While capital “E” economics can never seem to get out of its own, infatuated with statistics and regressions instead, small “e” economics is proven time and again. Simple supply and demand curves aren’t a realistic simulation of potential conditions, yet they are far more helpful than DSGE models even if highly stylized representations.

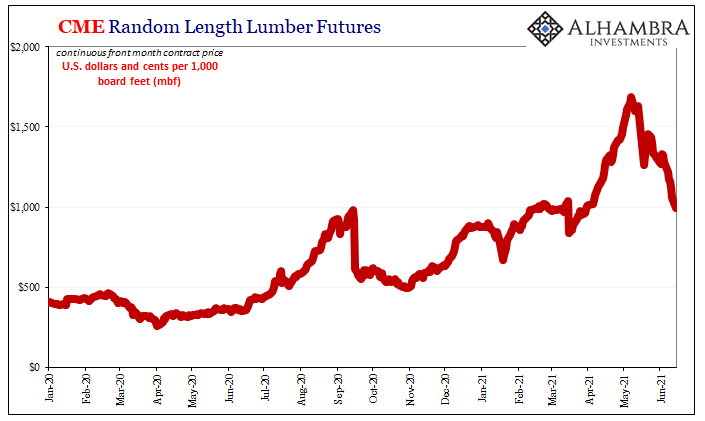

Take, for example, lumber prices. Anyone remotely familiar with housing over the last year has been cursing the average cost of wood. If you’ve been hoping to renovate on Uncle Sam’s nickel, up until early this year the commodity cost you the government’s dimes and quarters, too.

Peaking early in May at very nearly an insane $1700, today the spot price closed below $1000 for the first time in months (the futures curve still in heavy backwardation). Why?

Milling, mostly:

Lumber futures posted their biggest-ever weekly loss, extending a tumble from all-time highs reached last month as sawmills ramp up output and buyers hold off on purchases.

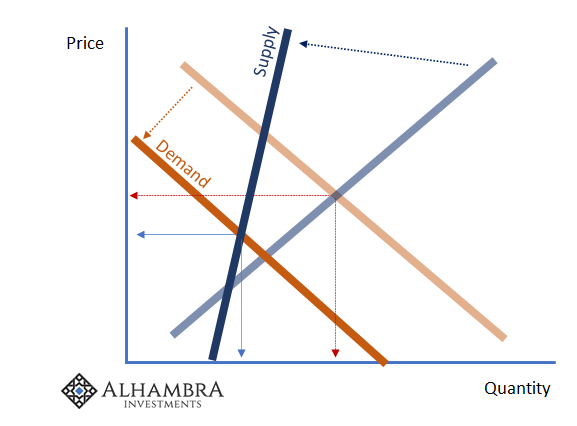

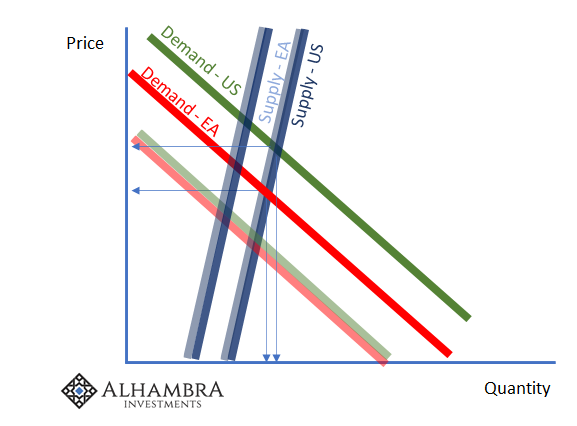

Like a lot of parts of the global economy, housing/wood/material each saw a drop in both supply and demand given last year’s recession. But the supply curve for many of the commodity segments didn’t just shift to the left, they grew inelastic, too. Drawing this using small “e” economics, the implications are easy to see (keeping in mind they aren’t depicted as anywhere close to a realistic scale):

Deflationary contraction. Both price and quantity decline substantially, entirely consistent with 2020’s big drop.

Following the trough, however, demand has outpaced supply rebounding from that bottom. Together with specific (transitory) factors holding supply back, preserving the curve’s more vertical shape, as each come back up the “equilibrium” doesn’t land in nearly the same place as it had been before the drop.

