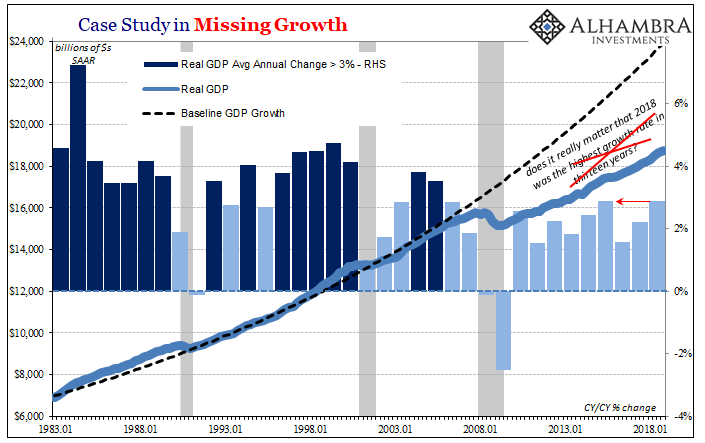

The BEA has completed its unscheduled departure from its release schedule. Due to the prior federal government shutdown, the government agency was only able to put together two estimates for Q4 2018 real GDP. The first had seemed to calm some fears that US growth was wobbly toward the end of last year, aligning uncomfortably with what we are more and more finding “overseas.” Coming in originally at 2.55617%, it was enough to disappoint both sides of the divide, neither confirming nor denying anything.

The final revision places fourth quarter growth at 2.14336% instead. It really isn’t a meaningful downgrade, but it is just enough to deprive 2018 of its presumed crown; last year can no longer be claimed to be the best one in more than a decade. Three years ago, 2015, continues to hold that distinction in the wake of the BEA’s new figure.

Of course, as noted last month, that isn’t a meaningful one, either. What we find, quite clearly, is an economic system which remains grounded in its same rut. This is not what Jay Powell has been talking about, nor is it what the White House has continued to claim so far into 2019:

Collectively, the 10 chapters that constitute this Report demonstrate that the strong economic performance in 2017 and 2018 constituted a sharp break from the previous pace of economic and employment growth since the start of the present expansion, reflecting the Administration’s reprioritization of economic efficiency and growth over alternative policy aspirations that subordinated growth. [emphasis added]

To be fair, the prior administration claimed the same thing in 2015; only to be similarly disappointed.

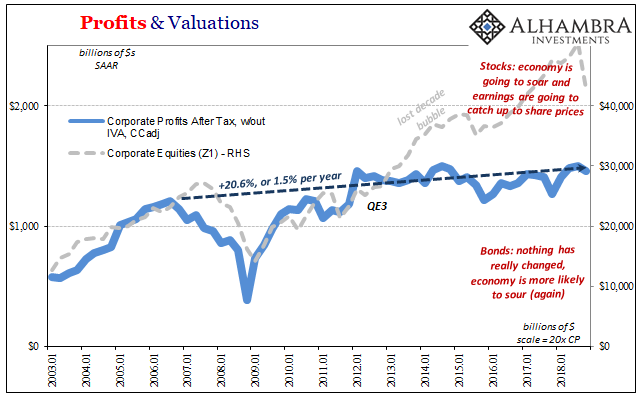

The idea of an economic breakout, however, is meaningful. And it defines practically everything we see. Political lines are drawn around it, as well as market dichotomies where investors fall into largely two camps: those who believe we’ve witnessed, or will soon witness, this “sharp break from the previous pace of economic and employment growth” and those who see how nothing has really changed.

This cuts across those markets, too. In the stock market, the majority opinion, what has driven share prices, is agreement with Trump’s assessment. Particularly in relation to tax reform and deregulation (Obamacare mandate), the ingredients have been put in place to accomplish what we all are seeking.

There’s the same idea in bonds, only it hasn’t been made nearly as convincing to the major players there. We hear, or heard, all the time about the end of the 30-year bond bull market. What will kill that “bull” is exactly this categorical change. If growth has indeed reached a new sustainable paradigm for the first time in a very, very long time, there won’t be a bond rout it will be a massacre that puts 1994 to shame.

