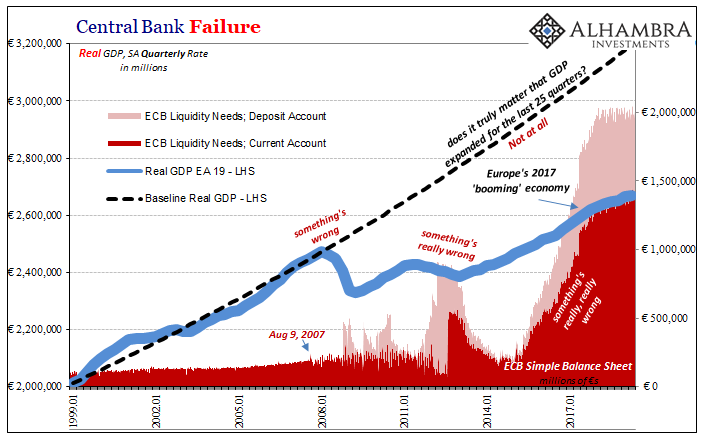

The key takeaway from Europe’s economic data dump today isn’t that the whole Continental economy is poised on the verge of recession, though that’s thrust of what’s being written about most. The reason is simple; this is all highly unexpected in the mainstream. Going by official accounts alone, there was never a hint of trouble before just recently. And many still believe this is all just overreacting.

Mario Draghi like Jay Powell made his final hawkish move in December 2018. He actually made his big error in December 2017, though. What we find throughout Europe’s economic accounts is that though the vast majority of the public is just now waking up to the danger, it’s been increasingly in danger for a year and a half already.

The turning point wasn’t sometime in 2019, it was the very end of 2017. On that there can be no doubt.

The implications are therefore profound – beginning with what really must be the cause. The mainstream is likewise filled with descriptions of trade tensions and awry geopolitics. They’ve certainly grown recently and there’s no doubt they’re unhelpful, but they cannot explain an 18-month long inflection dating back to the height of official hubris.

At the very moment central bankers were most confident about their economy, it had already turned against them. This should be a very sobering thought for anyone pinning their hopes on these same central bankers being able to rescue the system before it goes too far.

The people who said and wrote that the economy was booming when in fact it was eroding right under their noses are the ones we should look to for guidance as to how this will all turn out? Not in a sane world.

Nor should they get to describe what might (must) be the root issue here.

It’s not trade wars. The fact that this is what will be blamed anyway is simple omission. What else could be dragging down the whole world economy and all at the same time? In the mainstream, we are given no legitimate answer and in the absence of one the closest thing to plausible (sounding) will have to pass for analysis.

Some global factor with enough emphasis and force to derail the global economy over a very long period of time.

