They were doing so well, or at least not quite as bad as throughout the prior several decades. Through this year’s 5% CPI’s, Federal Reserve policymakers stuck to their gut not their heart. Transitory factors. Right call (as we’ll see in a minute).

That won’t be their mistake. On the contrary, these Economists (central bankers are all Economists nowadays, and the few who aren’t have only worked for them) continue to fall head over heels in love with the unemployment rate. Despite missing so badly the last time, just a few years ago, here they are ready to commit to their jilted love once more.

Not long ago, so unnerved had policymakers gotten about the unemployment rate’s false signal the FOMC initiated an 18-month “exhaustive” examination of the US economy, its inflation “puzzle”, and the unemployment rate’s role in it. What they found was – quite predictable if you aren’t an Economist – how the object of so much official affection had treated them so poorly.

They finally broke up in August of 2020 when officials discovered the unemployment rate was cheating on them; or cheating them.

When the Federal Reserve’s Grand Strategy Review was completed, the break up, you had to read between the lines a little and translate their academic econometric gibberish into plain English, but it didn’t take much effort:

According to [the UE rate] over the last several years, going back to 2015, believe it or not, back when this main labor market ratio first tumbled underneath what had been calculated as “full employment”, the unemployment rate has totally confounded monetary policymakers. At every turn, year after year, they judged its decline as consistent with the deviation from the maximum I just described above; the good deviation, the inflationary kind.

Yet, never once an inflationary burst nor the more important acceleration in growth we call a recovery. Because those things didn’t happen, the unemployment rate could only have been false. Yet, denial always persisted if for no other reason than CYA and convenience.

It sure seems like, and it is heavily implied (because they’ll never just come out and state this) here, these charlatans have finally acknowledged how they’ve been misleading themselves, and you, for more than a decade about the real state of the labor market therefore the overall economy.

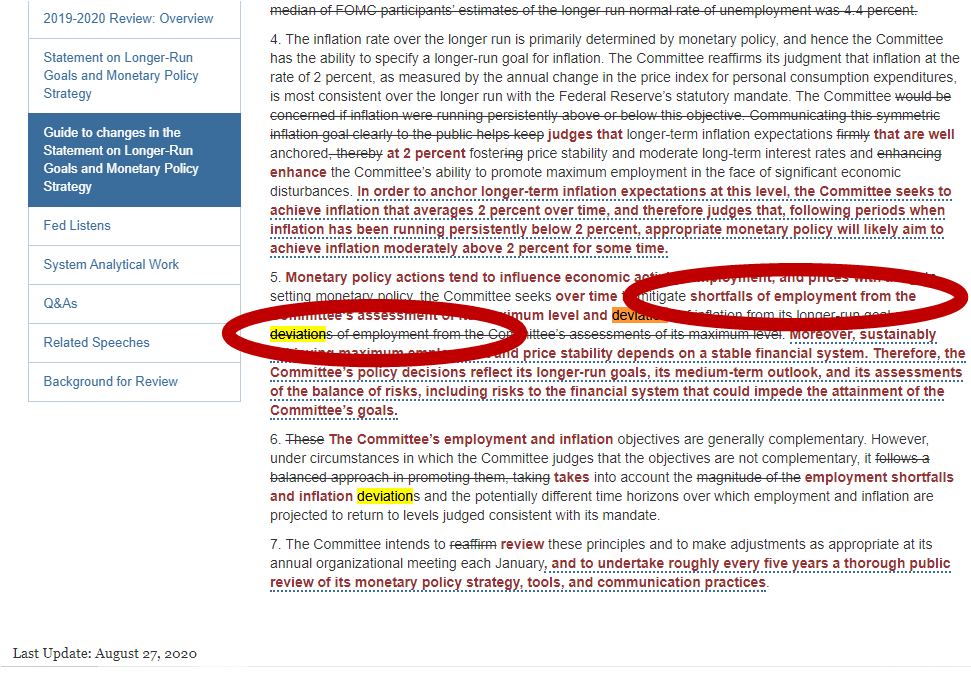

To that end, the term “maximum employment” was struck entirely from the Federal Reserve’s most sacred document.

