Go early and go fast. This was the message FOMC Governor Christopher Waller wanted to send to the CNBC audience watching his interview yesterday on that channel. He was referring to the possible taper of QE6. In Waller’s view, if the US economy lives up to its current hype in the form of two more blowout jobs numbers, those would confirm the Governor’s view inflationary potential is perhaps much higher than indicated by the Fed’s overall “transitory” stance.

He doesn’t mean to say the existing interpretation of recent US (only) consumer price data is wrong, rather it would be superseded by recovery events. In the case of continued near-million payroll months, this would seem to indicate using up remaining macro slack so quickly, demanding a shift in policy since labor market overheating would then, in the textbook view, greatly enhance the risks of this transitory supply shock and their artificial factors becoming more realistic and more serious inflationary pressures.

To get ahead of this scenario – should everything fall into place – would mean moving the start of rate hikes up which first requires a quick end to QE. Taper by September, possibly, according to Governor Waller:

In my view, with tapering we should go early and go fast in order to make sure we’re in position to rate rates in 2022 if we have to. I’m not saying we would, but if we wanted to, we need to have some policy space by the end of the year.

A very, very fine needle to thread. Beginning with the payroll reports, obviously, for this to happen they’d have to be sizable in spite of recent indications which are more heavily tilting in the other direction (jobless claims, for one).

But beyond his immediate data standards, there is a growing list of growing real-world negatives. For a conventional Fed policymaker like Waller, his view ends at the US boundary (textbook Economics determines the US economy as some mostly closed system). The FOMC doesn’t really care all that much if the rest of the world is suffering something to a greater extent with no end in sight – and maybe a possible trend worse than that.

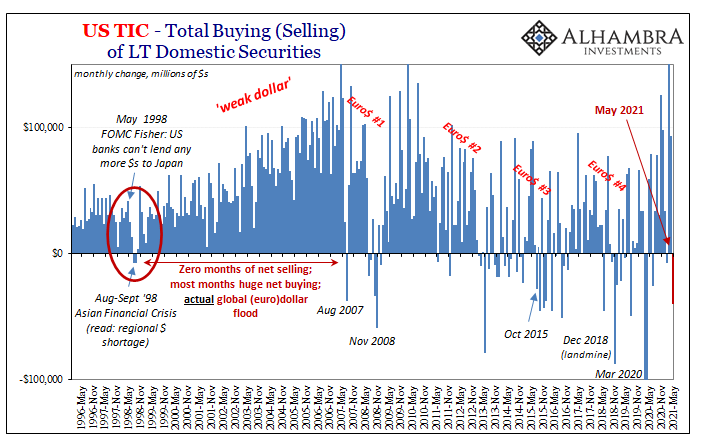

It’s a lesson these people never seem able to learn even though it was put right on display beneath their very noses only a few years ago. Here we are yet again with central bankers domestically talking about rate hikes and domestic inflation pressures because of a presumed quickening pace to purported domestic labor market strength when the entire rest of the global system is increasingly obsessed with the reverse potential of all those things.

