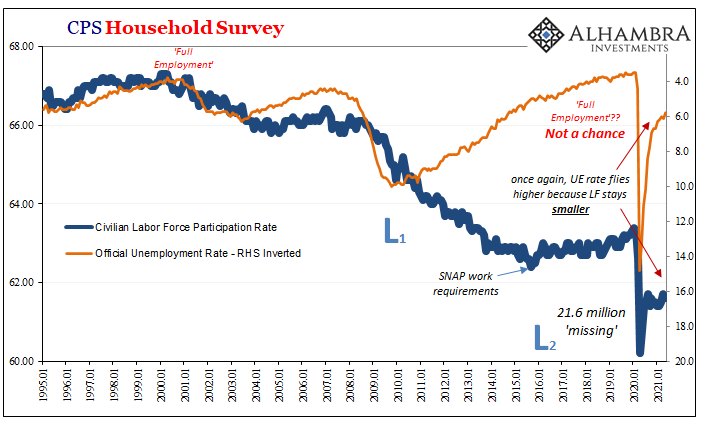

April 2021’s payroll estimate (CES) was the “bad” one; at a revised +278,000 it was “supposed” to have been significantly better than the “good” one for March (+785,000, revised). Near three hundred thousand in any month before 2020 would’ve been celebrated as a near miracle (that’s just how bad the labor market has been for a long time). What made it so worrisome, then, was that already in a deep hole we just can’t afford to take several more years at such a reduced rebound to get out of it (because by then it’ll be clear we aren’t going to, not in any meaningful way, just like the last time).

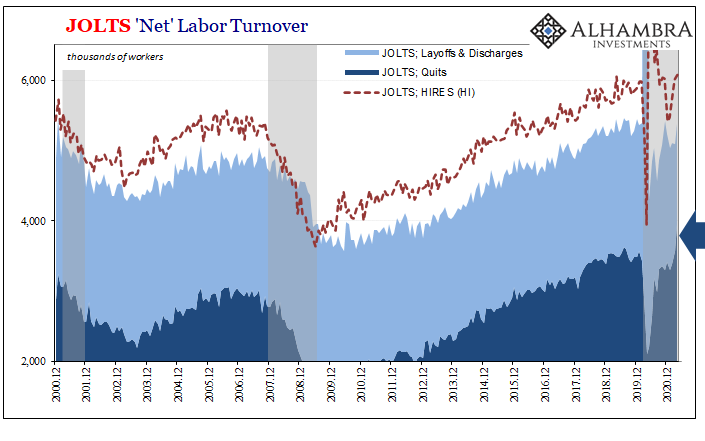

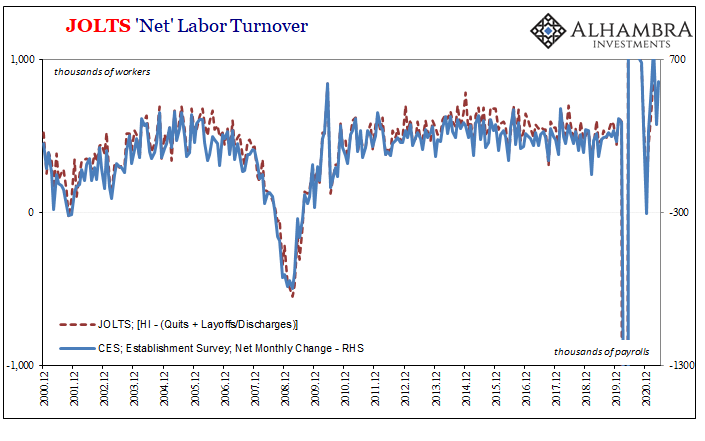

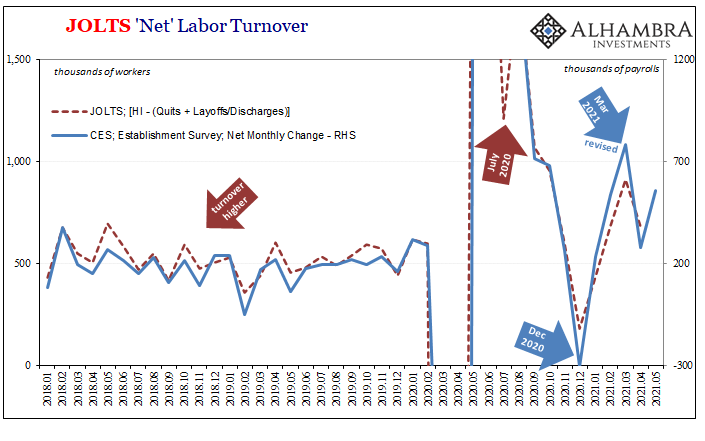

We can and have reconciled, so to speak, the headline CES payroll figures with the BLS’s other major labor market data in JOLTS (along with jobless claims). The latter, estimates on monthly turnover, have in the past plotted to very nearly the same numbers (once you account for a constant discrepancy).

