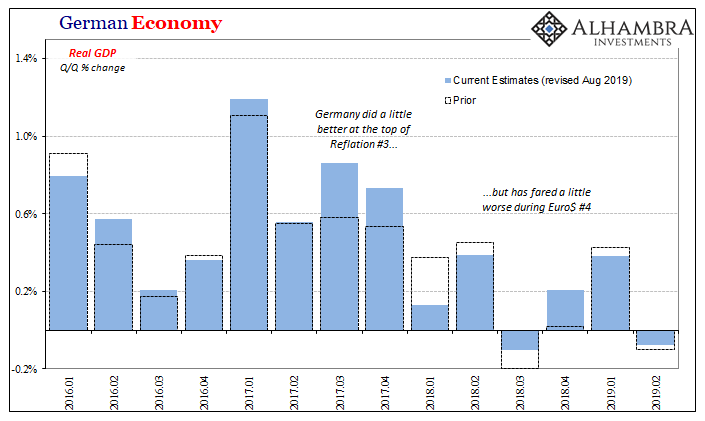

Yesterday, Eurostat confirmed that German GDP in Q2 2019 had contracted. Also issuing benchmark revisions, the European government agency found that GDP growth had been slightly better than previously thought at the top of Reflation #3. The last two quarters of 2017 saw the biggest upward revisions.

But if Europe’s “boom” really was a little closer to having been a real one, all that does is magnify the disappointment which has followed. Why didn’t it keep going? Eurostat’s newest benchmark series puts the German economy a little worse during Euro$ #4. Apart from Q4 2018, GDP growth was marked downward in the other quarters particularly for the clear transition into the first quarter of last year.

In other words, the change from reflation to renewed global monetary squeeze was even more abrupt than we had thought – at least going by GDP. However, this merely brings the broad economic accounts in line with market behavior. From the very beginning of 2018, you could tell something meaningful had changed. Government statisticians are only trying hard to catch up.

While this may be an academic exercise for those statisticians it remains a relevant topic for current discussion and analysis. Though we are conditioned to believe an economic contraction is a quick event which shows up “unexpectedly”, this couldn’t be further from the truth.

Germany’s economy as the whole global economy was hit with a shock more than a year and a half ago. Not trade wars, a eurodollar monetary shock. All the while in 2018 as European officials were giddy about their boom, they hadn’t realized it had already ended at the close of the prior year. That’s why in 2019 weakness in the public eye seems rapid and unforeseen.

Stop listening to central bankers and Economists. They really have no idea what they are doing.

And that’s just the beginning – literally. It’s hard to imagine more than eighteen months of lingering weakness as only the prelude. We are also led to believe that an economy either is in full and outright recession, or that it grows, expands, and booms. It’s not supposed to exist in something like a state of limbo, as if some wounded animal cruelly awaiting its fate.

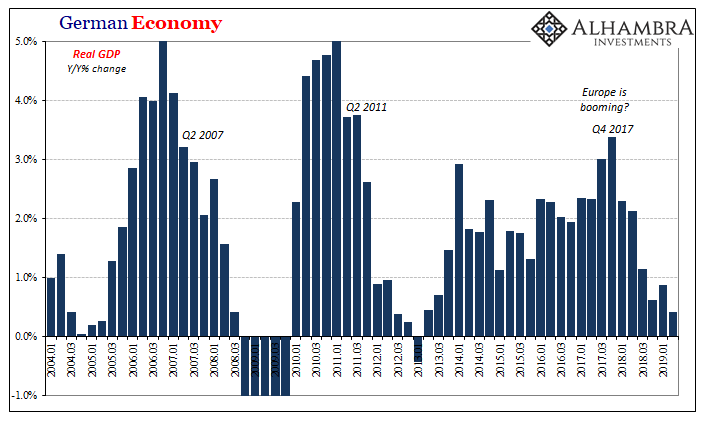

Yet, all the indications point to much more to come for Germany. There was some growth in 2017 during Reflation #3, but then when the calendar turned to 2018, and the eurodollar system reasserted its baseline (deflation), that was no longer the case. It wasn’t recession which took over from there, rather a sort of transitional state displaying a curious lack of either sustained growth or contraction.

That’s a lengthy pause for what are only now being called “transitory” factors, headwinds, and cross currents. From the conventional point of view, it may seem like the longer this drags on the better the likely outcome. A weird sort of impatience has arisen whereby if a full-scale contraction doesn’t take place by tomorrow some commentators and policymakers have convinced themselves there won’t be one.

