It is costing more to live and be, so naturally people are looking for who it is they need to blame. Maybe figure out some way to stop it. You know and feel for the basics since everyone’s perceptions begin with costs of just living. This is what makes the subject of inflation so difficult, even more so in the era of QE.

Money printing, duh.

By clarifying the situation – demonstrating over and over how there is no money printing therefore there can’t be inflation – we aren’t saying that prices aren’t rising. They obviously are. But by dispassionately analyzing the situation given its clear lack of any monetary basis, what we are doing is pointing out what instead must be responsible for driving costs of living higher.

And what that means for the future.

If it isn’t money – it’s not – then that changes the entire macro picture. These price pressures should be temporary given what’s not actually behind them. They are already proving to be as another monthly CPI rolls in and quite predictably it’s nothing like those from earlier in the year (only a few months ago).

The annual rates of change are similar, though monthly rates have diminished back to the disinflationary paces of the pre-COVID period. And even the annuals are topped out, many of the indices peaking back around April and May, June at the latest.

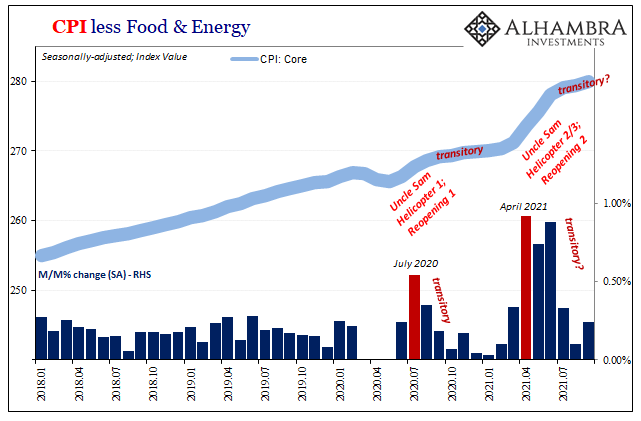

The BLS today said the overall CPI gained 5.39% (unadjusted) in September 2021 when compared to September 2020. A small bit faster than August’s 5.25% with oil prices moving higher, yet equal to June’s likewise 5.39% and not that much different from May’s 4.99%. No more huge acceleration.

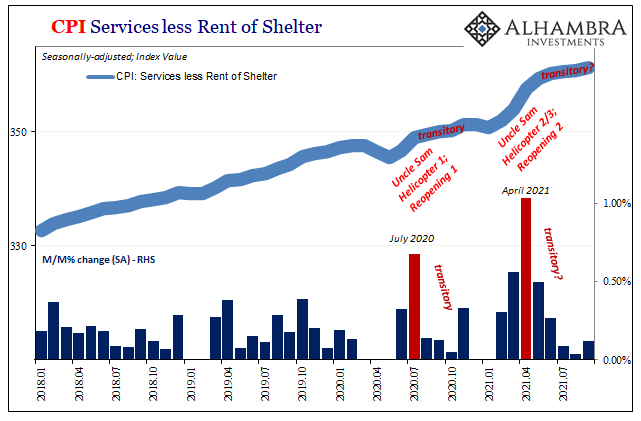

The core rate increased by “only” 4.03% year-over-year last month, just a touch quicker than the 4.00% in August yet down from June’s high of 4.37%. The monthly changes better display just how this really is establishing “transitory” (below).

Outside of goods, these consumer price bulges – Emil’s two-humped camel – are even more clearly defined (above). As the frenzy of consumer buying in especially durable goods fades further, the downward influence from the service sector which never really got going at any point along the way is what rises. Services point to even more serious weakness, therefore deflationary tendencies and ongoing potential, than when the last recession process began (in 2019, not 2020).

All of this in sharp contrast with five decades ago.

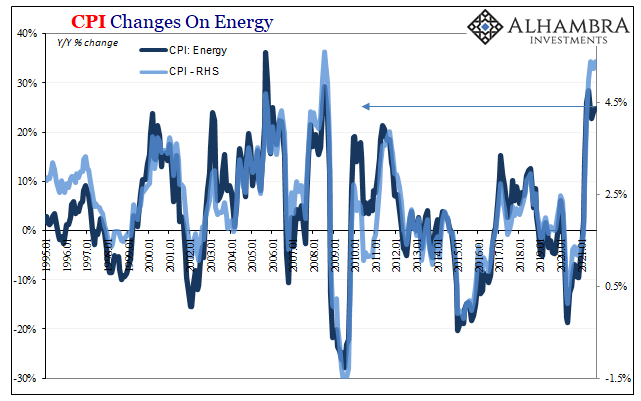

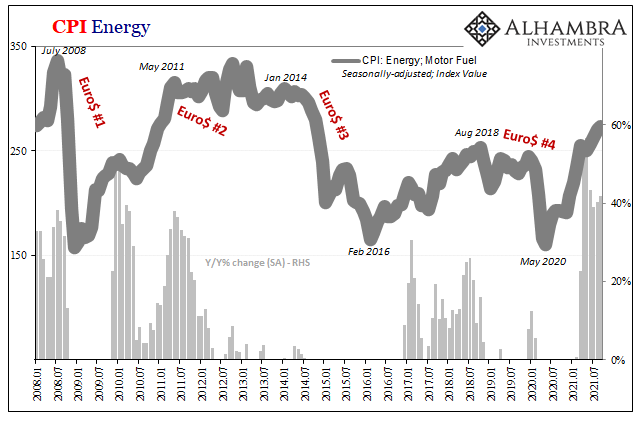

The Great Inflation was relentless, and it was everywhere. Start with gasoline prices, one of the key substances of the seventies which everyone who lived through it remembers only too well. While pump prices today are higher when compared to the past few years, they are actually significantly lower over the longer run (thanks to the opposite of money printing).

