We are going to start here with Europe before heading to Australia and then getting to China – and then currency. Why the ECB? It is going through the same pangs of dissatisfaction as its cousin the Federal Reserve had last summer. Like the Fed in 2020, Europe’s central bank in 2021 has climbed to the end of its grand strategy review and following its own come to the same conclusion as that other.

Symmetric inflation target requiring more nuanced forward guidance.

If you aren’t distracted by the shiny wrapping, you realize what Powell’s saying is that after failing to hit the inflation target for over a decade he’s now going to let inflation run over the target none of them could hit because for more than a decade no one could hit their own target.

A few weeks ago, Philip Lane – the ECB’s Chief Economist and a member of its Executive Board – wrote at some length about what’s being called for after adopting symmetry. It is a true piece of art, though not in any way the way Mr. Lane was shooting for. Though the financial media just eats this stuff up, the more these central bankers back themselves into an inflation (meaning monetary) corner the more they end up exposing their scam.

I’ll just sample one bit here relating to “forward guidance”, which for the 21st century central banks is a key component of what they actually do. You can and really should read the rest of it, if only to see for yourself what emptiness passes for policy:

Finally, the sentence that the forward guidance “may also imply a transitory period in which inflation is moderately above target” makes explicit that rate forward guidance that is committed to avoiding premature tightening may imply that inflation runs moderately above the target for a temporary period.

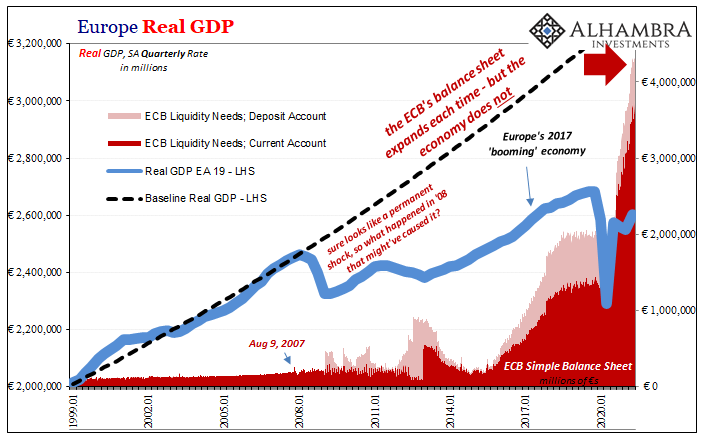

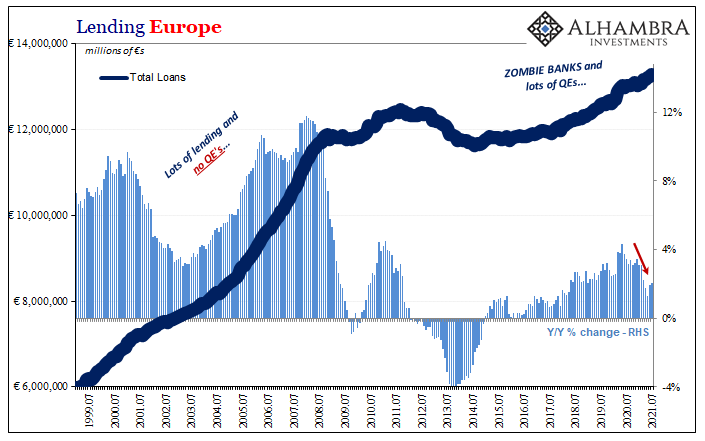

It all begins with attempting to explain the last decade-plus since the first Global Financial Crisis “no one” saw coming; the very monetary event which led to situations around the world – no matter what central banks did – when rates plunged and then stayed down.

