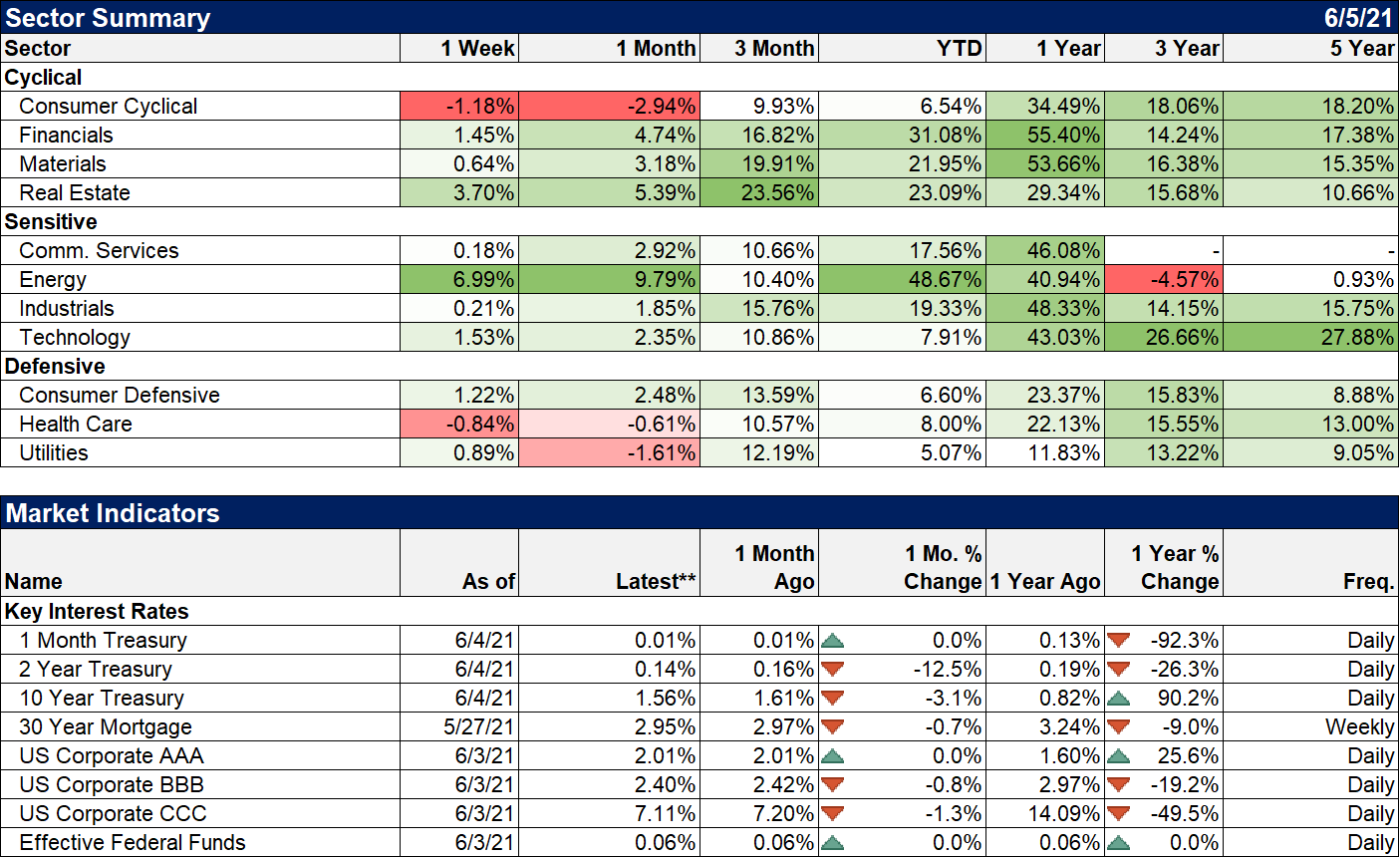

On a sector basis, the big winner was energy up nearly 7% last week. The outperformance of EM, Latin America, real estate, and commodities makes me wonder if we aren’t about to finally see the dollar get in a concerted downtrend. It didn’t happen last week as the dollar was basically unchanged. However, it is near the bottom of its five-year range, and futures markets are very benignly positioned right now. As I said a few weeks ago the only currency I see attracting a lot of bullish intent is the Canadian dollar. Otherwise, the big speculators appear to be as noncommittal as the standard guy character in a typical rom-com.

The US economy continues to recover from the COVID shock even if it isn’t as uniform as some would like. In parts of the country, the recovery is pretty well complete while in others it has barely started. So, yes, it is uneven. But it is continuing and I don’t see any reason to think it is done. Is it a boom? No, at least not everywhere. But in my town and a lot of other small and mid-sized cities, it’s going pretty well. Now if we could just find a decent bartender.

Joe Calhoun

Stay In Touch