It wasn’t all that long ago when the media began to fill itself up with one story after another about how huge looming inflationary pressures were causing the entire “market” to rethink its lengthy and determined anti-reflationary stance. Back in March, for instance, S&P had joined this chorus by zeroing in on eurodollar futures, of all instruments, and coming back with premature rate hikes out of them.

Recent trading in the Eurodollar and Fed Funds futures markets, which both track short-term interest rate expectations, along with a run-up in the five-year Treasury note yield, show that investors believe rising inflation during the post-pandemic economic recovery will trigger the Fed to prematurely abandon its policy of keeping rates at or near 0%.

No, no, no. This was – and remains – either blatantly false or intentionally obfuscating. Relative changes in curves like eurodollar futures demand accounting for all its dimensions; not just in which direction it might be moving at any time as well as through time, but intensity, too, along with nominal placing.

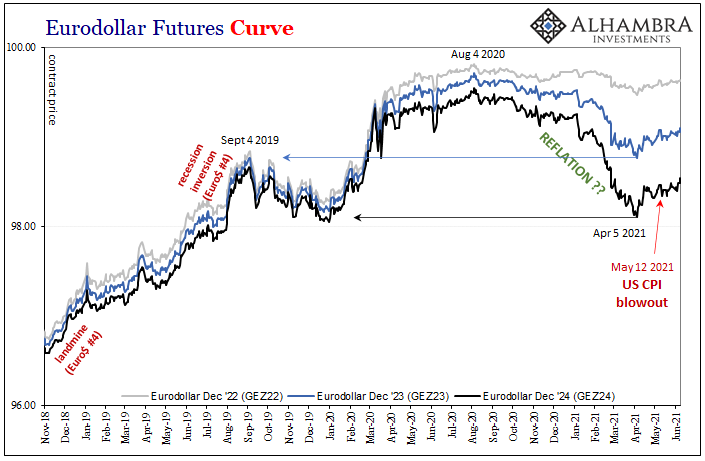

What the eurodollar futures curve at its lowest point (August 4 last year) had indicated was only trouble in the near-term building up to what was almost certainly a bleak intermediate and even longer-term (if there is much predictive power out past the greens and blues in the golds and purples). Thus, that nearly axis-constrained near-perfectly flat curve steepened somewhat during reflation, especially after early January 2021, to price a couple fewer permanently awful scenarios out of thousands of possible permutations.

To put it into S&P’s terms, what the market actually suggested was that rate hikes by the end of 2022 were no longer impossible; that didn’t make them in any way probable. Quite the contrary, as you can see when taking account of more than just contract price direction. Factoring curve nominals relative to history, recent and long term, that’s all it ever was.

Like the last time we did this inflation hysteria, “they” are all purposefully searching for the tiniest of molehills to make into mountains. And with eurodollar futures, tiny really does apply here.

Then came the April CPI which was released to the public on May 12. It was humongous in whichever way you wanted to compare and seemingly confirmed everyone’s worst inflationary fears (or the media’s long-sought I-told-you-so moment); big numbers all around with the core CPI’s monthly change the biggest since the tail end of the Great Inflation.

Given this, as well as other estimates confirming like those from the PCE Deflator, whatever those rate hike probabilities these must’ve gone so much higher, right?

According to Reuters, yes, they did. Quite unbelievably (as you’ll see in a second) the news outlet wrote up a story on the same day as April’s CPI, May 12, actually claiming this same market was indeed ramping up its expectations for what S&P had characterized a couple months before as “the Fed to prematurely abandon its policy of keeping rates at or near 0%.”

The eurodollar futures market, which tracks short-term U.S. interest rate expectations over the next few years, is betting on a roughly 80% chance of a rate increase from the Federal Reserve by December 2022, after the release of stronger-than-expected inflation data.

Huh? Where do these people get their numbers/math from?

But let’s set that aside and focus on the market “reaction” to the CPI as well as all the other economic data seemingly having pointed in the direction of Warren Buffett’s red hot economy and his even hotter inflationary warning about it.

