According to the recent release of the Federal Reserve’s projected forecasts, that’s it. It wasn’t one and done like Chairman Powell had initially indicated, this “midcycle adjustment” hits two. And that is it, at least if you believe the current calculations spit out by the Fed’s models.

It goes along with Powell’s blunt statement he made at the press conference on Wednesday broadcasting the second cut. The cut had already been superseded, big time, by events in money markets. Most people still believe that central banks take care of everything money, so to have such a mess show up right then was more than misfortunate from the policy perspective.

Officials are desperately trying to downplay, well, everything; beginning with any risks to the economy. There are none, the FOMC says in word as well as forecast. The economy is really strong and should be able to withstand these whatever cross currents and global headwinds. Out of abundance of caution, one rate cut as insurance. OK, maybe two.

But that’s it. No more will be needed. They are drawing a line in the sand here.

And it’s getting embarrassing, getting pushed back each and every time. Before even getting to repo and fed funds, Powell keeps changing his story. For the record, he keeps changing his story about repo and fed funds, too. We’ll get to that in a minute.

First, you have to keep in mind how this year began. Last year it was all rate hikes, inflation, and boom. Early January, that changed to a Fed “pause” because, it was widely speculated, rate hikes had been the issue creating a little bit of unhelpful, mildly irritating uncertainty. Ending the rate hikes therefore ended the uncertainty.

Except, no, the “pause” didn’t accomplish anything. The negative trends got worse and in response Powell said, OK, but just one rate cut. A single and nothing more. But, just to show you how serious we are, even though nothing’s really wrong, we’ll abruptly end QT, too.

The day after that was announced, August 1, bond prices skyrocketed and yields plunged. In response, there’s now two rate cuts. If it seems like Powell can’t keep his story straight, or that he can’t make up his mind and keeps allowing the bond market to change it for him, that’s because it keeps happening this way.

He’s literally behind the curves.

I mean that in two important ways. Throw out any statements he makes regarding rate cuts. He has no idea today what he will be doing six or twelve weeks from now let alone six or twelve months from now. This isn’t at all unusual, it is the typical pattern. Ben Bernanke suffered the same delusions as did Janet Yellen (especially in 2015).

The issue is funding pressures. It is always funding pressures. In response to the wild ride, the repo rumble this week, Powell flat out denied they were anything serious. He said, “They have no implications for the economy or the stance of monetary policy.”

They already have had far ranging implications for the economy just as they have already erased, written, erased again, and rewritten monetary policy. So, that statement was false the moment it left his lips.

With regard to the near term, FRBNY announced today that it has been directed to keep up these overnight repo operations. Seems inconsistent with Powell’s description of the situation, especially when considering the overnight operations are also to be supplemented by some term repos.

Term repos are the kinds of things a nervous central bank would conduct when concerned about markets being able to overcome the next seasonal bottleneck – quarter end. And these are almost surely the beginning of what will be a standing repo facility or potentially the next QE (as noted months ago, a standing repo facility would be potentially much more than the next QE).

In other words, unless something changed in the day and a half since Powell made his statement these fund pressures have already influenced near-term monetary policy to a substantial degree.

And that isn’t anything new. The whole reason Powell has gone from rate hikes to pause to one cut and no QT to now two and a whole bunch of liquidity operations has been the constant funding pressures that have been perfectly evidence for more than a year and a half. The fact that the Fed has been downplaying and dismissing them the entire time doesn’t mean they didn’t exist or weren’t serious.

It just means, as demonstrated this week, policymakers don’t really understand and appreciate what is going on (which was obvious in how unprepared they were, and how little effect their response created). We’ve been talking about fed funds and the joke (IOER; it’s a joke because time and again it has been proven to be useless) since early on in 2018. Eighteen, not nineteen.

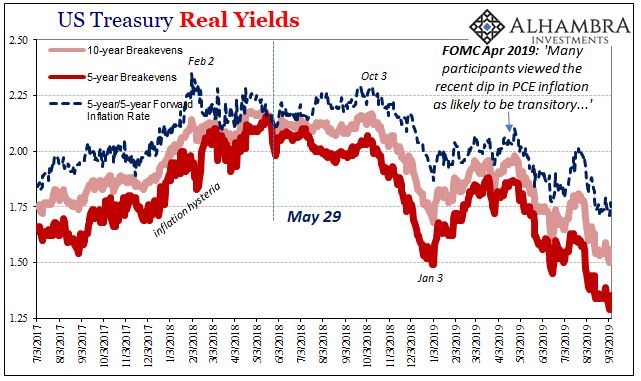

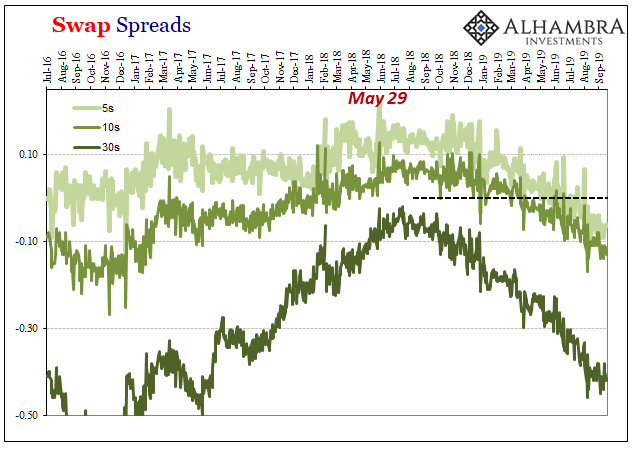

But things really got serious in April and then especially May 29, 2018. Something big broke on May 29, which is why that date features prominently in so many markets, on so many charts. It has proven to have been a definitive inflection. The funding pressures, in that case repo collateral, have only gotten worse since that time.

