So we’ve never had people in a more gambling mood than now. But that doesn’t mean that investing is terrible. It does mean that prices for an awful lot of things will look very silly.

Warren Buffett, CNBC interview, 5/2/26

If you’ve been reading these weekly missives for any length of time, you know I’ve been ranting about gambling for quite a while now. The gamification of the markets started, in my opinion, with the founding of Robinhood, by two guys who got their start building high frequency trading platforms for hedge funds. They founded Robinhood in 2013 to “democratize finance for all”. Or at least that’s what they told everyone, but from the beginning the app’s design mimicked social media and gambling to keep its customers (marks?) trading. The first clue is that it is “free”, which is only true in the sense that you don’t pay a direct fee to trade.

One of my favorite economics acronyms is TANSTAAFL (there ain’t no such thing as a free lunch). In the case of Robinhood – and almost all brokerage firms today – your lunch is paid for by “payment for order flow”. That’s how Robinhood and most of the other brokerage firms get paid today. Robinhood gets paid to send your orders to Citadel Securities (or some other market maker; Citadel is just the biggest), not because that’s where you get the best price but because the market makers are paying them to do so. Citadel wouldn’t do that unless they were able to take those orders and make more money than they could without them. There’s a reason Ken Griffin owns multiple $100 million plus residences.

Robinhood, from the beginning, had that casino feel to it. When you did your first trade on the platform, the app screen would shower the user with a colorful confetti animation (that was too much for regulators and has been discontinued). That was your first clue that this wasn’t your father’s customer’s man but they went further, offering “rewards” for referring your friends to the app. They were also the first to send push notifications about market events, looking to stoke your FOMO (fear of missing out) and the app itself was designed to feel more like a dating app than an investing tool. You swipe up to submit an order because, I guess, they didn’t want to give you the option of swiping left and rejecting a trade. It seems almost quaint to think of markets as efficient allocators of capital when the most successful innovations in recent times is an app using every trick from the social media playbook to keep you trading and zero days to expiration options (of which Buffett said, “That’s not investing. It’s not speculating. It’s gambling, just totally.”).

What is more disturbing, I think, is that the economy itself has now been infected with this gambling fever. We got a report last week on Q1 economic growth which was – quelle surprise – exactly 2%. That’s what I’ve been telling you to expect because the trend hasn’t budged since about 2010, the economy growing at average annual rate of 2.2%. If you just look at the headline number, this report looks unremarkable but the composition of GDP in this report is disturbing and emblematic of the pervasive nature of gambling in our society today. We all know the AI hyperscalers have been increasing their capex, and earnings reports last week from Google, Amazon, Meta, and Microsoft confirmed the huge bet these companies are making on AI. They expect their capex to rise by 77% over the next year to over $700 billion, the vast majority of that to build out AI infrastructure. AI spending in Q1 was responsible for about 3/4 of the total change in GDP: Spending on information processing equipment accounted for 0.83% of the 2% annualized GDP growth while intellectual property products (software, R&D) accounted for 0.7% of the total. Since the beginning of 2025, AI spending has accounted for about 45% of GDP growth – and now it is accelerating.

That doesn’t necessarily mean that absent AI spending the economy would have grown only 0.5% because we don’t know what would have happened without the AI spending. But we do know that a lot of the money being spent on AI isn’t staying in the US because much of the equipment is imported – tariff free I might add. Nevertheless, supply/demand dynamics are very much evident in this GDP report. Prices for computers and peripheral equipment rose at an 18.5% annual rate in Q1 while R&D prices rose 5.5%. We see a different impact on software prices which fell at an 11.7% annual rate in the quarter. Software companies are cutting prices because AI is, potentially, a direct competitor. Frankly I don’t think most software companies have anything to worry about. The price of AI is artificially low right now as companies train their systems on your prompts. But once that is done – and we’re rapidly approaching that point – prices will rise and probably not by a little.