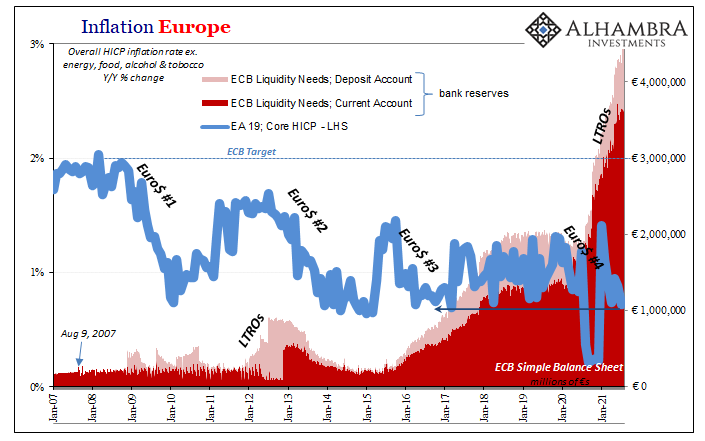

Symmetry is believed necessary as a consequence of low interest rates and their proximity to the nominal zero lower bound (or below it, as in Europe’s case). Thus, being near the ZLB requires an especially forceful response (more and more serious words) to overcome that boundary.

But a huge monetary response, as the everyone knows, or, truly, as the media sells it, is intensely powerful (“pouring trillions of dollars/euros/yen/etc. into the economy”) which can only mean (in theory) that financial market participants view it as eventually quite inflationary. Abundantly inflationary.

However, since we also know that central banks are vigorous inflation-fighters, the mere expectation for higher inflation because of how awesome more forceful monetary policies have to be leads markets to prematurely price eventual policy tightening thereby choking off that very inflation meaning recovery.

Its own success is its failure!

Thus, in order to combat this ZLB expectation which leads to inflation expectations and then the wrong set of policy expectations, the ECB (like the Fed) is introducing this new forward guidance and symmetry to add yet another layer of expectation to be intertwined within this pretzel of torturous “logic.”