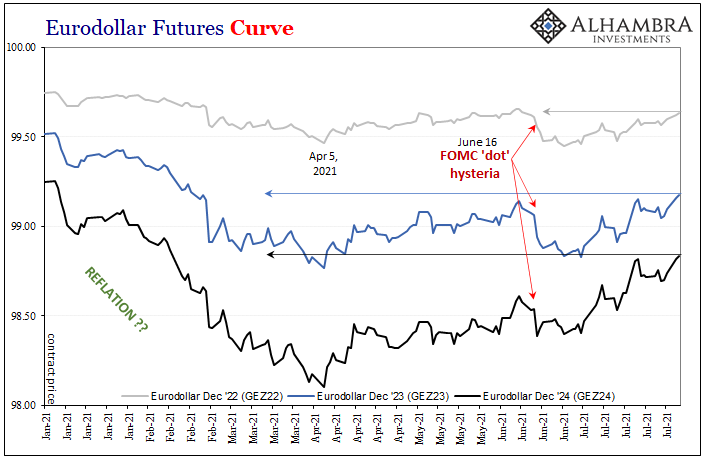

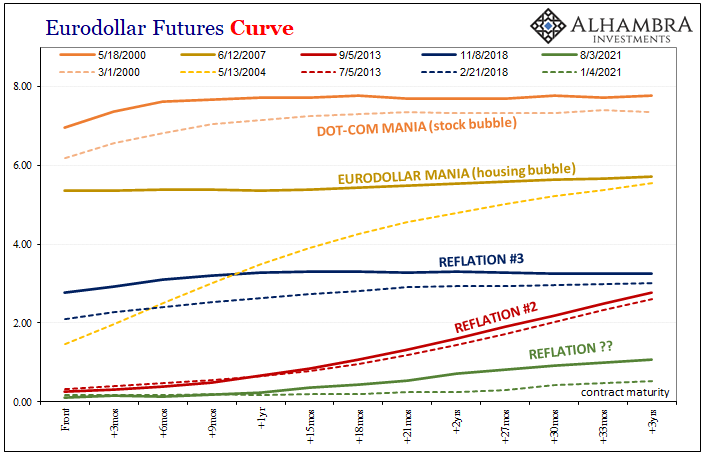

Not only 2018-19, there was this same kind of microscale hysteria not even two months ago when the June 2021 FOMC published its “dots.” Remember them?

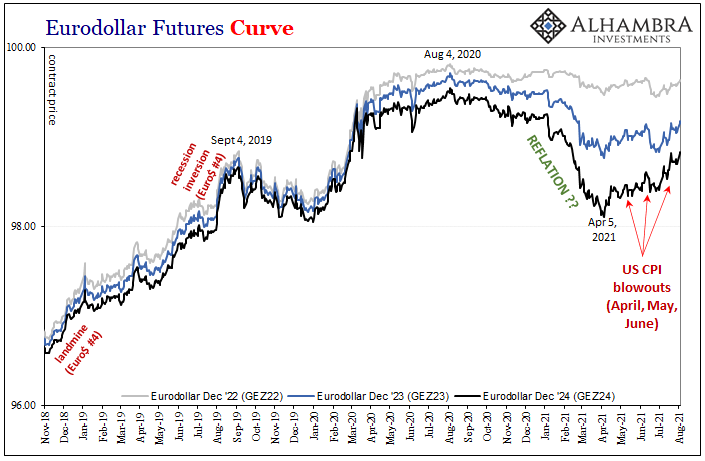

The bond market (the whole thing, not just Treasuries) did adjust to a few more of those blots moving up and left on the plot when released on June 16. In eurodollar futures, for example, being tied to and paid off in future 3-month LIBOR also means paying close attention to what the FOMC does with alternative rates; its fed funds target range and the tools, like RRP and IOER, used to achieve it.

Unlike the textbooks, however, the market doesn’t just take these officials at their current word (the whole point of the 2018-19 fiasco foretold first by eurodollar futures) and then obey by pricing curves derived directly from the mouths of monetary officialdoms. What gets priced into this curve is what the market perceives the FOMC will be able to do over the interim between now and whichever future contract strike; whether the current FOMC currently agrees or not.

These are two very different things (see: 2018-19); Fed wanted and forecast rate hikes, eurodollar futures priced cuts. Cuts were the result demanded by monetary and economic reality globally Jay Powell and the FOMC ignored.

When the dots were announced back in mid-June, this set off a minor “bump” or shift in the eurodollar futures curve. What it actually meant was the market slightly raising the chances for the dots given Jay Powell’s tenacious indifference to reality just a few years ago.

You can see what I mean about 2021 above; since the curve really didn’t move all that much even in June, the market was only pricing a very small probability of the dots coming to fruition and only on the demonstrated stubbornness of policymakers (again, 2018) to dismiss, ignore, and otherwise misunderstand the actual monetary conditions surrounding them as well as the whole world.