Even though JOLTS is one month further in arrears, when we match them up together it does give us some idea as to “why” payroll levels changed in the way the BLS thinks they have. For April 2021’s huge miss, what the latest JOLTS estimates for the same month, released today, show is that, first, the payroll decline from March was only somewhat larger than what the net turnover indicated, and, second, that using turnover it appears the primary reason for the slowdown was an enormous, out-of-the-blue increase in the number of employed Americans who just up and quit their job.

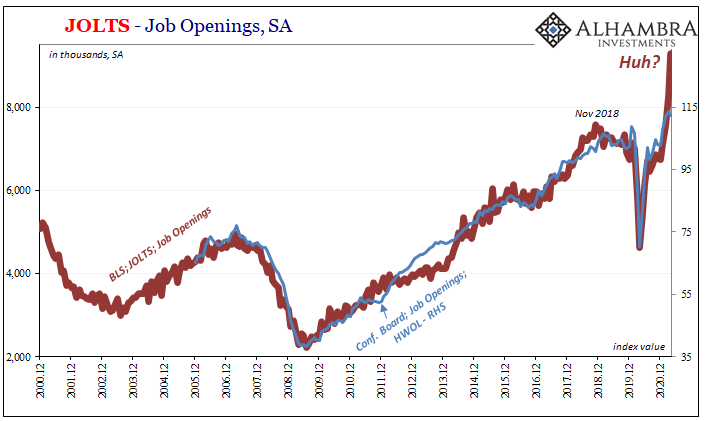

Never seen anything like this before; and this wasn’t even the most jaw dropping series for April 2021 JOLTS. If anyone is interested in highly unusual data, get a load of Job Openings (JO):

We have to start by pointing out the huge difference between the BLS views on JO and other data sources such as the Conference Board’s (whose actually declined a tiny bit in April from March).

It’s almost comical at this point, how the BLS JO figures once again directly feed the same LABOR SHORTAGE!!! narrative. Companies, so it’s being said, are absolutely desperate to find any workers at all income levels. So frantic are these businesses that, according to JOLTS, the seasonally-adjusted level of posted job openings increased by almost exactly a million during April alone; from an already not-even-close record high of 8.29 million in March to then 9.29 million.

This was, remember, the same month as the huge payroll miss.

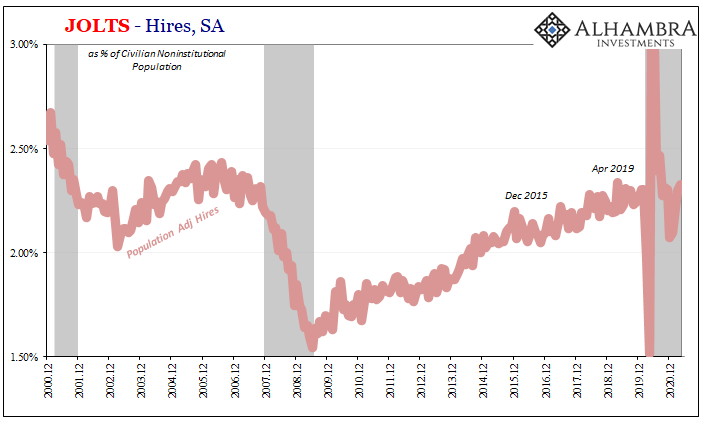

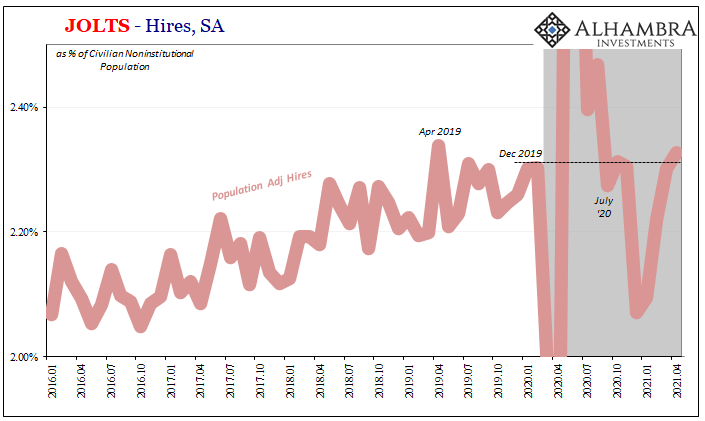

That’s because on the other side of the equation, hiring, or HI, companies continue to add to staffs at a rate that more resembles 2019 and its recession “scare” (which wasn’t a scare). According to JOLTS for April, HI barely increased from March, each only a touch more than 6 million. When adjusting for population, that’s somehow less than what happened during the lackluster mid-2000’s.

That’s the LABOR SHORTAGE!!!!, right? Companies are advertising like crazy but aren’t hiring like they are advertising because workers aren’t coming in for interviews; or, the too few who are, these aren’t employable.