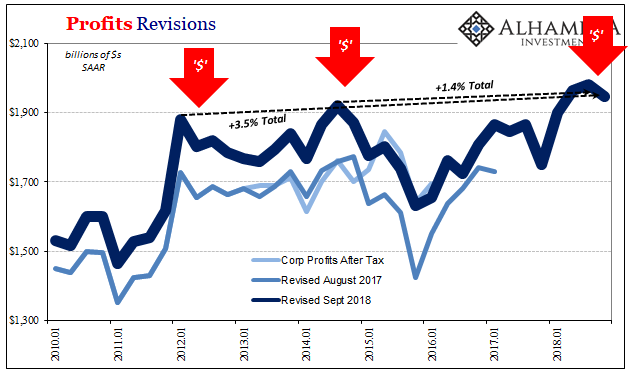

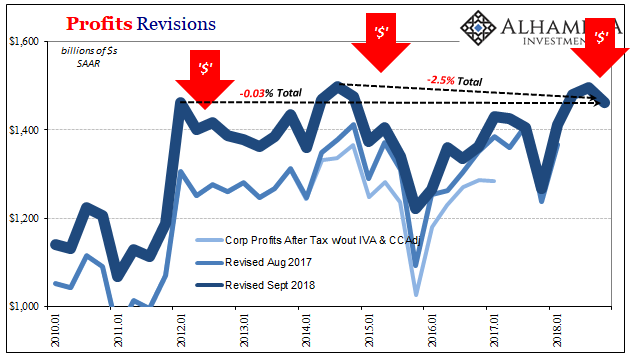

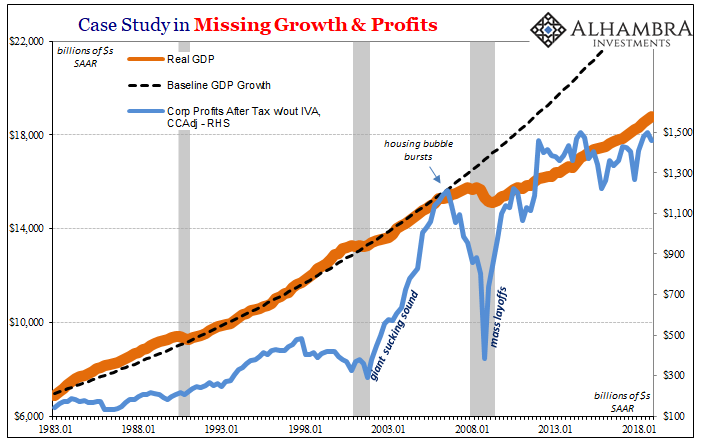

Where it all comes down is corporate profits. These are at the center of everything, economy to markets, both stocks and bonds. The final GDP estimate includes the first figures on economy-wide bottom lines. For yet another quarter, the bond side continues to be most consistent with the evidence.

There is just no profit growth evident anywhere. Even after the corporate recession of 2015-16, net incomes didn’t rebound nearly the way it had been anticipated. Profits across-the-board were not suppose to merely equal the prior 2014 peak and then stall, as they have, it was supposed to be better than a V-shape with 2016 as the ultimate trough.

This up down, up down, up down simply adds up to nowhere; a stretch of time which now stretches back an astounding seven years. It’s a sufficient sample size to reasonably conclude, as bond markets here and around the world have, that if it was going to happen it surely would’ve happened by now; QE’s, tax cuts, ARRA’s, whatever. It seems like “something” else is still holding back economic growth.

The bigger problem is this looming US participation in Euro$ #4. Profits were down in all categories in Q4, though not substantially. Still, it adds weight to the idea that there is limited upside, as shown these last seven years, and more than a little re-emerging downside for the so-called supply side of the economy.

It is, I believe, one key reason why, along with liquidation pressures, stocks fell sharply during that very quarter. Which position, stocks or bonds, became more likely? Is there now a better probability that corporate profits soar with the economy and therefore vindicate sky high share prices? Or is it the other way, where the economy falls flat (or worse) yet again leaving stock markets vulnerable from underneath?

The current data on Q4 leaves us with only the impression that nothing has changed – so far – the same feeling which became a lot more popular as uncertainty built to the end of last year. It has only grown more so this year as evidence stacks up on the negative side.

Stock investors are certainly still holding out hope that this economic therefore profit breakout is still coming, maybe full recovery is, yet again, just delayed. Forget about rate cuts as stimulus or anything like that. In the context of this diverging view, which position is solidified by central banks throwing in the towel and then reversing course as bond markets now project?

This is the question that will eventually perplex most people in 2019, once the implications are more readily appreciated as the warm glow of dovishness is recognized as something very different.

Stay In Touch