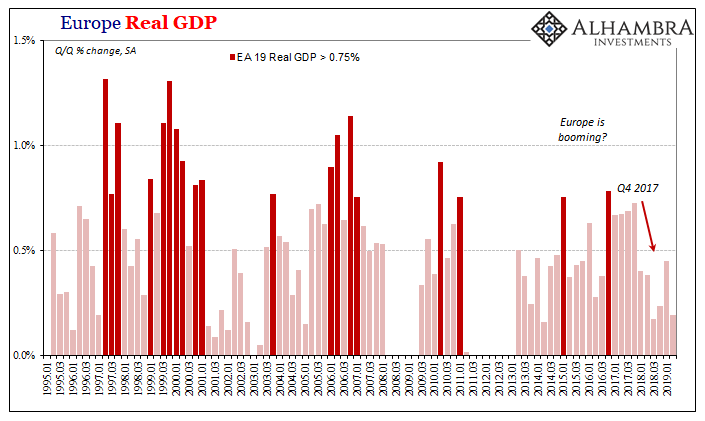

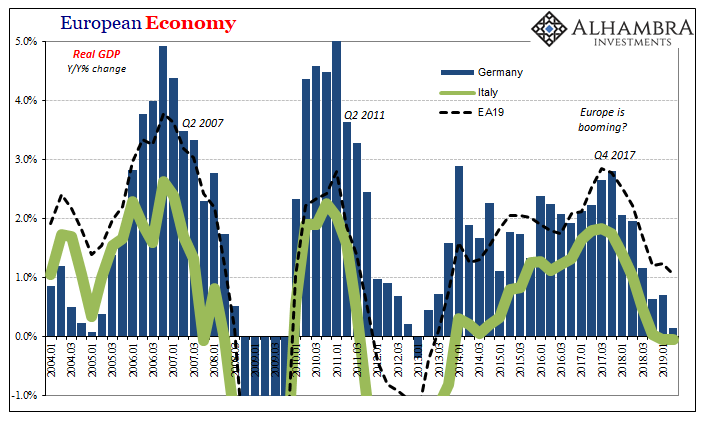

According to figures released today by EuroStat, real GDP in the second quarter for Europe’s EA19 bloc rose just 0.193% from the first quarter. Year-over-year, real GDP was up just 1.1% – the lowest since 2013.

Economic growth simply disappeared the moment the calendar flipped from 2017 to 2018. What changed in January 2018 which could have pushed an arguable boom onto a trajectory toward an inevitable bust? And why would that catalyst repeat its effects all over the world at the same time?

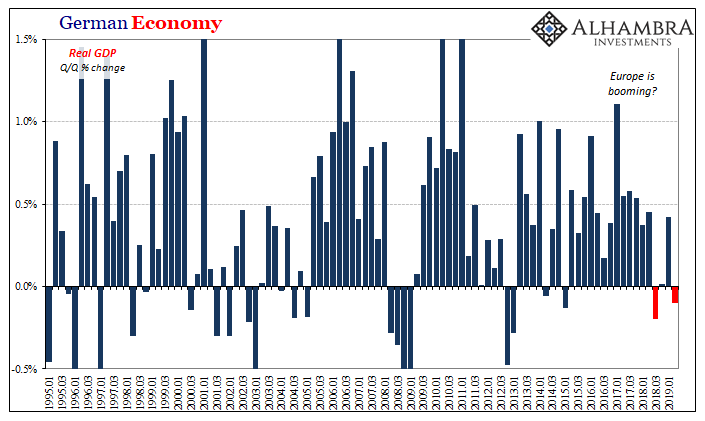

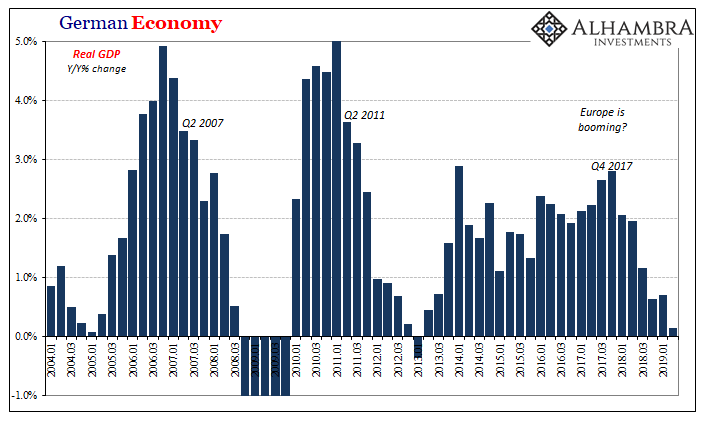

This time, though, it is the German economy which is bearing the brunt of what are very clear (and uniformly corroborated) eurodollar pressures and dragging the whole European one down with it. Real GDP for Germany contracted again in Q2, down 0.1% quarter-over-quarter. It’s not the level of contraction so much as it is now an entire year without growth. Year-over-year, real GDP is basically unchanged in Q2 2019 from Q2 2018.

Whether you view it by quarter or by yearly comparison, the deceleration all dates back to the beginning of last year.

Everyone is only paying attention now because the issue has become so obvious. It’s easy to dismiss annual growth in Germany going from 2.8% in Q4 2017 to 2.0% in both Q1 and Q2 2018 as a normal fluctuation. It was only a little harder to excuse Q3 2018’s 1.2% – Mario Draghi has reassured his public this slowing was of no concern because 2017 had been truly blistering (it wasn’t).

In November 2018, Draghi said:

There is certainly no reason why the expansion in the euro area should abruptly come to an end. A gradual slowdown is normal as expansions mature and growth converges towards its long-run potential.

Others joined in with stories about the water level in the Rhine river as well as emissions testing and regulations (which Draghi also mentioned) fouling the auto business. Unless your idea of potential is zero or negative, it couldn’t have been a combination of mean reversion and these alleged one-off factors. It’s now gone way beyond all those excuses.

