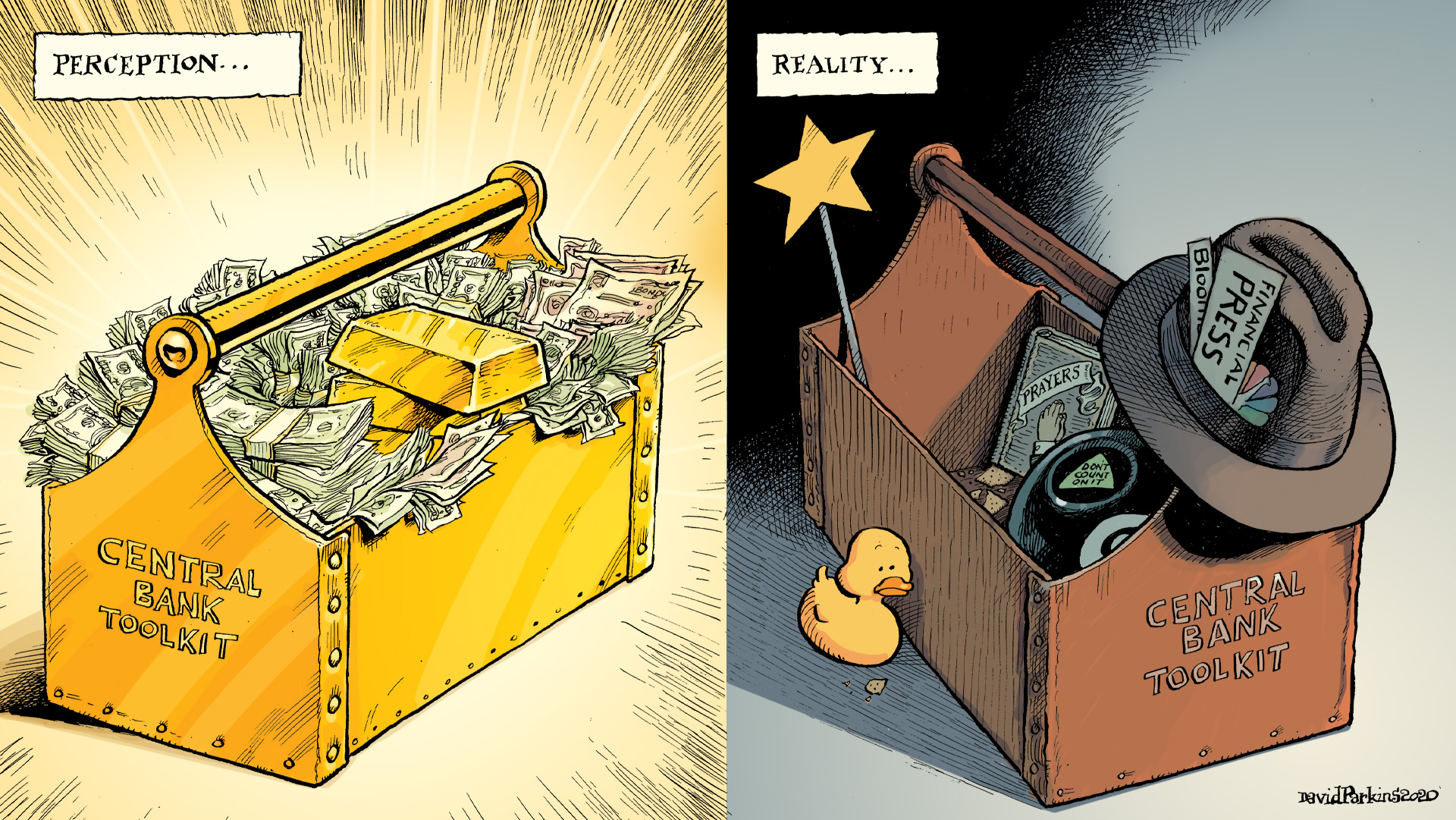

Central banking’s real monetary power comes from a different kind of printing. We’re all taught and told from the very beginning that it’s derived from enjoying the money printer, the ability to stack currency at will. No. In actual fact, monetary policies are all money-less leaving “monetary” authorities to employ instead the press which prints words.

Deciding which words, and more importantly what they mean, now that’s not at all what they teach you in school. The closest to this truth is the fuzzy concept of “moral suasion”, but even when that’s brought up and out it remains closer to a lie of omission (while the idea is introduced, it is only said to be a small part of what central bankers do rather than their entirety).

Officials talk and we’re supposed to just take the words at the face value printed up in the financial media. This is how we can get to something like this (note the title):

The challenge was to mitigate the rising cost of prolonged easing to financial institutions, without giving markets the impression the BOJ was headed for a sharp exit from easy policy.