See for yourself:

Having quasi-committed just last year to not falling into the same honey trap of falling in love with the unemployment rate, Chairman Jay Powell today at Jackson Hole indicated that, yes, the FOMC has once more fallen in love with the unemployment rate (in the manner Fed Governor Waller had laid out mere weeks ago). What Powell said today in Wyoming was:

My view is that the “substantial further progress” test has been met for inflation. There has also been clear progress toward maximum employment.

When former Chairman Ben Bernanke said near exactly the same thing, referring to progress in all the same factors, the “taper tantrum” which followed sharply contrasts to the reaction in significant markets (meaning: not stocks) after Powell’s remarks earlier this morning. Yields are down.

Why so different this time?

Perhaps the very amorous hearts of “monetary” officials have been so captured by that object of their affection, the unemployment rate, they simply don’t realize how after breaking up with it last summer they still hold dear all their same feelings anyway. Lovestruck dumb.

The bond market, however, isn’t under the same spell or subject to the same illusion. As I wrote almost two weeks ago, there was every reason to expect taper without tantrum in 2021:

The key part behind both the Fed’s [2013] tapering as well as bond yields surging upward was actually the same thing, another thing, rather than the former driving the latter. In other words, “…confidence that that is going to be sustained.” The second “that” being economic progress – legit economic progress.

Whereas the bond market in 2013 was becoming somewhat more confident (not for long) in the idea of legit economic progress behind Bernanke’s taper, the bond market in 2021 is, forgive the expression, crapping all over Powell’s.

Dovish my a–. This need to pretend the Fed is in charge is downright pathological.

— Jeffrey P. Snider (@JeffSnider_AIP) August 27, 2021

What Powell said today was the *same* thing as what Bernanke had said in May '13.

Why such a different reaction this time? I told you two weeks ago taper w/out tantrum.https://t.co/L3yCkzlVeF

Powell Aug '21: slowing QE "could be appropriate"

— Jeffrey P. Snider (@JeffSnider_AIP) August 27, 2021

Bernanke May '13: "we could in the next few meetings, take a step down in our pace of purchases."

Why totally different responses in bonds (which actually matters if you care about labor, econ, the world)?https://t.co/E9b0PEBI59

The unemployment rate has seduced the FOMC for the third time. Fool me once…

Therefore, it will not likely be of much comfort for policymakers that “transitory” past “inflation” (which will mean it wasn’t inflation) continues to be evident in actual data.