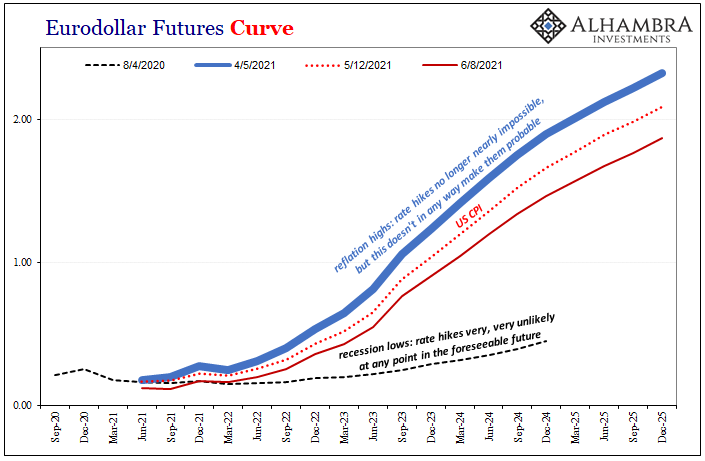

If eurodollar futures prices go down as future expectations of interest rates (3-month LIBOR, in this case) go up, then according to Reuters the eurodollar futures market surely must’ve been hit with a serious, game-changing selloff in the wake of those inflation figures on May 12.

Except, no, it’s been the exact other way since early April:

Going back to that point, eurodollar futures have instead joined the Treasury market in anti-reflationary behavior. Properly placed into the context of nominal indications as well as history, more appropriately interpreting these markets leaves you wondering if all these people are looking at the same markets.

Despite the CPI – as well as, described earlier today, the growing assurance of yet another labor shortage (even though the last one turned out to be fake) which will, supposedly, contribute a huge amount to inflation – more and more these markets are turning their back on any sort of inflationary probabilities at any levels. Doesn’t matter the economic or consumer price data today, the uniform picture across the entire “bond market” going back to, oh, Feb 24-25-26 is to look right past all of it.

And, just to be clear, the curves were unequivocal even during their reflationary selloff (January thru March) that any probabilities of inflation running tepid let alone hot never got all that high to begin with. As I wrote at the end of March, just as that reflationary run was running out:

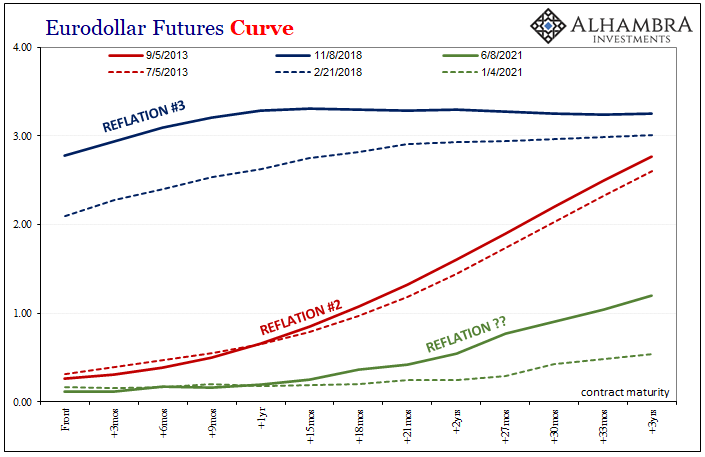

This December 2024 position is basically saying the first half of the decade of the 2020’s will somehow, on average, be materially worse than the 2010’s even if slightly better than the single and singly awful year 2020 had been where inflation and economic growth is concerned.

But that’s not the message you see all over the internet despite it being right here in the right market.

A little bit better than last year just doesn’t have the same ring to it, especially in light of the desperation to paint early 2021 as somehow different from all prior post-2008 circumstances. That’s all the curves have said even up to and including April 5’s price trough/near-term reflation peak.

And today, despite the out-of-this-world inflation numbers along with JOLTS Job Openings as apparent confirmation of massive labor shortage pressures, the eurodollar futures curve like the Treasury yield curve is “somehow” pricing even lower probabilities of higher rates all over again – as if the CPI didn’t really mean much or anything beyond early 2021.

Not just “transitory” inflation, which isn’t inflation, it’s all transitory price behavior for the same reasons these curves never truly got off the ground. Overall conditions really haven’t changed all that much from one of the worst years on record. No wonder there’s so much disinformation because there is next to nothing in evidence conceding all this talk of sustained inflation is even much possible.

Stay In Touch