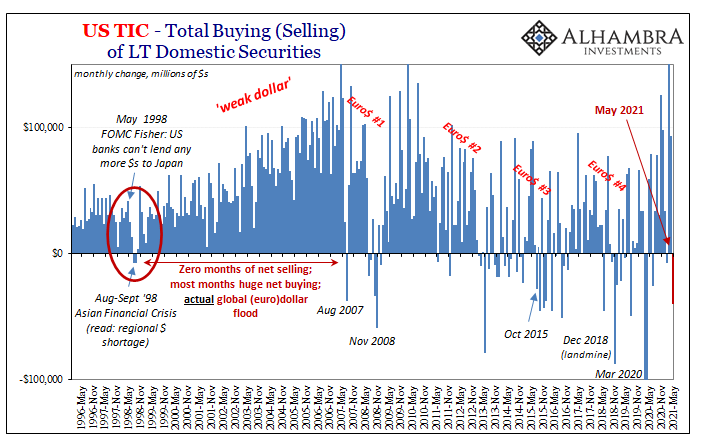

I’m just going to post some brief comments on other parts of the TIC data. The major takeaway from the May 2021 update is what I wrote earlier, how what these figures show is both entirely consistent with what will be to most people a surprisingly long history as well as completely misconstrued in mainstream conversations (what few may take place).

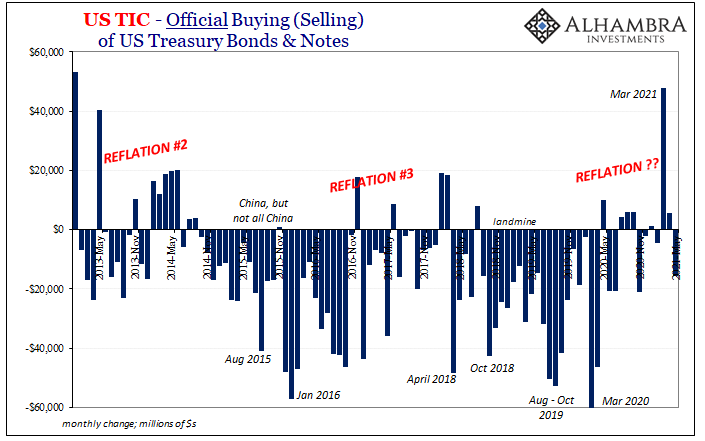

We’ll begin with official institutions. They were again on the selling side of UST’s, after having been solidly reflationary buying (also backward to convention; central banks adding UST’s during reflation when everyone is supposed to be getting out of USTs) back in March. Not huge selling, and a single month doesn’t by itself lead to any solid conclusions.

However, as discussed at length earlier, this is hardly a singular indication or isolated case.

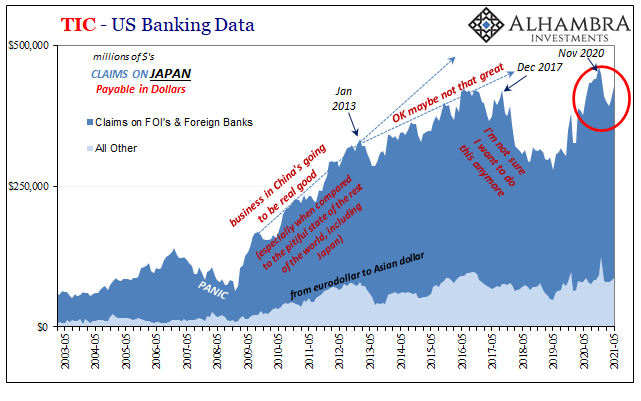

From there, we’ll look at a few interesting regional/geographic dollar distributions. Starting with, ironically, Japan, the TIC balances show now two months of reversing the prior decline in what US banks report to claim from Japanese counterparties (ironic in how I used the history of Japan selling UST’s to illustrate the opposite of what these last two months of this series indicates).

Dollar activity with Japan had dropped considerably – one of the first clues for brewing difficulties – beginning last December. A couple months of rebound isn’t necessarily reflation-ish, it’s not uncommon for variations month-to-month or a for several months.

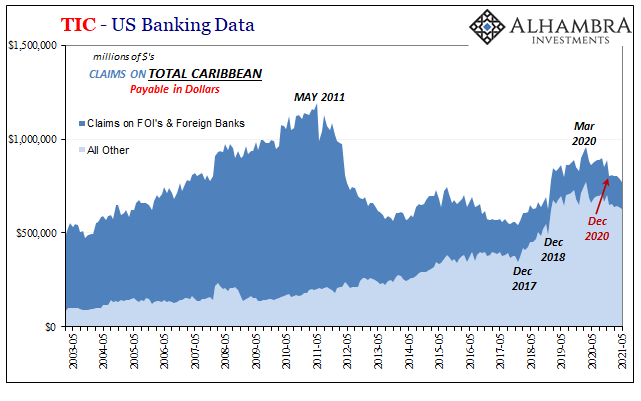

The Caribbean, on the other hand, a major eurodollar system node still shrinking and nearly identical to Japan before April and May this year: December 2020. You don’t want to make too much out of this data, either, simply because it is inconsistent, torn up by discontinuities, and applies to a sector of the global eurodollar market notorious for being utterly opaque and unreported in any fashion.

You can blame Caymanian denizen Emil Kalinowski; and if you don’t wish to do so directly, I’m happy to on your behalf.