Or, on the other hand there is, as always, a single caveat left out of this formulation, as it was when these same circumstances popped up just a few years ago. And this, I believe, is where the quitting is telling.

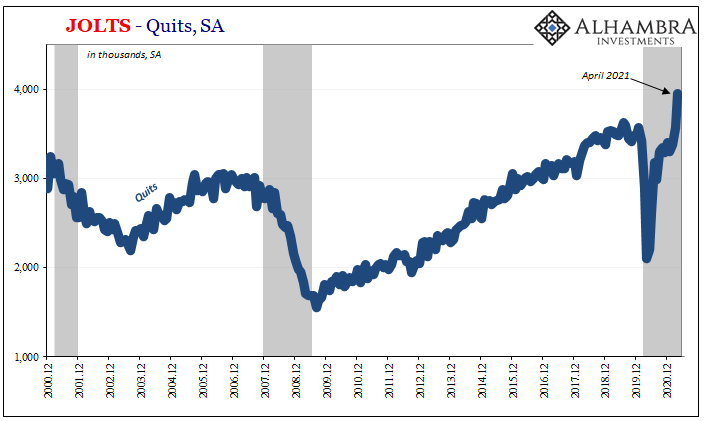

In JOLTS, the number of quits absolutely surged in April, too, if not quite as impressively as JO. Rising to 3.95 million from 3.57 million in March, and 3.38 million in February, this is unprecedented and therefore indicates either bad data/sampling or something truly unusual.

That higher number of quits well more than offset a lower number for layoffs/discharges, combined with basically the same level of hires as in March left net turnover for April down substantially like headline payrolls. This still doesn’t get us all the way down to the low level of the huge CES monthly miss for that same month, but it captures most of it (immediately above).

In other words, what JOLTS is proposing is that for unknown reasons an extraordinary slice of the employed workforce decided they no longer wanted to work at the same jobs – even though, by the same data, they were not hired on anywhere else!

Take this job and shove it!

While it ties into the payroll miss, it doesn’t do much for the LABOR SHORTAGE!!! except to potentially suggest the same problem as in 2018. The key component which, now, historically, and forever after (assuming no MMT), balances labor and business is, obviously, wages.

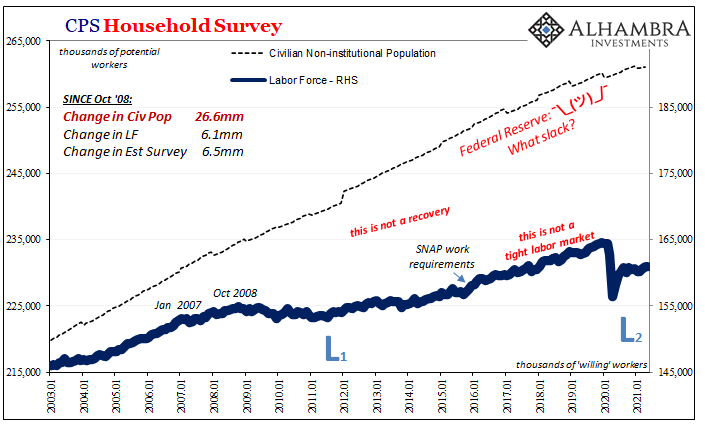

The part always left out of the LABOR SHORTAGE!!! thesis is just that; there is never really any labor shortage, instead companies who are “desperate” to hire workers just must not be paying the market-clearing wage. Their anguish is quite really a function of their own bottom lines. All the data shows conclusively this enormous slack.

It can’t be – at least in this case – a higher comparison favoring unemployment payments because you don’t get to claim benefits unless you are involuntarily separated; these, according to JOLTS, are workers who left of their own volition. Why?

It could be a number of possible reasons but the most likely, certainly in my view (FWIW), is likely to have started with low starting pay supplemented by promises of better pay down the road. Companies, especially small and medium-sized businesses, the same who claim to be most hard-pressed to find workers, are and have been deeply hurt by the recession. Thus, the pay mis-match.

We’ll start you out low because that’s all we can afford, but don’t worry we’ll bump you up just as soon as this red hot economy (Warren Buffett said so!) gets only hotter.

But if all that heat turns out to have been hot air? The longer real recovery doesn’t happen, the more it becomes apparent to newly rehired or hired labor it isn’t going to. See ya!

Though manifested differently, still too similar to 2018’s LABOR SHORTAGE!!!! which was easily explained in the same sort of way; if companies were actually experiencing a truly booming economy, they would’ve paid the requisite clearing rate to have hired all they could handle and more. Macro slack then as now.

But they didn’t because they wouldn’t or couldn’t pay what the market wanted, and so neither a true labor shortage nor the inflation a real one would’ve proposed. This doesn’t mean there aren’t pockets or instances of shortages in isolated cases, there are, but it doesn’t add up to anything like a huge boost to inflationary pressures many envision now just as they had in 2017-18. Today, as then, quite the opposite, actually.

More on this – from eurodollar futures – later.

Stay In Touch