Up more than 40% from last September, which everyone notices straight away, yet 12% less than the last time the Federal Reserve began to taper its (irrelevant, not money printing) QE back at the end of 2013.

And the reason for the intermittent cost savings? Energy prices are highly susceptible to these repeated (euro)dollar shortages which don’t just interrupt otherwise inflationary conditions, they end them before they can ever get started.

So, the good news moving forward is, if the dollar and much of recent data is correct, energy prices (which lag) might not be upward bound for much longer. The bad news is when energy prices fall, though we may pay less for gasoline when they do, it’s because the global economy, US, too, goes back in the toilet.

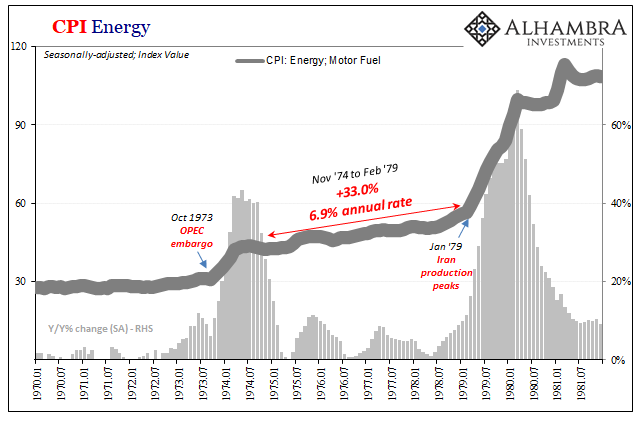

Compare this sporadic energy “inflation” with actual monetary inflation like that of the Great Inflation during the 1970’s:

While oil supply factors grab everyone’s attention for having elevated crude prices the most, even in between those two famous episodes the cost consumers paid was almost a straight line higher. From November 1974, the bottom of a very nasty recession, until February 1979 when Iran’s oil was removed from supply due to the Islamist takeover, motor fuel prices in between gained a nearly steady 7% annually.

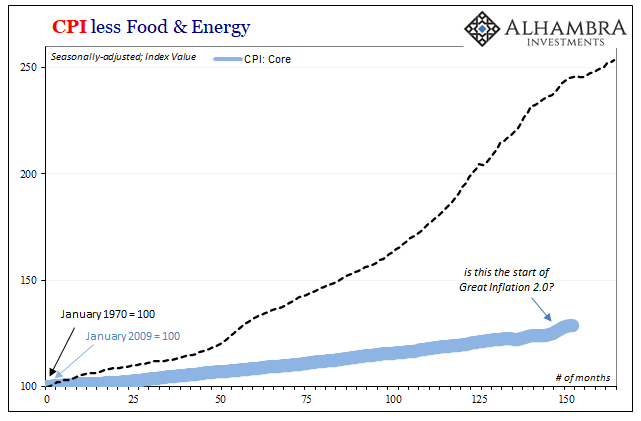

But what really made the Great Inflation “great” was that it wasn’t just oil or food. This is why we scrutinize “core” rates of inflation closely. Yes, gasoline and beef go up, those alone don’t make inflation. When the money is overflowing, all of it goes up and keeps going.

Therefore, when the core rate shifts, too, that’s when we know it’s more serious and thus maybe has that legendary money printing behind it. Note: while there really had been a boatload of money printed during the seventies, it wasn’t the Fed.

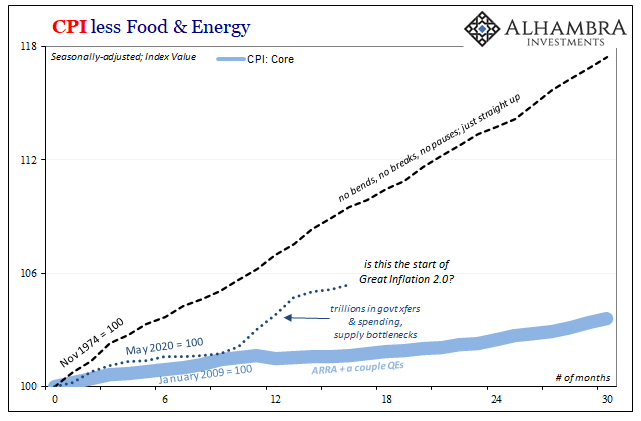

Because of this, everything goes up, core included, and it goes up year after year. No breaks. No pauses. No reversals. Nowhere to hide (for consumers). The charts below are a perfect set of illustrations of what I mean:

OK, people have finally conceded the last time, aftermath of 2008, didn’t ignite an inflationary surge like “all” the Fed’s more famous critics had proclaimed. This time, though, it’s different; many are now arguing Great Inflation 2.0 began only last year (2020) given both the insane rates of QE as well as the even more insane levels of federal government deposit helicopters (recognizing the first ineffective helicopter flew in early 2008, now much bigger whirlies this time around).