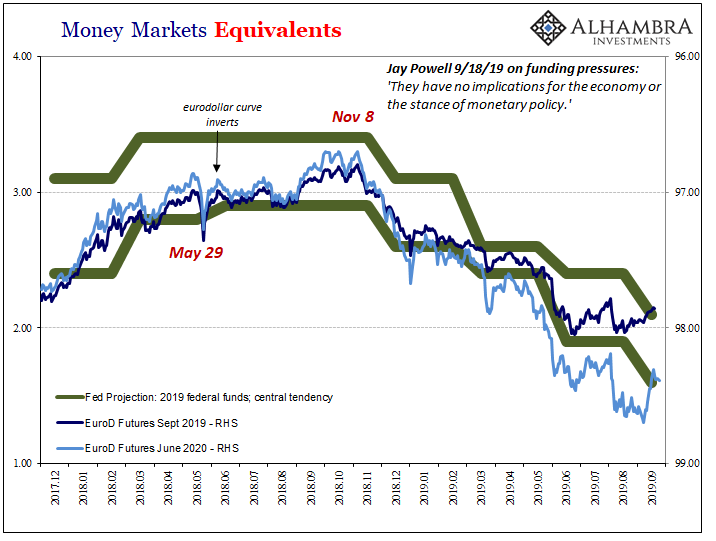

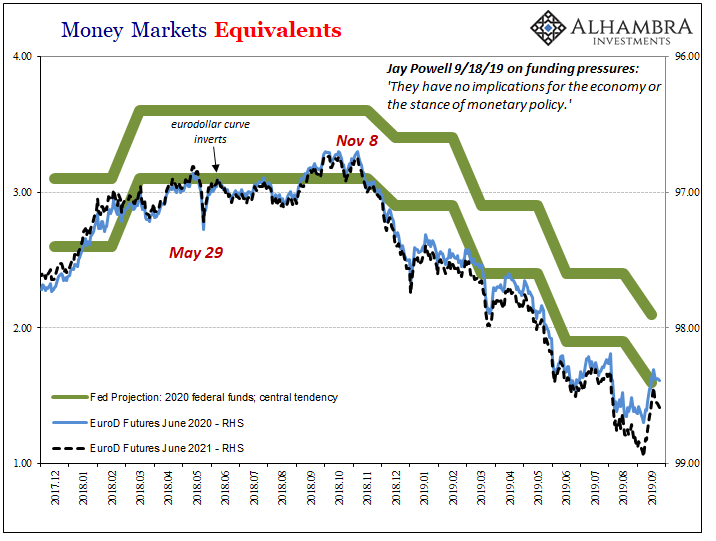

And they have very clearly influenced monetary policy long before getting to this point. Look at how the Fed’s own models closely follow along with eurodollar futures:

It can’t be any more blatant. It doesn’t really matter that eurodollar futures price out expectations for 3-month LIBOR and not federal funds; the two, LIBOR and fed funds, are closely related anyway. It is a bet on what policymakers will actually be doing in the future, not what they believe they should be doing because policymakers have no clue.

Even the models know that they are going to end up following the market. And the market has been pricing funding pressures ever since May 29. It is not coincidence how the eurodollar curve inverted just two weeks later – and on the very day in June 2018 when, of course, the FOMC moved IOER (technical adjustment) for the first time.

It was the market picking up the seriousness of May 29 as well as the un-seriousness of policymakers in responding to it; even though those same funding pressures had been building up in repo and fed funds beforehand, too.

Jay Powell and his gang are not serious people. He says funding pressures don’t matter, not to the economy and certainly not to monetary policy. He expects that you are too stupid to understand they already have mattered and in every way possible – from derailing that epic boom and inflationary breakout long before the end of 2018 to bringing two rate cuts and counting, ending QT long before it was scheduled to end, and now a pathway toward more permanent (and ultimately futile) reserve operations.

It sure sounds like a whole bunch has been changed about every part of the situation.

And despite all that, the questions and concerns about a potential US (dissenter James Bullard) and global recession have only grown louder. That’s maybe the real bad news of fed funds blowing up this week; he won’t be able to blame it on “trade wars.”

They really, really have no idea what they are doing. That’s true always, but there are times when it really shows. This week was definitely one of those times. It will not be the last for 2019. Don’t take my word for it, certainly don’t take Powell’s word on anything. The bond market had it clocked from the very start.

Stay In Touch