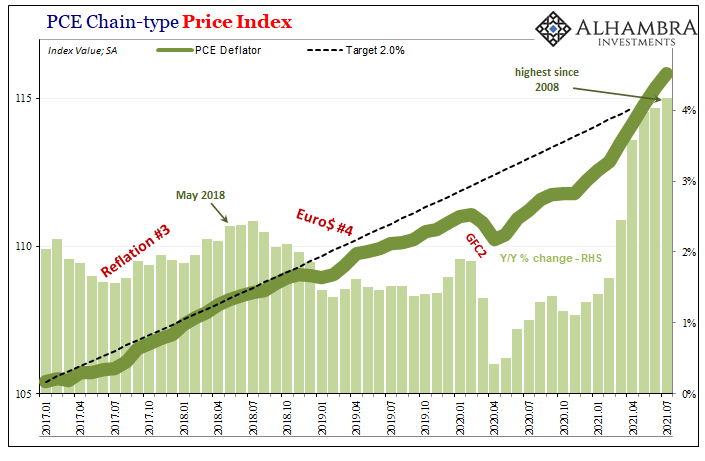

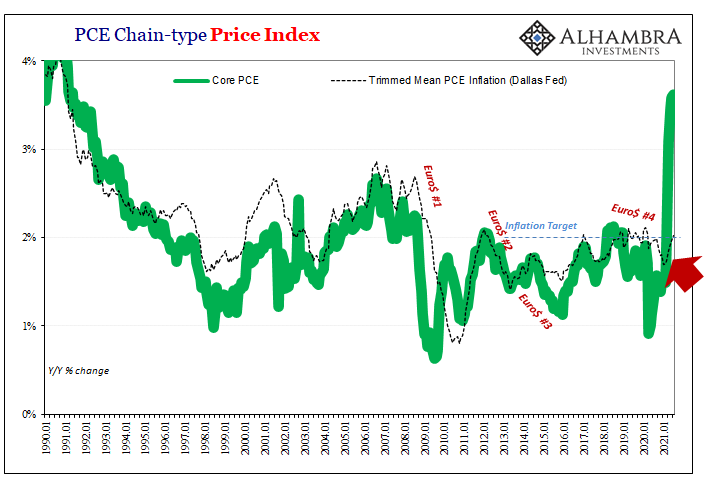

The PCE Deflator for July 2021 is rendered stale by the CPI’s release two weeks before it. Either way, the FOMC prefers the former and it is, like the CPI, already coming around more than around the edges. The year-over-year change elevated to 4.17% for the overall bucket, but the monthly change (seasonally-adjusted) has softened for the third straight month.

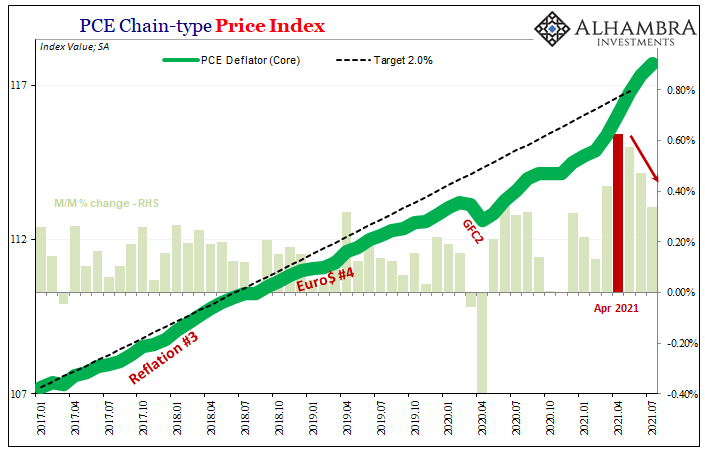

Same for the core PCE Deflator, up 3.62% in July 2021 compared to July 2020, but “only” 0.34% when compared to June 2021. The short run rate of change has clearly downshifted, pointing to a past peak in that same month of April we keep running across in inflation as well as market data around the world.

On top of the growing evidence for “transitory”, the Dallas Fed’s trimmed mean PCE Deflator strikes another factor from 2021 “inflation” – consumer price data has been driven by a suspiciously narrow set of prices (autos and gasoline). Actual inflation, to be actual inflation, is broad-based and sustained for a prolonged period.

All of this means the Fed seems to have gotten this year’s “inflation” right for the right reasons, but is now committing to the same errors when interpreting the unemployment rate setting them up – and all those blindly following the romance – to immediately squander their first victory in forever.

There are any number of easily-observable reasons why there isn’t any tantrum to this year’s taper. Though this year’s “inflation” wasn’t inflation, there isn’t much chance next year’s is even close to that insufficient. Why not? Since we’ve got the two love-struck fellas, Bernanke and Powell, the answer to this unlovely “conundrum” provided by the cold-hearted lady Yellen in that suspiciously brutal (see: above) year of 2014:

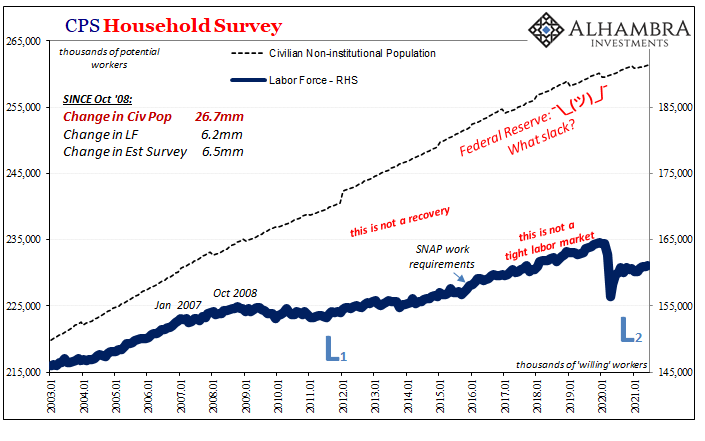

Ms. YELLEN. But when we see diminished labor force participation among prime-age men and women, that suggests something that is not just demographic. And so my personal view is that a portion of the decline in labor force participation we have seen is a kind of hidden slack or unemployment.

Stay In Touch