If it walks like a duck and quacks like a duck, then it must be inflationary overheating. Or not? As more time passes and the situation further evolves, the more these recent price deviations conform to the supply shock scenario rather than a truly robust economy showing no signs of slowing down.

There are any number of those currently being exhibited, along with a few that call into question just how much speeding up had been done in the first place.

This shouldn’t have been, or wouldn’t have been, an issue in any actual overheating – especially what’s really been behind the upside. Unprecedented direct government intervention, payments to businesses and consumers alike extending into trillions. The theoretical basis for the inflation scenario was always that easy.

But no matter how many trillions you pour into it, if the economy has been seriously damaged the most that will come out is a transitory price history. Given Uncle Sam’s (not Jay Powell’s) influence, demand rebounded more quickly than supply causing the obvious imbalance; this was then extrapolated by assumption into overheating and inflation.

That assumption would only have been valid if the economy actually performed as if it was, rather than, as it has, truly underwhelmed. Outside the domestic goods economy, there’s nothing much to indicate sustainable influences (it only gets worse outside the US, too). And as the federal government’s influence(s) fades (even with more advance payments set to begin next month), there’s been instead a palpable turn toward, hey, wait a minute, that’s it?

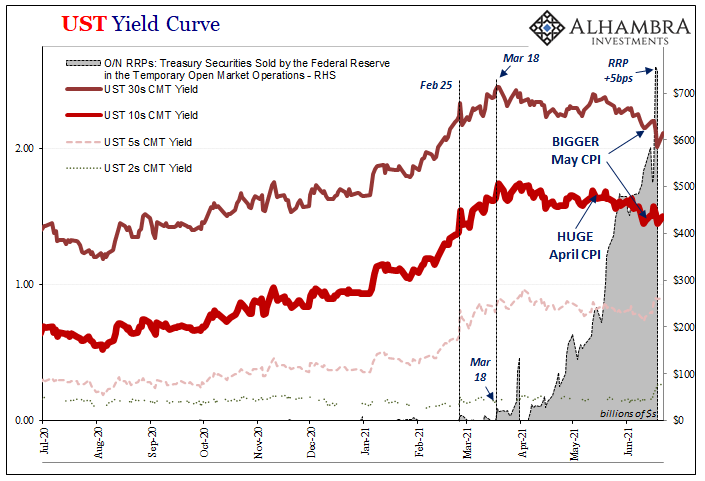

Not just bonds and stubbornly anti-reflation interest rates being affected by the same problem affecting bills and the Fed’s reverse repo. Narrow overheating in goods and commodities is one thing, why hasn’t it been more broad-based?