I do wonder though how the economy would be doing without the AI spending. Some other reports last week are cause for concern. Personal income and spending looked great on the surface with income up 0.6% (double expectations) and spending up 0.9%. Unfortunately, a lot of each of those numbers was nothing more than inflation. Real disposable personal income (after taxes and inflation) was actually down 0.1% and is up a mere 0.4% over the last year. Real personal consumption was up just 0.2% and 2.1% over the last year. Is it any wonder that the savings rate has fallen from 5.1% a year ago to 3.6% today?

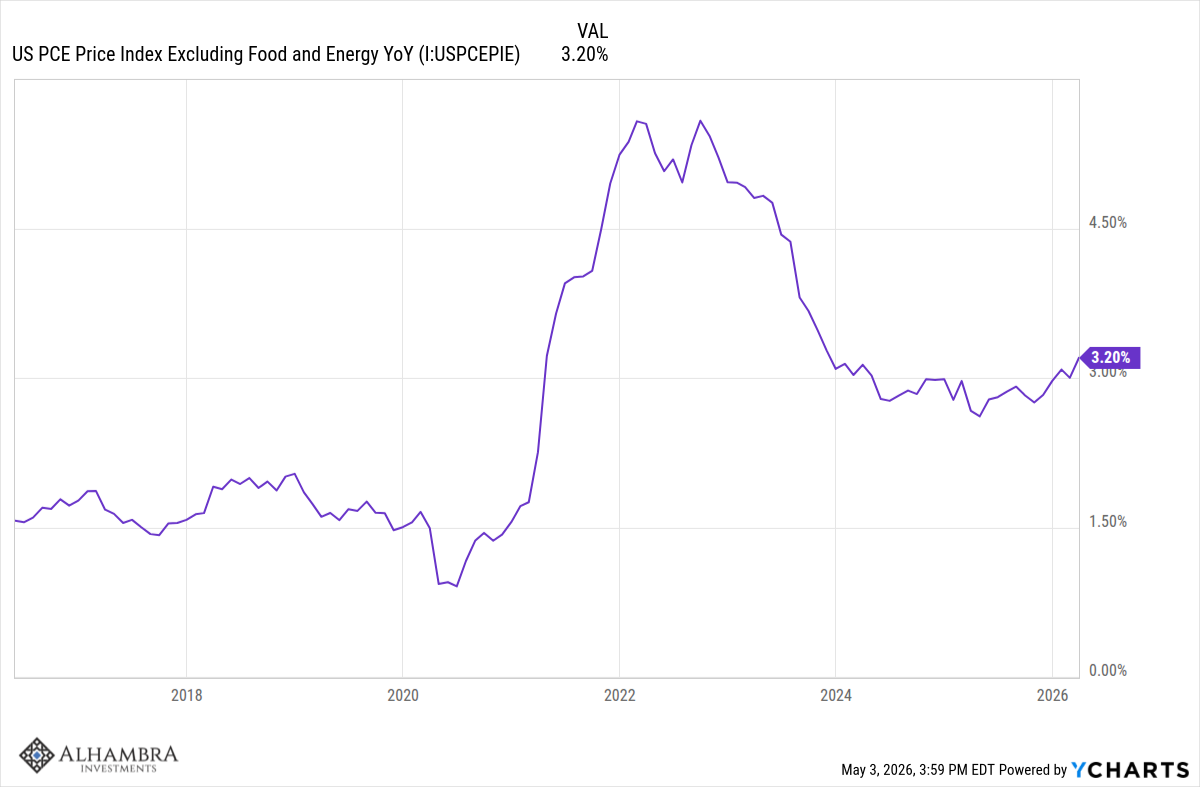

The PCE price index was up 0.7% in March and 3.5% year-over-year. The core reading – which is what the Fed is watching – was up 0.3% for the month and 3.2% over the last year. A year ago, the year-over-year change was 2.6%; inflation is accelerating. I’m sure it’s just coincidence that it started to rise again in April of last year when President Trump announced his “reciprocal” tariffs.