But if demand levels off while the supply curve shifts just incrementally back to the right, prices will begin to fall back down again – exactly what’s starting to jump into the lumber market – even if ultimately the quantity at “equilibrium” is less than it had been at the start (red arrows above) before the contraction.

Not only does this pattern suggest transitory “inflation” (using the quotes because a supply shock isn’t inflation), it also indicates that once those supply factors settle the underlying state of demand, which hasn’t actually recovered, begins to more and more reveal itself.

While prices were skyrocketing upward there may have seemed an inflationary excessiveness to it, making it appear that the economy had “overheated.” In reality, small “e” economics, it is more likely settling in the opposite shape. Once beyond the commodity-induced price effects, it becomes clear the economy is settling back into the same disinflationary circumstances or even more than when this all began.

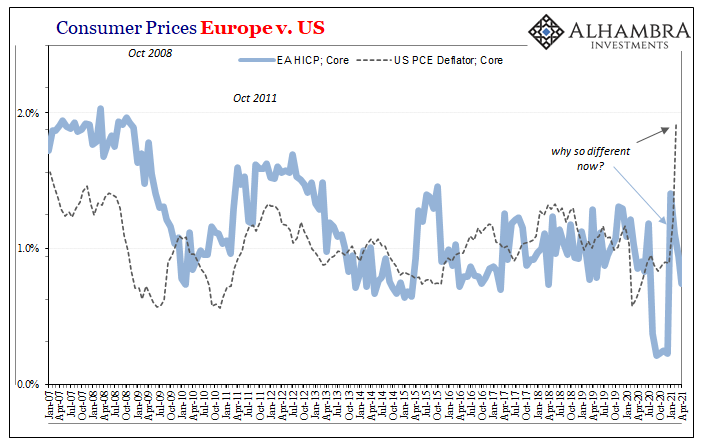

Is there any evidence for these simple curves outside of the steep dive in lumber? Well, yeah; it’s everywhere. Including the US CPI (last two, in particular).

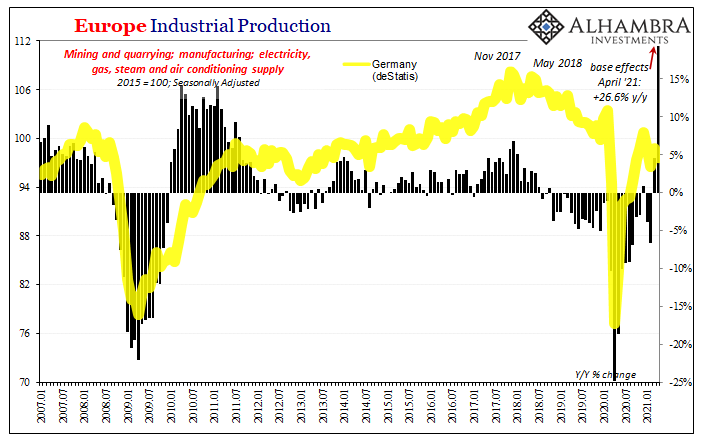

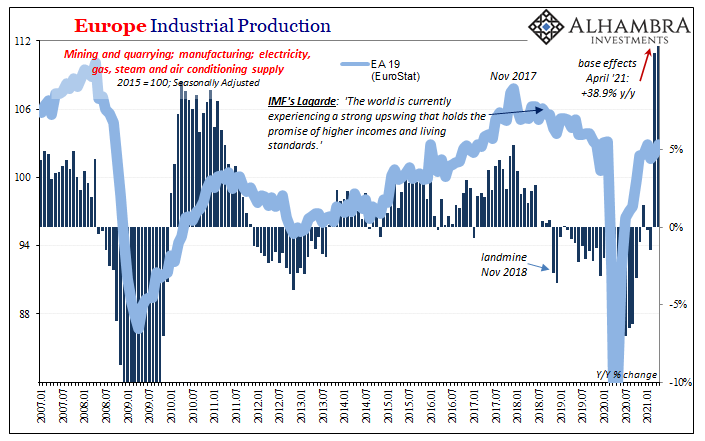

Start on the supply side in the global goods economy. In this case, we’ll use the broad measure of Industrial Production across a range of different geographies. In Europe, German IP continues to languish despite loosening restrictions which had previously inhibited the lackluster rebound going into this year.