That said, still there are some correlations worth paying some attention. This latest development could be one, though, again, it more than any in TIC probably requires the most corroboration and initial skepticism.

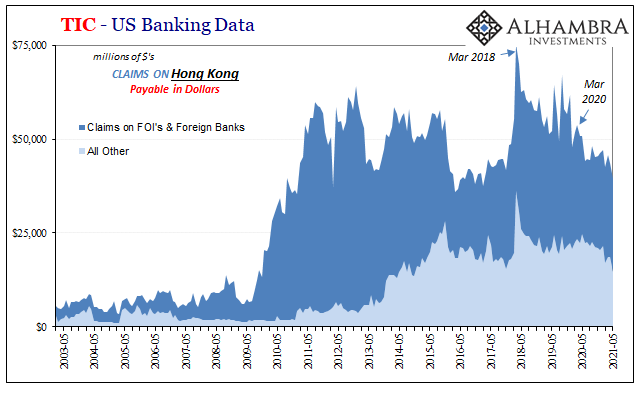

Another one of note and potential noise is Hong Kong. We’ve paid close attention to dollars in this place for its connections (obvious and otherwise) to China and the mainland’s constant dollar issues. Unfortunately, the Hong Kong TIC data can be taken in a number of ways.

The falling balances could be consistent with lack of dollar flood and even the growing evidence for the 2021 dollar shortage.

But there is also a possible political correlation with China’s incredibly sad yet assertive authoritarian takeover. Whomever taking whatever dollar transactions are getting out of town. Even if this latter possibility, this would seem to slam shut any hope of restarting China’s 2017 suspected – never confirmed – Hong Kong bypass.

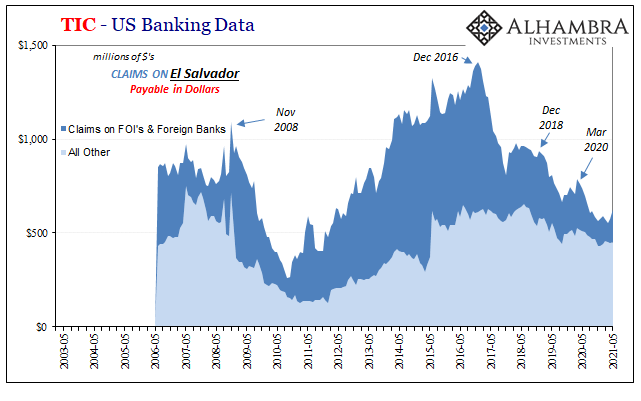

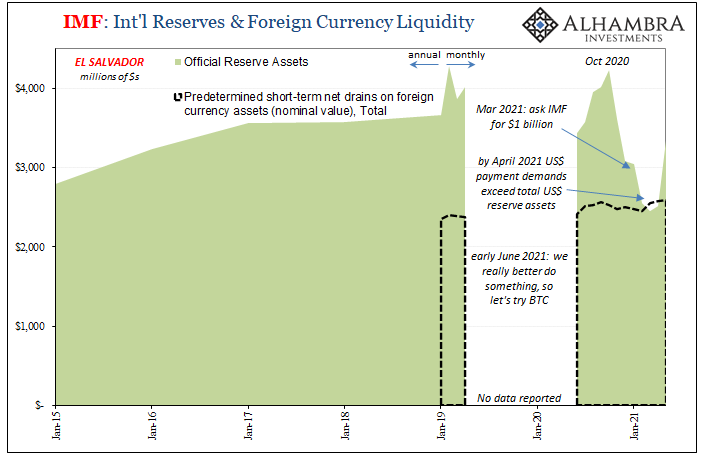

Lastly, I thought it worth including El Salvador’s TIC. This sovereign nation in early June announced that it would study and then move to accept Bitcoin as legal tender later this year. As I recently wrote, though:

Even hardcore Bitcoin maximalists are at somewhat of a loss to explain it. On the one hand, this is exactly what they’ve been preaching ever since the pseudonymous Satoshi Nakamoto laid down the currency’s genesis block way back on January 3, 2009. Bitcoin, they say, is an actual and useful currency so here’s a country willing to put their form of modern money where its confusing mouth is.

But – and here’s the hang up – Bitcoin is supposed to supplant the dollar because the latter has been judged by its most hardcore proponents as worthless; the Fed and its obscene levels of “money printing” and all that. Not, in other words, what El Salvador is up to.

The country isn’t attempting to defend itself from the eurodollar system’s imminent demise. On the contrary, officials from El Salvador had previously, in early March 2021, just three months before this Bitcoin gambit, opened discussions with the IMF for a further $1 billion infusion – our first clue about what’s actually happening here.

Treasury’s TIC data, as you can see above, even more damning than the IMF’s reserve data (below) since this other, TIC, relates to private dollar conditions for those in the country rather than official reserves, therefore TIC refers to the ability (or, in this case, inability) of local banks to source dollars in regular fashion.

Reserves come into play only after problems in the private sector (basically the point of my earlier TIC analysis).

Ghost money, in other words. The consistent history of what follows from inelasticity which here as well as everywhere else it is observed around the world flies directly in the face of “too much money.” No dollar flood here, either, on the contrary the potential usefulness of a form of crypto ledger money – or money of account – in the absence of, too little effective supply (read: forget about the Fed’s bank reserves).

Stay In Touch