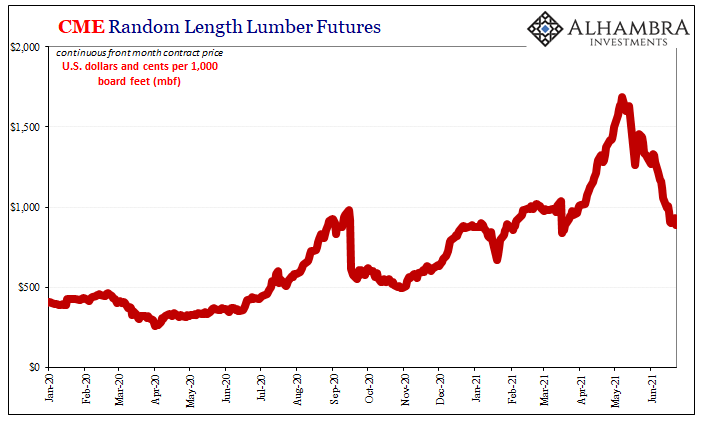

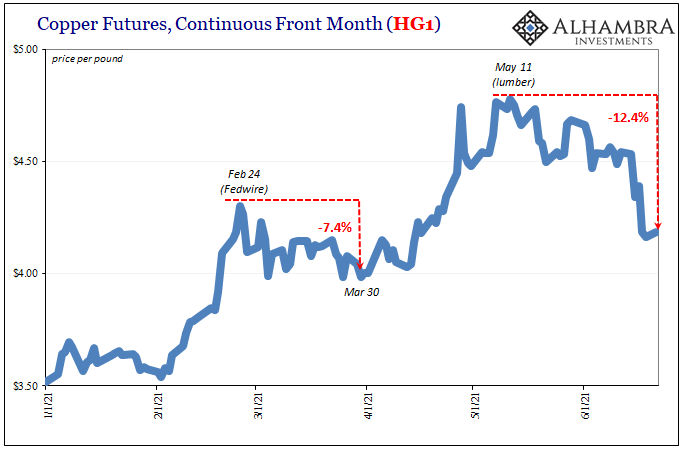

And now commodities have begun to soften and right on schedule (sort of); meaning that as supplies begin to tick up (along with de-hoarding and destocking inventories) the supercycle meme loses much of its potency – particularly given that its two key leaders, lumber and copper, are now its two key losers. Lumber prices keep falling, now below $900, while Dr. Copper has (for now) stabilized around $4.20.

Neither trend points toward overheating or supercycles (nor does the constraint shown by producers). On the contrary, if it walks like a supply shock and quacks like a supply shock it must be…

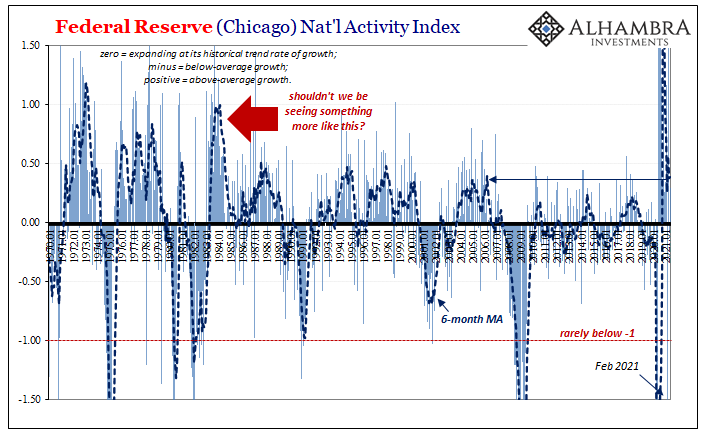

In more macro terms, the Fed’s Chicago branch and its National Activity Index does a fair job of highlighting what’s also been missing. The index had tumbled sharply in February (revised now to a pretty terrible -1.61) based, we were told, on unusually cold weather. It rebounded sharply by more than 2 points in March but then fell to slightly negative in April. The latest update for May puts it at only +0.24.

This thing – like a lot of data – has been all over the place because of the difficulties of the past year. On average, however, we’d expect by now unambiguousness behind the numbers. With everything supposedly going for it, why isn’t it going so much consistently faster? You’d think by May 2021, with trillions in “stimulus” and more than a year of “recovery”, this index would manage something substantially greater than +0.39 (6-month average).

While that level is higher than the peaks registered during the post-2008 lethargy, it’s still only equal with 2005 (not exactly a rip-roaring economy) and noticeably less than during the best times of the 1990’s. It is nowhere near like what the index had indicated during the 1980’s, particularly the big recovery after the 1981-82 recession – which is just what an overheating economy would at least begin to resemble.

Why aren’t we getting 80s-style figures outside of a few narrow goods segments? It really should be widespread and constant.

This doesn’t just propose a supply and demand imbalance to explain consumer and producer prices, it also is entirely too consistent with incredibly low bond yields looking out well past those and pricing an economic baseline that’s somehow even more degraded than the one priced into the 2010’s.

That’s really all reflation has been in the markets to this point; a bunch of temporary and artificial factors that could only hide these deficiencies for so long. And while those don’t look nearly as awful as they had in 2020, being slightly better than awful doesn’t work out to good. Certainly not inflation good.

Stay In Touch