It’s entirely the other way around; the longer an economy remains in limbo the greater the probability it doesn’t get out of it unscathed.

That’s especially true given the nature of the shock which is being slowly transmitted into and throughout the global system. This is one reason why I call them eurodollar squeezes. The word “shock” delivers sometimes the wrong connotations; an immediate event like an explosion from which the full extent of the damage is instantly apparent.

These eurodollar squeezes, however, are like a constrictor deliberately squeezing the life out of otherwise alive prey. The “shock” is the first bite when the serpent grabs hold. Once it does, unless the prospective meal breaks free relatively quickly its chances for survival get darker and darker as time passes.

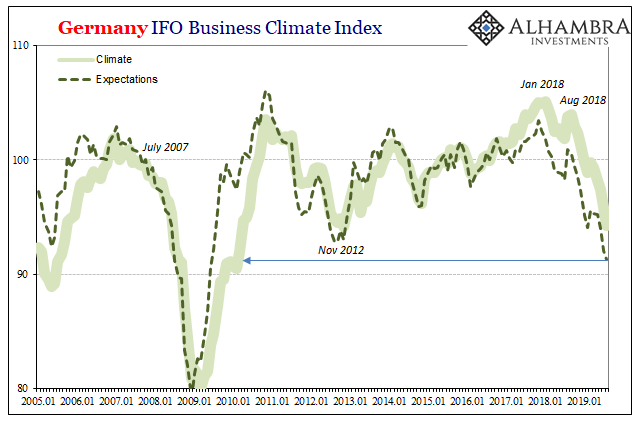

Data keeps showing up which suggests that for the German economy the point of no return is either close at hand or has already been surpassed. More and more it looks like the best case is something like the milder 2012 recession, which was mild only in comparison to the Great “Recession” that had preceded.

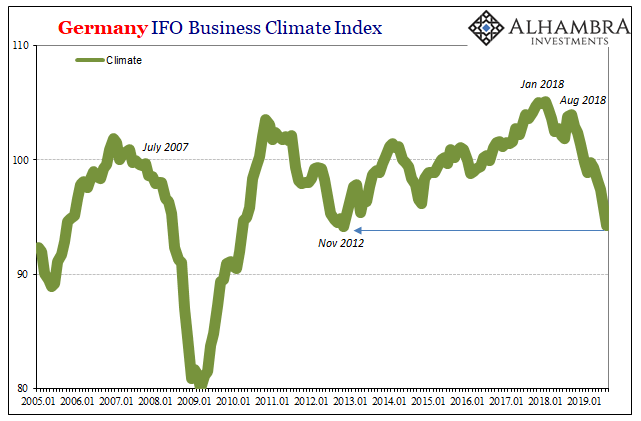

The latest estimate for August 2019 from Germany’s closely-watched IFO institute, like the ZEW it puts the current business climate already equal to the depths of that previous recession. Part of the reason is how the downturn is no longer limited to trade and manufacturing – the point of fracture introduced by the eurodollar shock way back at the end of 2017. The lack of monetary oxygen from the ongoing squeeze has penetrated the full economy.

This is very bad news indeed. It’s not just manufacturing where the decline continues, but we now see that the weakness is really affecting the services sector which is large and important for the German economy.

That was professor Clemens Fuest, head of the IFO, telling CNBC about the seriousness of Germany’s situation. Perhaps the more important piece of his organization’s data release was the expectations component. For the month of August, it was more Great “Recession” than 2012 recession.

What’s indicated here is exactly what I’ve described. The shock and economic transition took place when the dollar turned (the relevant flipside to our key formulation, CNY DOWN = BAD), and even though that was a long time in the past and the German (global) economy has been struggling for more than a year and a half already, it is still quite possible and even likely this has only been the beginning stage(s). More and more likely, in fact, with each passing month.

And while we pity the poor Germans that doesn’t mean we aren’t selfishly looking on with increasing alarm. As more and more economies around the world behave in the same way and with the same indications, big ones, too, like Japan and China, it suggests that Germany is no global outlier – it is merely the farthest down the road and therefore a potential glimpse at our intermediate future.

The further they slip downward, the greater our own potential downside.

You can, I hope, see right what it is that might be so spooking the global bond market (and gold) at the moment, at least from the econ side of things (there are other purely monetary considerations which bond yields are reflecting, too). Against all this, Jay Powell’s single rate cut, the ECB’s coming “stimulus”, and Janet Yellen’s childish term premiums all look pretty ridiculous by comparison.

The shock and the squeeze, they are old news. All that’s left is the last one.

Stay In Touch