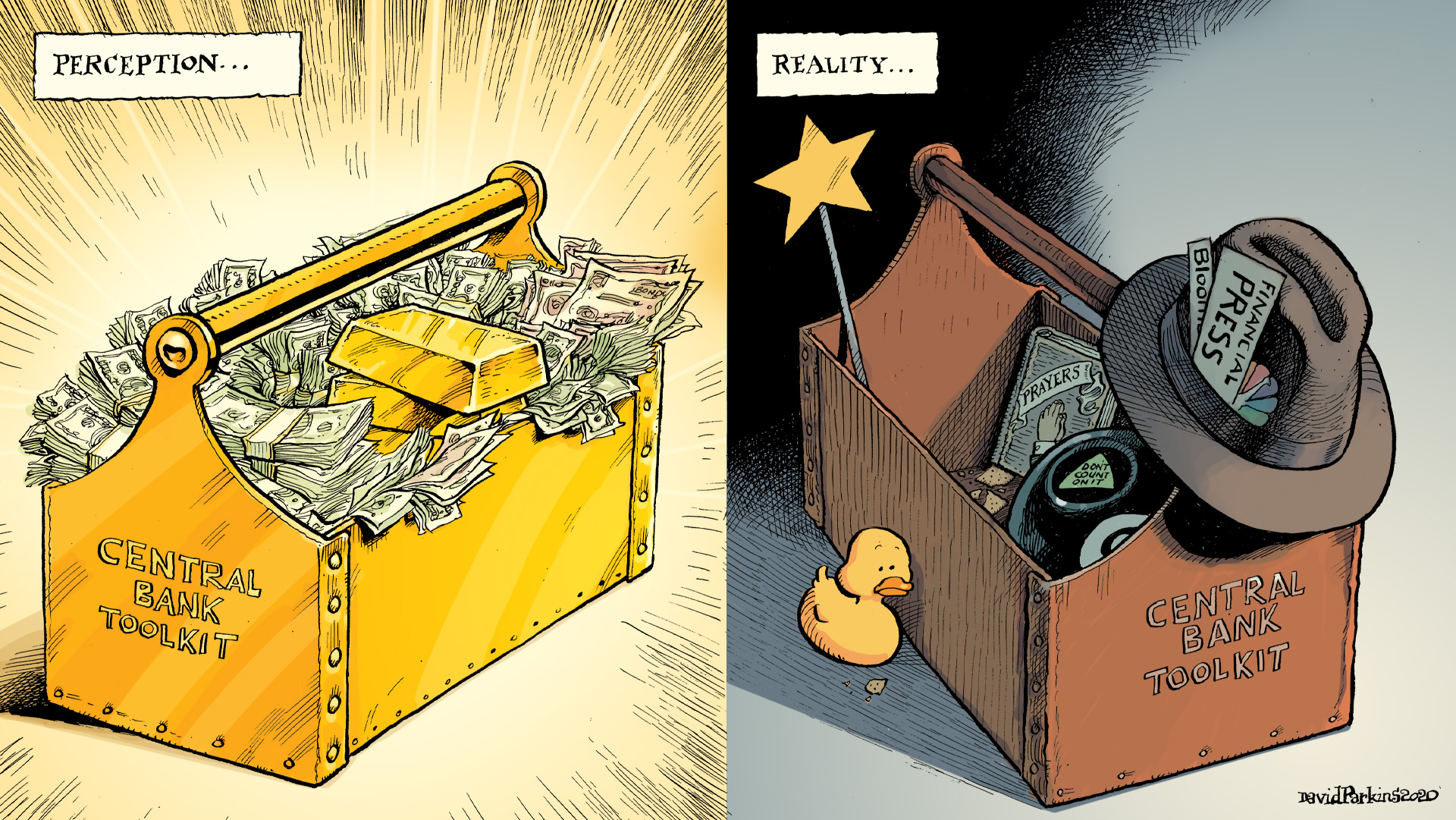

There’s no money in this monetary policy business, mind you, merely a network of ad hoc theories which can never explain how anything works nor how everything else got into this mess and stayed in it. Central bankers aren’t monetary stewards, they attempt pop psychology via unnecessarily convoluted trains of contradictory concepts because their North Star, their God That Cannot Fail, is their words.

Monetary policy is extremely powerful simply because they say so.

So awesome, this “easy money” verbiage, that it constantly needs addressing and updating because the symptoms consistent with actual easy money never materialize (some more honest folk might see this as falsification, which is not allowed in cults).

Keep all this in mind as we head next to Australia and beyond.

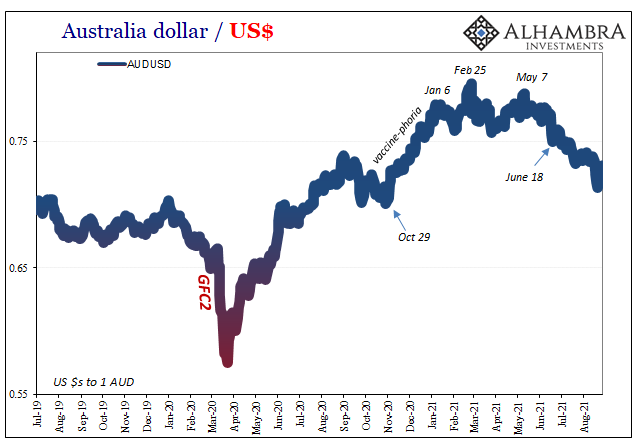

What I wish to point out from Down Under is the Aussie dollar and its exchange relationship with its US counterpart – which in reality means eurodollar rather than technically US dollar.

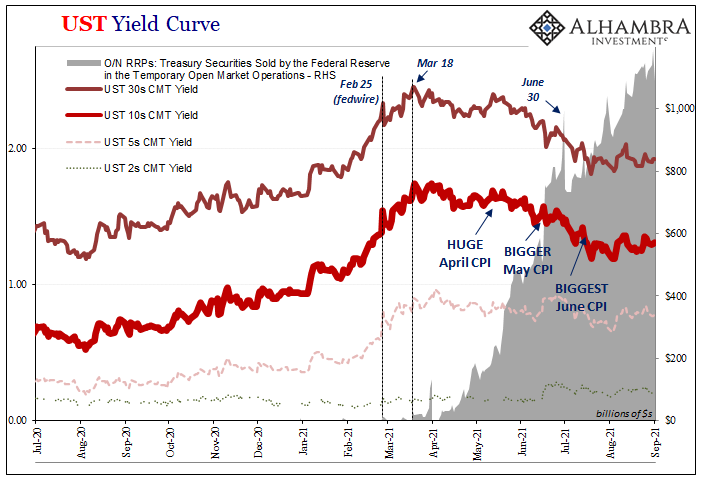

It’s been moving lower (rising USD) since February 25 (Fedwire), no surprise. It took a real tumble, however, around June 17 and 18.