In a functioning society with a Fourth Estate which hasn’t abandoned its core mission to question authority with fact(s), such a sentence would never have been put forward to an editor, let alone get passed around between what few of them remain and then somehow approved for publication. What’s written above is a bald-faced absurdity, a complete contradiction and one so plain it would be bewildering if not for the context from which it has been written.

This is, sadly, standard for mainstream content when it comes to central banks.

Think about it: “rising cost of prolonged easing.” Not just a greater burden, this larger hardship of “easing” being thrust upon “financial institutions.”

Call me old fashioned if you will, but just common sense dictates that “easing” means – in every monetary context – that it gets easier for, you know, financial institutions.

What can they even be talking about here? Specifically NIRP, but really overall everything central banks really do.

The world’s peoples have been fooled. The greatest trick that devilish Greenspan ever played was to get the world to believe the money printer exists and that central banks wield it. They don’t (and Greenspan knew it).

By conjuring and then constantly reinforcing this image of impossibly fat stacks of new literal cash printed out at the push of bureaucrat button, it came to be believed that central bankers would never have to even use the thing; they could substitute their words and other actions as they would like. Thus, if Central Bank A does X, and Central Bank A says X = easing, no one questions the sequence.

But what is “easing?”

It must have a literal meaning outside the envelope of central banker-approved discourse. Before this Orwellian era of doublespeak, it had been incredibly simple and intuitive. People didn’t require second-, third-, and fourth-party interpretation.

More money means banks can do more of what they are supposed to do. Lend in the real economy. Those very financial institutions in question, when they have more money at their disposal or within easy reach, no one should expect much other than higher scores of credit and therefore sustained growth. Inflation, even.

The lie of omission is in skipping those intermediate steps; Central Bank A does X and we are all meant to assume those fruits of easing will show up without fail. In fact, so incredibly farcical, our assumptions are the whole point as current theory presumes by getting us all to believe that will be enough for all of us to act and in us acting on being fooled that is how the intended monetary goal will be met.