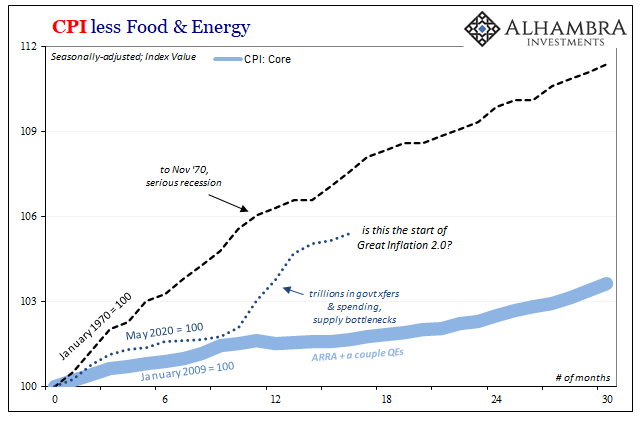

How do just the past seventeen months (since first reopening) compare to the Great Inflation from the perspective of the core CPI? Not particularly well.

If anything, the trend (camel humps) in core rates more directly reveals how much is different from the early seventies as well as what’s really making the consumer price bulge this year (and last). To begin with, core inflation just exploded during 1970 even though the US economy was mired in a severe recession! How’s that for what actual money printing can do.

Since this is the core CPI, it represents how the prices in every part of the consumer bucket went up and kept going up without letting up.

Compare that to the current period since the bottom in May 2020, and outside of those few months earlier in the year core inflation has performed almost exactly like the bottom line rather than the top. In other words, it can’t have been QE’s, rather prices pushed up somewhat by epic helicopter drops and the most substantial supply problems since the seventies.

Given all of that, didn’t even match recession 1970. Outside of those few months of Uncle Sam, core inflation remains very clearly very 2010’s.

To drive home the difference, let’s further compare the last seventeen months with that same mid-70s chunk noted above; when oil prices between supply issues rose at a sustained rate so, too, did core prices.

All this is why we won’t call what’s happening right now inflation; because it isn’t. Since it is not monetary inflation (redundant), we expected it to be transitory and, to this point, that’s proving to have been the case as each monthly update is released.

None of this is to deny that consumer prices haven’t gone up, and up by a lot – if compared to more recent years.

What we are doing is demonstrating that the “going up” part, or the camel humps, are for reasons other than “money printing.” Therefore, they are exceedingly unlikely to continue. The blame for these tremendously painful cost burdens belongs elsewhere.

This is not to led the Fed off the hook, either; policymakers are very much responsible for quite a lot because they don’t actually print any money. Doubly to blame for allowing a confused public to remain confused about QE’s and bank reserves while simultaneously being unable to fix the real monetary problem (shortage), leaving the global economy to have long ago normalized to a disinflationary world which simply means one which has been robbed of vitality and growth for a criminally prolonged period.

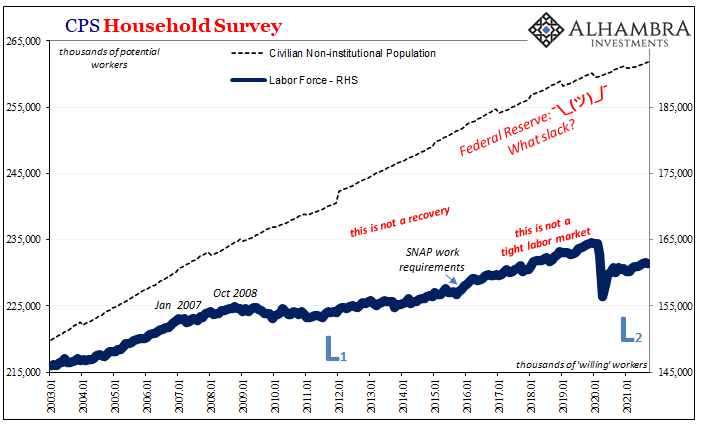

And that is what makes even these recent bulges all the more painful; workers as consumers unable to absorb them without legitimate economic growth despite all the constant talk of labor shortages and unnaturally fattened lazy couch potatoes.

Even more confusing, Jay Powell’s Fed having been right in its diagnosis of transitory about those prior humps is now committed to making an even bigger inflation mistake going forward. Frustratingly, the public has been led to believe the central bank printed too much money leading to this (these) consumer price bulge(s), while the Fed understands it didn’t and the bulge wasn’t, but because the Fed doesn’t pay any attention whatsoever to effective money conditions (how would it?), it is back to making its inflationary predictions as a matter for the Phillips Curve therefore the low unemployment rate.

Tapering later this year won’t be based on money, either, which very appropriately puts the Federal Reserve into the same category with current consumer prices.

Stay In Touch