AUD isn’t just correlated underlying with eurodollar conditions, it is likewise especially linked and susceptible to the same which go along with China. As you’d expect, Australia is at the margins one of China’s closest economic “colonies.”

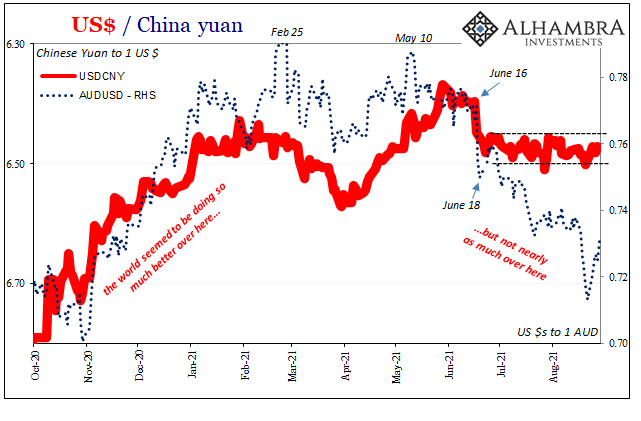

The same spike in US$ (bad) which registered in the Aussie not surprisingly shows up in CNY. Again, around June 17 and 18.

What’s perhaps more important is that since June 22, CNY is no longer moving much at all in either direction. The quasi-peg remains in effect to this first day of September, meaning more than two months. That’s then the real stealth money of one of the few actual central banks left on the planet: PBOC.

As I worked out here, the cringe remains; not something you really want to see and therefore a backhanded indication of relative seriousness.

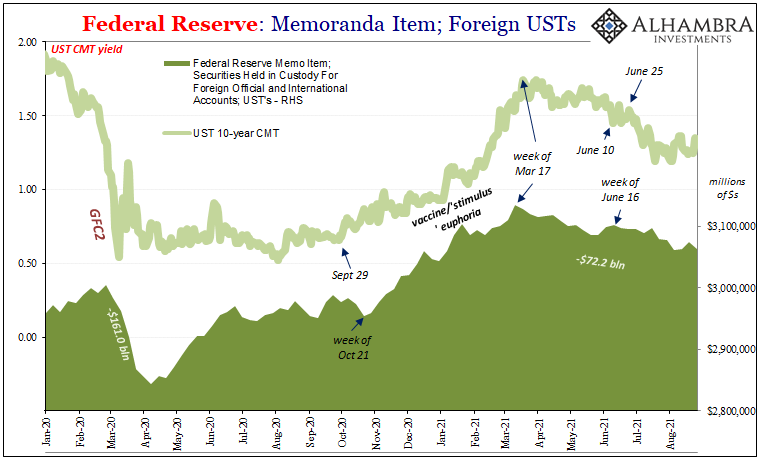

So, we have to ask, what was it mid-June that seems to have so disturbed the eurodollar system as to have forced Big Mama’s, as the PBOC is known, interventionist hand?

Yes, reverse repo.

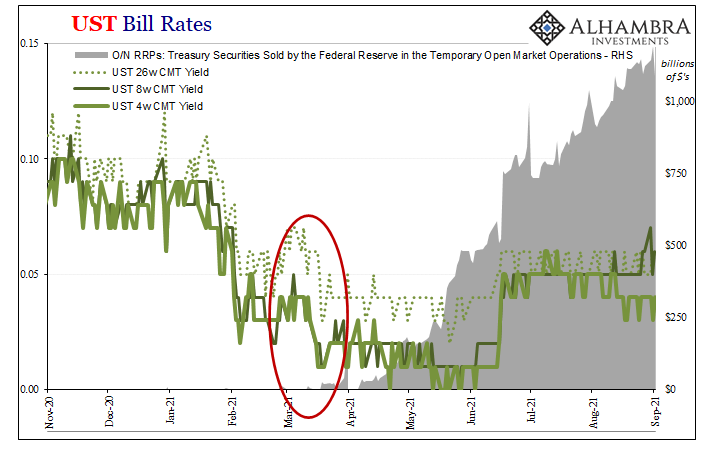

June 17 just so happens to have been the first day that the Fed’s new RRP rate came into effect. An increase of 5 bps from the zero lower bound, the same one the ECB seeks redress over, which doesn’t seem to be much of an issue by itself.