Still, now into April (the latest data), Germany’s industrial sector remains depressed when compared to pre-COVID as well as, more importantly here, in terms of what should be happening given general commodity and goods prices.

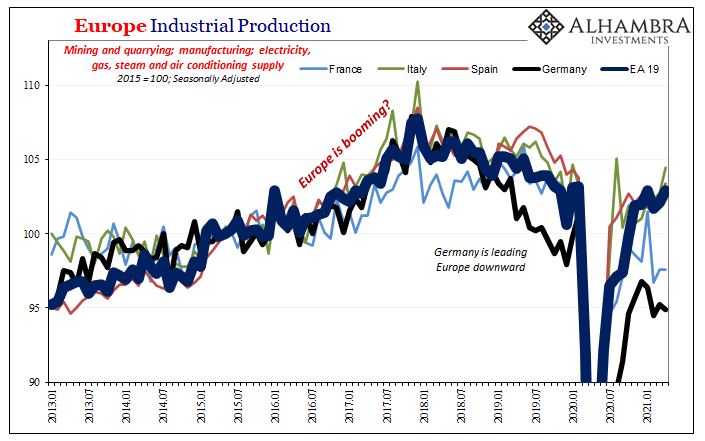

The rest of Europe is performing only slightly better. France more like Germany while Italy has come out the best of the Continent’s largest constituents; though none of those is categorically different from their German counterpart. Slightly better than awful remains in the same category of curiously depressed.

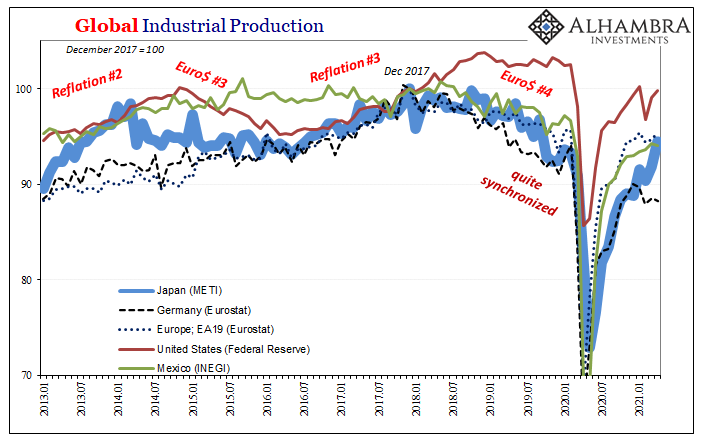

Mexican industry has fared much like that of Europe, while US IP indicates a more buoyant rebound but one that has lost quite a lot of that over the past few months. Only the Japanese seem to be moving more quickly in the upward direction lately, but even here industry is still unusually depressed given prices and the scale of the decline it is rebounding from.

The entire global industrial sector (including China), which contains, among other things, commodity production, is failing to robustly come back from a very deep bottom.

On the other side, demand, there’s been wider variations in the reflationary return in each of these places. Demand in the US goods sector, in particular, has obviously been more fulfilling due to the also transitory influence of Uncle Sam, inducing the US curve a bit higher and right than the same for other parts of the world – particularly Europe.

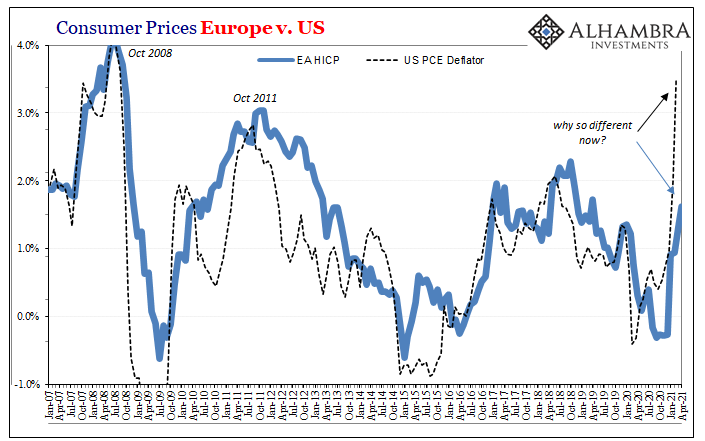

In other words, basically the same supply situation (depressed) but vastly different on the other side given shifts in each demand curve. This shows up, then, in a sudden discrepancy between consumer prices:

The CPI in America is hitting into 70s-style while in Europe it’s not any different from the past few years. This despite the fact that, global factors, inflation conditions in Europe and America had tracked one another (suspiciously) closely before the past couple of months.