All this AI spending amounts to a giant bet on future growth from the AI productivity increase everyone assumes will materialize any minute now. And it better because I think investors are starting to get impatient with the big spenders. Of the big AI hyperscalers (Google, Meta, Amazon and Microsoft) that reported last week, the biggest winner was Google, which was the only one of the four to report any kind of positive impact on earnings from AI. At Meta, which reported spending a lot of ad dollars with no positive impact on the top or bottom line, I suspect investors are starting to feel a bit of deja vu. Zuckerberg spent billions on the metaverse and all shareholders got was a new company name that looks even more ridiculous today than it did when it was announced.

Even at Google, the supposed big winner, earnings were goosed by a mark up in the value of their private equity holdings. What might those be? How about a 15% stake in Anthropic “worth” about $160 billion and a roughly $100 billion stake in SpaceX? Earnings including those markups totaled $62.6 billion; without them $28.7 billion. That’s still a nice pile and a growth rate of 20% is hard to find in a company the size of Google but why do you think they decided to mark those holdings up now?

This earnings sleight of hand is impacting S&P 500 earnings in a big way. The earnings growth rate for the S&P 500 rose from 15% to 27.1% last week. 71% of the dollar level increase in earnings came from just 3 companies: Alphabet, Amazon, and Meta. The blended earnings growth rate of the Magnificent 7 stocks rose to 61% from 22.4% at the end of March. The big drivers of stock prices are earnings growth and interest rates. With interest rates quiescent for the last three years, earnings have the conn and in the S&P 500 that means AI is steering the ship. The S&P 500 now is so concentrated in technology and technology-adjacent stocks (Google and Meta are the two biggest allocations in the Communications sector) that one sector is now 44.3% of the fund. The index funds may still meet the criteria to be called “diversified” but if you’ve been consistently buying “the market” in your 401k for years, you’ve built up a big bet on AI. By the way, if you think you get more diversification by switching to a fund like Vanguard’s Total Stock Market index, you do but it only reduces the concentration to 38.3%.

The rules for the S&P 500 didn’t change for a long time. Once, inclusion just required that the company be “big”; however that was defined over the years. But since 2000, there have been multiple changes; some good, some bad. In 2004, in the wake of the dot com bust, a profitability requirement was added (positive) and in 2017 companies with multiple share classes were disallowed for new entry (positive) but that was repealed in 2023 (negative) because it excluded too many tech stocks. Now, S&P is looking at making more changes by allowing inclusion in the index 6 months post-IPO rather than the previous 12 months and repealing the profitability requirement. Why? Have you heard that SpaceX, Anthropic, and OpenAI would like to go public soon? I’m sure that has nothing to do with these rule changes. S&P hasn’t approved the changes yet so maybe their FOMO will fade before these companies manage to IPO but NASDAQ is in full froth. They changed their rules last week so companies only need to be public for 15 days before becoming eligible for inclusion. I don’t think John Bogle would approve.

I’ve never liked the term bubble because there really isn’t a definition; bubbles are very much in the eye of the beholder. But I’ve seen a few booms and busts across the four decades I’ve been at this game and AI is certainly in a boom phase. Whether or when it turns to bust, I don’t know but I would just warn that it doesn’t have to be something directly related to AI that brings these stocks back to earth. Remember, as I said above, stock prices move on earnings growth and interest rates. The former are doing well right now, even absent the tricks used to boost earnings from last quarter (although that isn’t generally a good sign) so everyone watching earnings feels pretty good right now. Me? I’m watching the other part of that equation – interest rates.

Almost four years ago, I wrote a long form article called Dawn of a New Era (which you can download here) which laid out my view that the future would be more inflationary. The thesis is based on demographics (labor shortages), deglobalization (diversifying supply chains away from China), industrial policy (more government involvement in the economy), and reckless fiscal policy. It wasn’t perfectly prescient but the general thesis holds up quite well, if I do say so myself. Part of that thesis was that the inflationary episode we were in at that time (2022) would be contained but it would not be the last one. With inflation turning back higher over the last year, it may be that the second wave is upon us. If that is right, interest rates may be headed higher.