By raising the RRP, the Federal Reserve was meddling in affairs way beyond its ken; actual monetary affairs. In trying to better control misbehaving T-bill rates (and GC repo), to portray some competence, Jay Powell’s gang actually revealed their further incompetence and the real issue.

I wrote about it specifically right on June 17:

Here’s where the FOMC has done us a huge and inadvertent service; by raising the RRP 5bps off the zero lower bound, it has given this bill, collateral premium the space to “show itself.” Which, on the very first day of the new RRP rate, it just did…

The reverse repo is at 5, yet bill yields at the 4-, 8-, and 3-month maturities are all less than this. Why? It can only mean this one thing, a premium relating to value for some other utility, otherwise nothing would ever yield below this secured alternative with the Federal Reserve. Who would buy a 4- or 8-week UST bill returning one and a half maybe two basis points less than lending to the Fed secured by the same instrument?

If there wasn’t a collateral constraint, the RRP would act like a hard floor. It isn’t and we’ve seen this before. Thus, why UST note and bond yields, for example, have almost perfectly correlated with RRP usage in the “wrong” way.

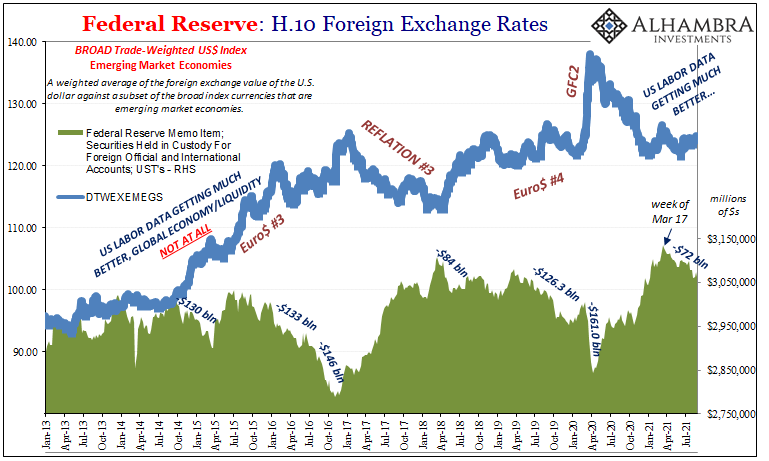

By moving a little bit off the ZLB, the Fed all but confirmed the primary underlying issue as one of a collateral instead of “too much” money from overly abundant but largely useless bank reserves. If it really was about this digital flood of dollars, why only increasing and increasingly global deflationary indications, pressures, and further potential?

In the wake of Federal Reserve officials dipping their ignorant toes into the real monetary world, rather than sticking with the scripted universe of speechifying, it has left the PBOC (and certainly others) to deal with the further fallout and consequences – deflationary potential consequences – as best it can.

In China’s case with CNY, in a way (cringe) no one ever wants to see. It began back in late February, picked up a huge wave in March, and then the Federal Reserve pushed it further along in the wrong direction because those at the Federal Reserve like those at the ECB are only good at playing central bankers on TV.

COVID? Weather? Chinese emission controls?

No, dollar; eurodollar. And it all begins (therefore doesn’t end) with central bankers who aren’t central bankers, who believe in the ultimate power of their own voices than stoop to studying the real money plumbing in order to find then do something useful about its structural shortcomings.

This here is my own overly verbose way of saying, forget inflation since the real monetary world has because nothing truly has changed. Words are neither euros nor dollars, and they sure haven’t been eurodollars.

Stay In Touch