Different demand curves for the same sort of inelastic supply curves.

This, then, raises the key issues facing each moving forward. Where will the demand curves be as the global economy moves into the second half of 2021? There could be more room to rebound (shift right), though already suspicions about how far or fast. In the US, mostly, we have to wonder if we’ve seen the fullest extent of that shift as the federal government’s artificial influence wanes (even with accelerated child payments coming next month).

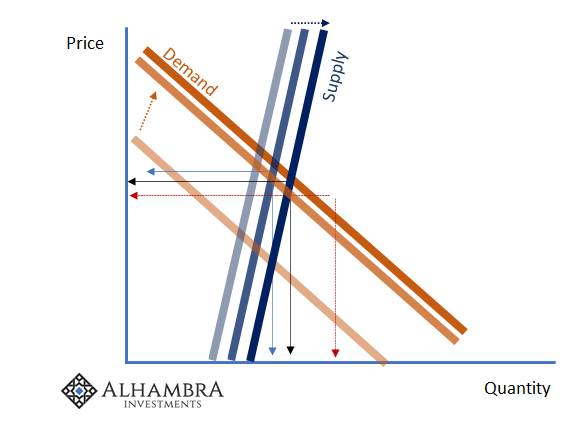

Bottlenecks like the global chip shortage have surely plagued the supply side everywhere, but is that the only problem restraining those? For one, given commodity prices, if some super-cycle was upon the world only being held back by this then producers overall would be acting (and producing) with reckless abandon already. If they really believed these prices were sustainable, we’d see it in global IP (and more).

On the contrary, producers are producing as if they believe demand may not have much more to go on the upside (much smaller potential shifts to the right). Thus, as supply begins to catch up those bottleneck prices drop (crash) away leaving the entire economy exposed, in the second set of curves drawn above, as substantially less than its pre-recession condition.

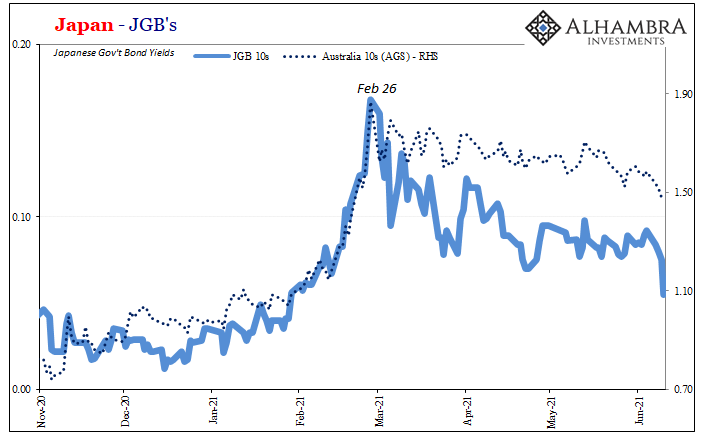

How would the prices of, say, safe and liquid instruments react to the potential increase in the probability of this kind of situation? They would rise, rates would fall, no matter what the current estimates for consumer prices; both the outsized, Great Inflation-like figures in the US as well as the is-this-all-you-got over in Europe. In fact, because of this disparity, it only adds to those probabilities.

No recovery, not even transitory “inflation”; just uneven rebounds in terms of geography as well as demand vs. supply. And with bonds behaving as they have, ignoring each of the last two vastly different CPI’s (and PCE Deflator numbers), that’s growing uncertainty about how much farther in demand along with more certainty about the limitations imposed by the true shape of supply after bottlenecks.

Stay In Touch