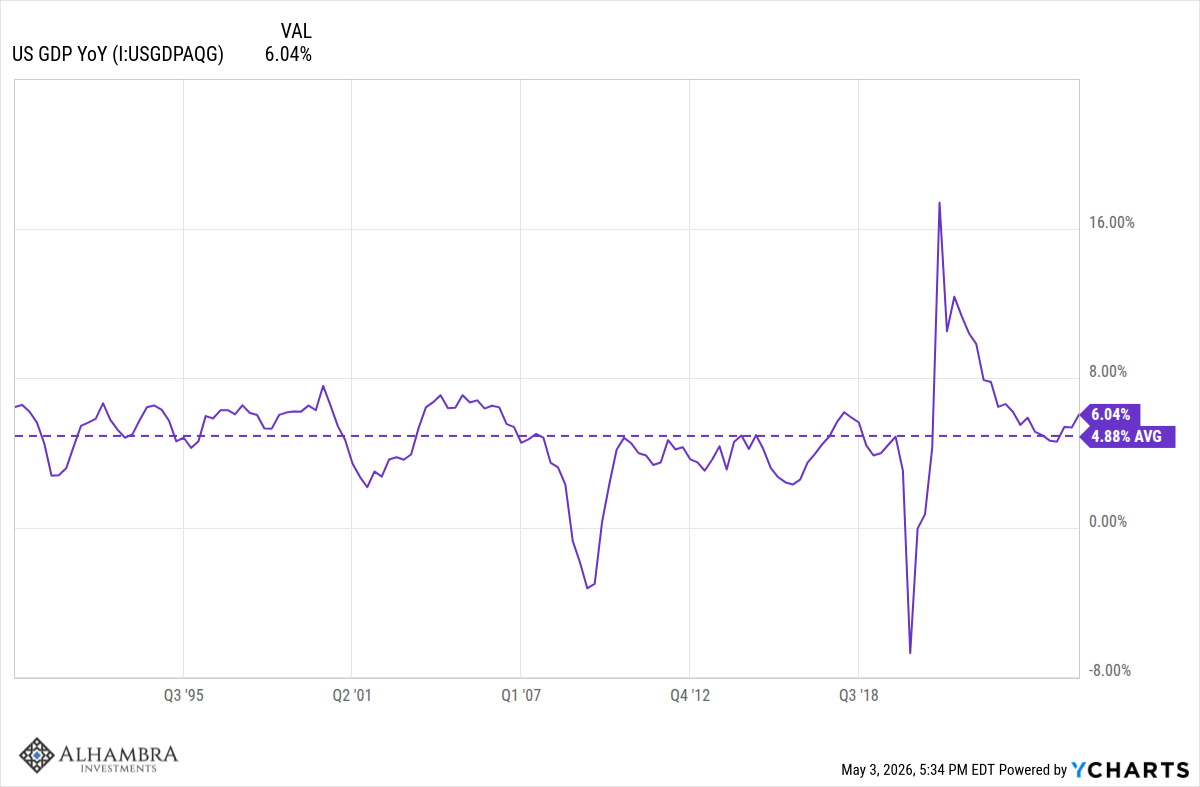

When the GDP report was released last week, all the attention was on the inflation-adjusted version, real GDP. But the real news was actually in the non-inflation adjusted number, nominal GDP. As I’ve written many times, the Fed really only affects nominal variables and that includes NGDP. The year-over-year change in NGDP released last week was 6.04%, up from 4.65% in Q1 last year. That acceleration is partly due to a slight rise in real growth but mostly about inflation. Since NGDP and the 10-year Treasury note yield converge over time, the rise in NGDP is not, in my opinion, good news for stock investors. I’m sure we all remember 2022 and what rising rates do to stock prices, even those of innovative tech companies.

Everyone knows that earnings for the S&P 500 are great right now which means it is largely priced in. And the consensus right now is that there will be no more rate cuts by the Fed this year. Indeed, the odds of a rate hike by next March are higher than for a rate cut. It wasn’t that long ago the market was expecting multiple rate cuts this year but now, despite the President getting his preferred Fed Chairman, the market expects none. That’s how much expectations have shifted over the last 6 months. Will we start to see rate hikes priced in? If so, that probably isn’t going to be good news for the market gamblers who seem to think no price is too high for anything AI-related.

Joe Calhoun

Stay In Touch