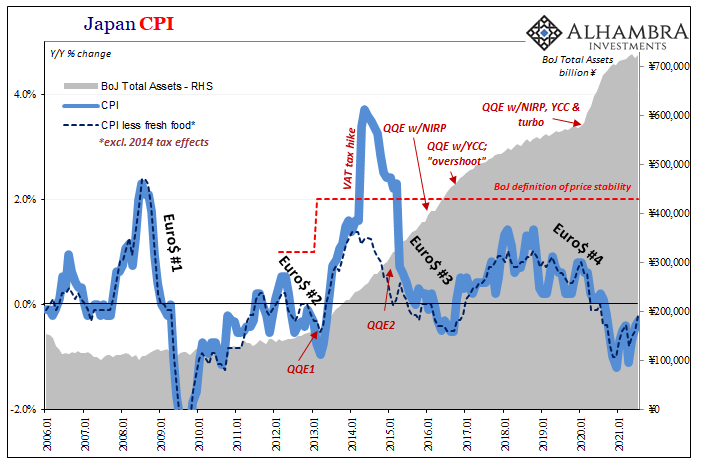

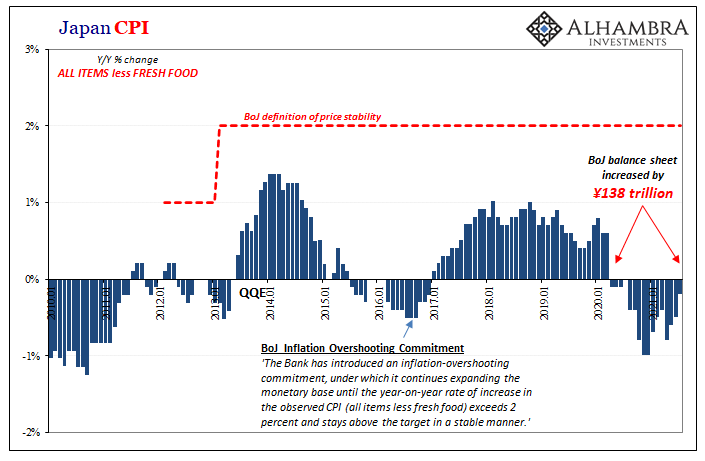

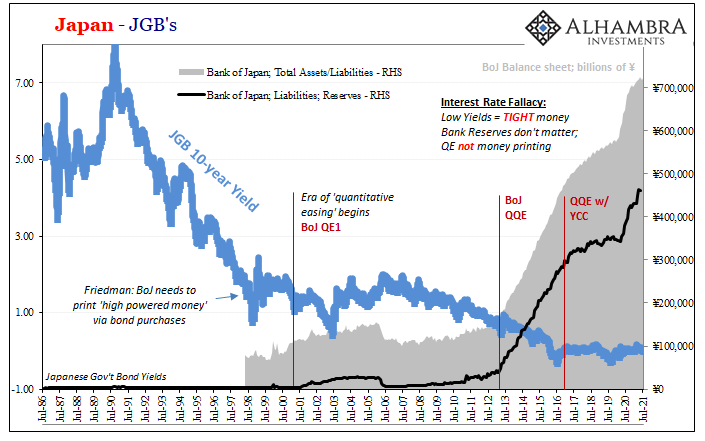

The ridiculous paragraph I quoted above (thanks to J. Fraser for flagging it!), as well as the stupid one I just wrote, pertains to the Bank of Japan suddenly rethinking this whole QE stuff. As we’ve heard for a dozen years here in the West, and for over twenty in Japan, QE is money printing since, “they’ve” said, the result of bond buying (or broader asset buying) is more and more bank reserves.

Bank reserves are classed as money, some even claim base (or high powered) money. More of that stuff = easing…in theory.

In practice, no dice. Back to the same article:

Amamiya and his top lieutenant Shinichi Uchida have worked behind the scenes to make Kuroda’s complicated policy framework–a product of years of unsuccessful attempts to revive stagnant consumer prices–more manageable, and eventually return Japan to more normal interest rate settings, even as the economy struggles with the pandemic.

The BOJ’s dwindling monetary options mean the two ambitious technocrats are instead pushing the bank into schemes bordering on industrial policy, such as those designed to encourage bank sector consolidation and green finance. [emphasis added]

Think back to the first time you ever heard the term quantitative easing. Whenever that was, there was never any doubt about it, right? This was always, always said to be the biggest, most impressive display of raw power and authority ever conceived. As I wrote “celebrating” QE’s twentieth earlier this year, from the very first Japanese one way, way back in ’01:

In the mainstream view this stuff is still made to sound so very simple and easy. On QE’s very first day those twenty March’s ago, CNN (and every other news outlet) claimed, “The BOJ’s move injects a large amount of money into the Japanese economy — known as quantitative easing.” The media still writes the same thing every time another QE rolls off a seemingly boundless assembly line.

Remember, also, how Haruhiko Kuroda’s QQE (April 2013) was said to be the ultimate “bazooka” even Paul Krugman had been impressed (the “credibly promise to be irresponsible” guy).

Now all these years later most of the same policymakers are tacitly admitting it was all a spectacular dud! From loudly claiming indisputable effectiveness ahead of time to quietly switching gears after the fact. Always and everything to avoid having to admit to real science; maybe none of this is actually easing. Maybe, just maybe there isn’t any useful money in any of these “monetary policies.”

If this other is and has been true, how would it look any different from this:

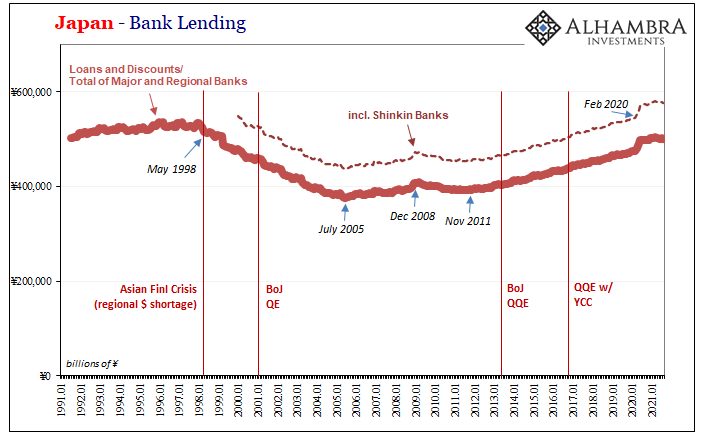

Bank lending in Japan (as everywhere else QE is practiced) remains less today – even after the 2020 bump due to panicky corporations – than there had been at the start of 1998. The combination of ZIRP and QE has accomplished diddly despite only more obscene levels of them over time (just how obscene, see further below).

No matter what “easing” pursued by the Bank of Japan, bank lending peaked during the Asian Financial Crisis (as discussed in more detail here, shown above, 1998 really was the final nail in Japan’s coffin of a Lost Decades) and then declined a ridiculous 30% despite zero interest rate policy (ZIPR) and then QE; two of them.

Those made zero difference as bank lending would not bottom out until the middle of 2005 (just as QE was ending), and, here’s the ballgame, it has never really come back.