Without a frame of reference in the dollar as well as the (global) bond market, these things sounded somewhat plausible. Today, they look as ridiculous as they always were. In no way was this unexpected.

With Germany on the verge of, if not already in, recession, what are the chances for the rest of Europe? What does it say about the real state of the whole global economy?

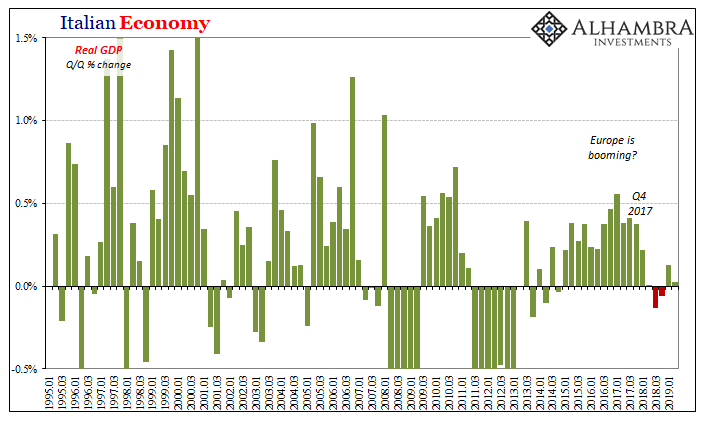

The Germans are merely leading the way downward, they are by no means alone in doing so. Again, the pattern is the same if for now at different levels. Italy, for example, has likewise been without growth over the same timeframe. Q/Q, the Italian economy managed the smallest of gains in Q2 but again all that does is confuse the lack of growth over a significant length of time.

Real GDP in Italy has been about zero or less in four of the last five quarters; in that fifth quarter, the gain was all of 0.126%.

Varying in intensity, the pattern and timing is uniform across Europe.

Central bankers like Draghi and now Christine Lagarde will say that the economy is otherwise fine but it has shown some downside risks. To manage them, the ECB like the Fed will take out some insurance in the form of “additional accommodation(s).” Whether rate cuts or QE, or rate cuts plus QE (plus tiers for the NIRP penalties), does any of it really matter?

They have no idea what they are doing and more so they have no idea why they have no idea what they are doing. Authorities all around the world have no legitimate frame of reference from which to accurately interpreting events and conditions. They have no way to translate – Economists just don’t understand bonds and interest rates, so the public doesn’t either – what are to them mysterious cross-currents slamming the global economy all at the same time.

A few billion in US tariffs on Chinese goods have nothing to do with January 2018.

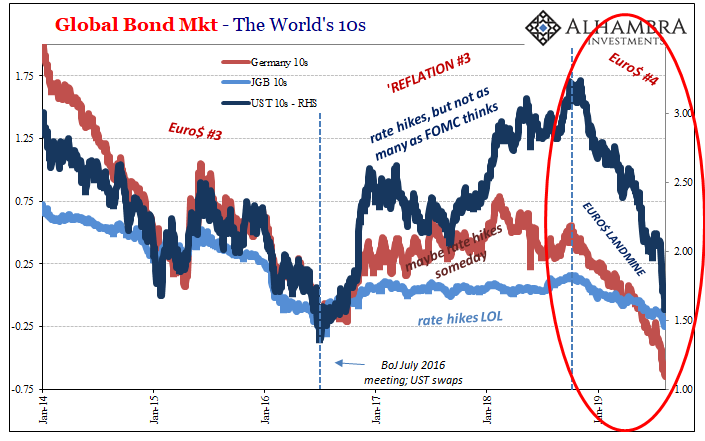

Thus, you can take their projections and assurances about “stimulus” and throw them all in the garbage. The bond market has. From the signals coming from it, I wrote last May, a few days before the 29th, that you could already tell:

…the European economy at the end of January [2018] smacked right into a brick wall of eurodollars. As noted earlier, beginning with the sudden appearance of global liquidations it’s as if Europe’s economy rolled over all at once. Not that it was booming to begin with, meaning that in reality it may be on the wane from a still too-low starting point.

The only question you should be asking yourself today is: if German bonds were and are right about Germany’s and Europe’s economy, then US bonds are…

Stay In Touch