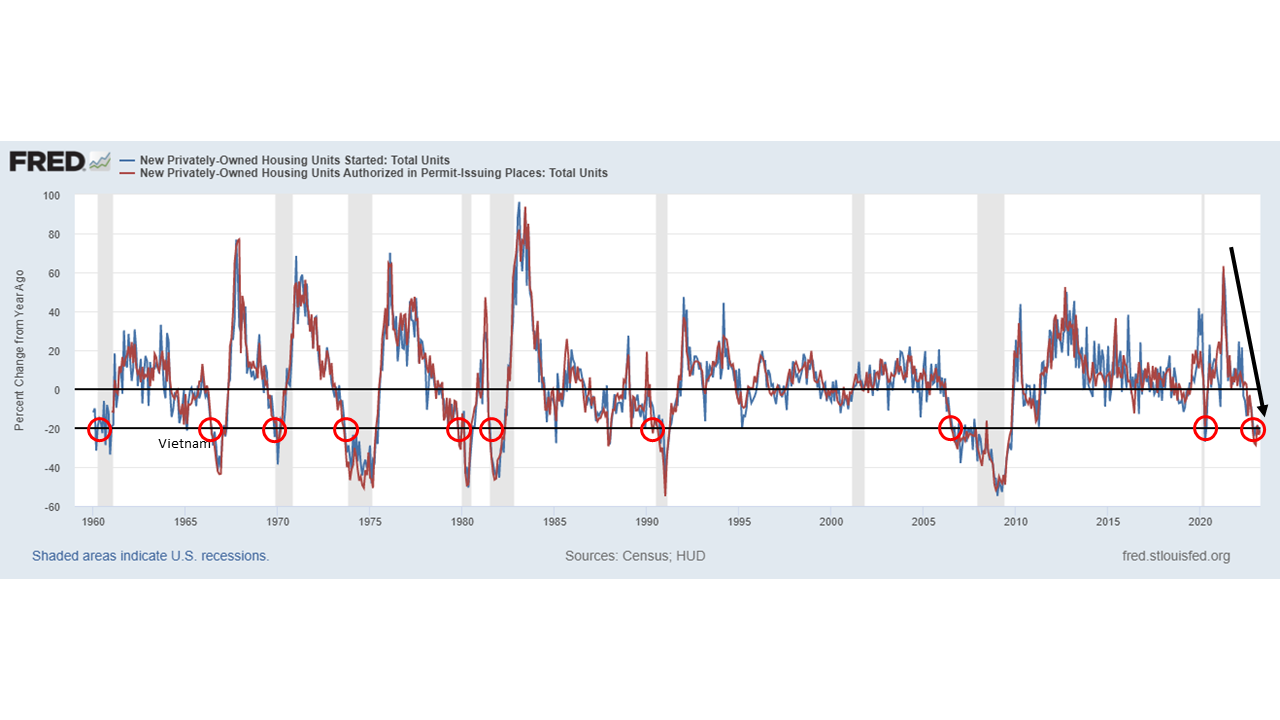

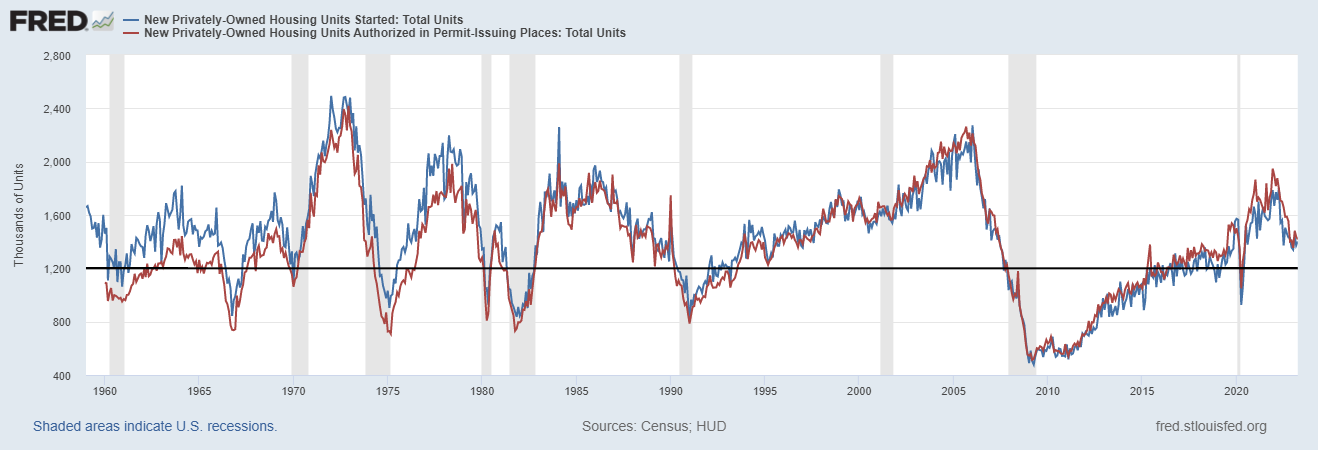

Housing starts and permits for April are running at a level of right around 1.4M units down from around 1.8M last year. That’s a drop of 22% in starts and 21% in permits. 1.4M units is roughly in line with the long term average. The level of starts and permits is not yet concerning, but the slow down continues to be worrisome.

For housing starts, the surge in building during the pandemic started to abate around April 2022 so the year ago comps start to get easier. For next month’s release, I would expect the annual growth number to be much better than -22%, a wide back of the envelope forecast would be for -7% to -13%. Should annual growth in housing starts fall again by 20% May 2022 to May 2023, that would put us around 1.2M units which has been a recessionary level in prior cycles. So the sequential number for May will be the one to watch next month, flat sequentially would be a good start.

As for permits, the data diverges a bit starting in May 2022. Permitting continued to run at a higher rate through August 2022. This is likely because of delays or backlogs in the permit process from the pandemic restrictions. We’ll just call it building permit supply chain disruptions. The annual drop in permits is expected to remain higher than starts. The annual growth rate shouldn’t be less than -20%, but somewhere around -16% to -18% is in the ballpark.

Stay In Touch