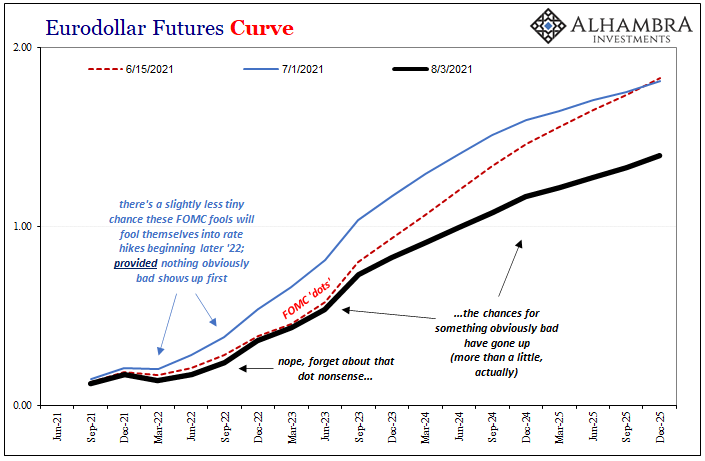

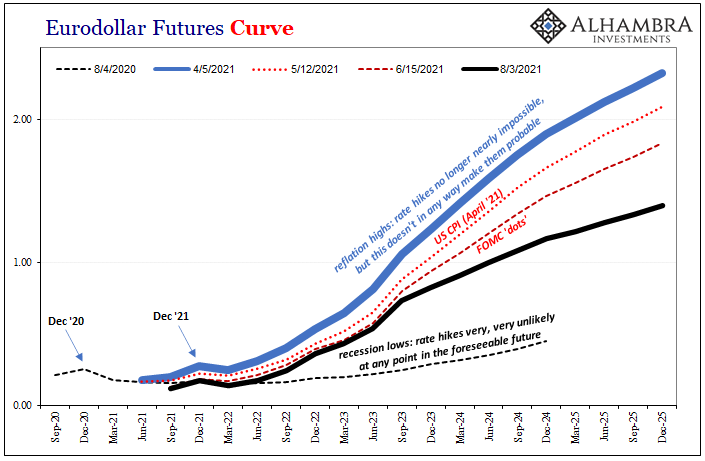

For only a couple of weeks afterward, to put it bluntly: with these dots there’s a better than nonzero chance these fools really will fool themselves into starting 2022 rate hikes. The big caveat is the same one noted above; for even this to have any possibility, everything would have to go just right in between. Everything.

That’s why – as you can clearly see on the charts above – the post-dot bump has been completely erased and then some after only a short lifespan. The curve has collapsed back, front end to back end, because the market looking globally, and actually understanding what it’s looking at, unlike the FOMC, has priced the chances of everything going right as becoming slimmer than already, uncomfortably closer to none.

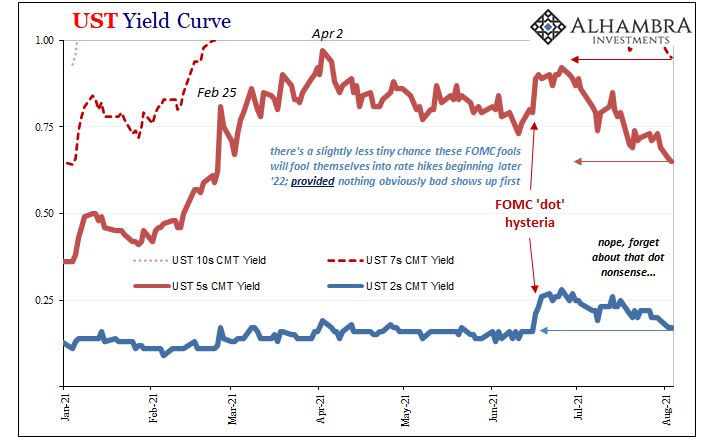

And it’s not just the eurodollar futures curve where the FOMC’s “hawkish” inflationary confidences are being deleted from current trading considerations. In nominal US Treasuries, it had been the shorter end notes which, like eurodollar futures, bumped up a tiny bit on the dots.

It didn’t last all that long in the UST yield curve, either. Now, with the 2-year back down around 16 bps, the dots are completely gone from the front; in the longer notes, even the 5s, the dot bump was gone weeks ago with more and more the long end of the curve eating away at what little remains from total reflation achieved in January and February.

In other words, forget the June dot hawks, forget taper; the market has because there are even bigger, more fundamental, and regrettably widespread (which means both global as well as monetary comprehensive like US$ collateral) concerns all over the horizon.

Waller or any of the others can talk taper all they want; the real market didn’t ever much care in June and now doesn’t care at all. Officials don’t realize, because you wouldn’t ever hear otherwise on CNBC or wherever else in the mainstream news, neither their dots nor their taper talk actually matter much where it truly counts. Instead, it is those seeking to keep Inflation Hysteria #2 alive who attempt to turn public attention toward the purported (though disproven) importance of taper and rate hikes – even as months ago things turned.

Go early and go fast? Already done, months ago, just in the opposite direction by the real monetary authority (not the Fed).

The bond market, though we may live on the same planet, this is another world from the FOMC and its blind followers. Unfortunately for Earth’s inhabitants, pretty much all of them, reality repeatedly and consistently matches the bond prices.

Stay In Touch