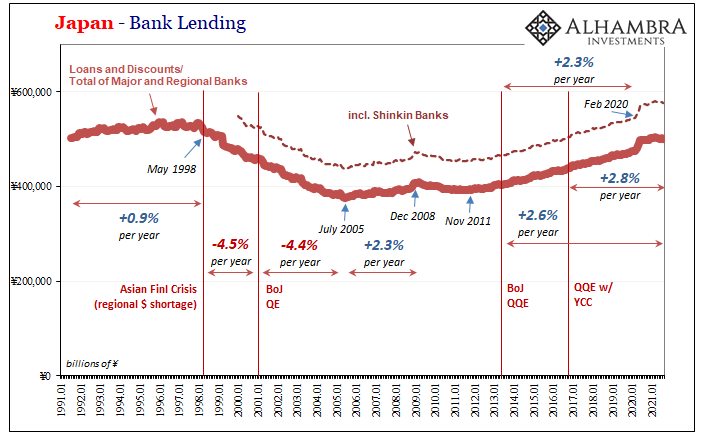

Between the start of 1998 and the first QE in March 2001, bank lending (not including Shinkin banks) declined at a 4.5% annual rate. From the start of QE1 until July 2005, bank lending declined at a…4.4% annual rate.

From then on, with QE1 and 2 being terminated in early 2006 (and even rate hikes), lending then restarted to the tune of a +2.3% annual rate to the end of 2008 (interrupted, obviously, by GFC1).

Japanese lending would again bottom out in November 2011 (despite several “modest” QE’s and long before the QQE) and from the start of Kuroda’s bazooka progress at a 2.6% annual rate through the latest figures for August 2021. It was only slightly better for QQE w/YCC, September 2016’s attempt to print more words in place of useful money, but each of those are benefiting from the March-June 2020 surge in lending which had nothing to do with the Bank of Japan.

Up to February 2020, Japanese lending under QQE was exactly the same annual rate (2.3%) as the non-QE years of 2006-08.

Most important of all, none of these rates of increase are anywhere close to a growth-inspiring, inflation-confirming economic recovery. So I ask in place of what the media should: just where is the easing, Mr. Central Banker?

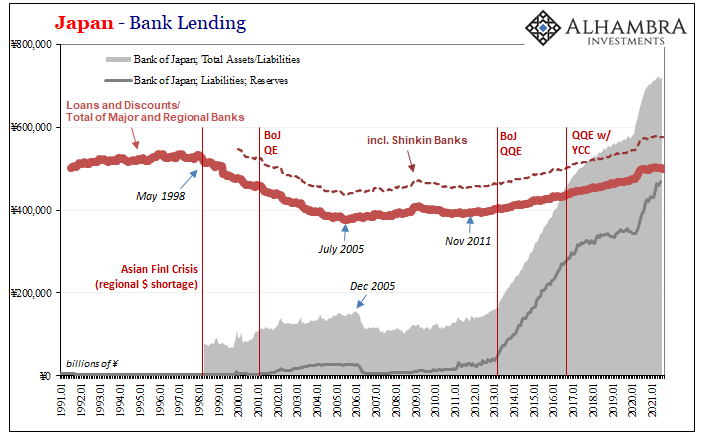

By June 2016, the Bank of Japan’s balance sheet, swelled then by a mere three years of QQE [dud]zooka, in that month BoJ’s holdings surpassed the total level of loans and discounts reported by all of Japan’s major and regional banking institutions. By August 2021, there were very nearly as many bank reserves as total bank loans.

I ask yet again: where’s the damn easing?

The media uniformly reports on “easy money” before then all the ways in which there could never have been actually easy real money while never once noting, questioning, or examining these gross inconsistencies. At most, something about stock prices. It is the words “easy” and “easing” which constitutes the business end of intended policy; the paragraph cited at the outset here just one perfect example among countless others.

So, after having failed at QE’s and QQE’s for twenty years, these Japanese central bankers (along with others around the world) are going to ditch “injects a large amount of money into” whichever economy in favor of, presumably, injecting what they know the media will still write is a large amount of money this time into specific industrial and service sectors (ESG, as one place to start).

From dumb bazookas to smart bombs?

It’s all lies. In fact, the theory itself totally depends upon the entire world buying into them. That might work for some financial markets grossly detached from physical reality (cough stocks cough), but the plain fact is no one can solve a real monetary problem with fairy tales and news articles championing little more than bad pop psychology.

Merely printing the word “easing” over and over and over will never be on the money. This whole nightmare ends when “we” are honest about what should be incredibly easy.

Stay In Touch