All About The AI?

It’s an AI stock world and all the other stocks are just living in it, right? That is the persistent narrative we’ve been hearing for at least a couple of years and while the story is starting to see some cracks, it is still widely believed. There is still an underlying whiff of FOMO surrounding the AI and AI adjacent stocks. Is the narrative right? That is a more difficult question to answer than it first appears. If we look at some recent stock market returns, the answer, at first, seems to be no. Small cap, midcap, international and value stocks are outperforming now while the big growth stocks take a breather. Certainly the AI stocks are perceived as large cap US growth stocks so if small, value and international are starting to outperform that would seem to be good evidence that the AI boom is coming off the boil.

But is it really that simple? It sure seems like good news if the market has broadened out and other types of stocks are performing well. Diversification has been a tough gig the last 5 years so seeing other asset classes – other than gold – start to perform well is a welcome sight. Within the equity market there are positive signs that we aren’t just dependent on a small group of stocks for performance. Since May 18th the S&P 500 is down slightly (-0.5%) but the percentage of S&P 500 stocks above their 50 day moving averages has risen from 48% to 65%; the percent over their 200 day MA has risen from 55% to 65%. This broadening out is also seen in the S&P 500 dispersion index, up from 27 at the end of last year to 42.5 today. Even as the large tech stocks have faltered some, other stocks within the S&P have picked up.

The earnings outlook has improved too and while tech stocks are a big part of that, it is the energy sector leading the upward revisions so far this year. That would seem to be related to the Iran War and maybe it is but with oil prices back down to pre-war levels, estimates have not retraced. By the way, the crude oil futures market remains in backwardation despite the (possible) unclogging of the strait of Hormuz. There is a persistent group of permabears out there who seem desperate to paint the oil market as on the edge of disaster. I saw several references last week to the crude market shifting to contango – with spot prices cheaper than prices a few months out, an indication of an oversupplied market – but if it did, it didn’t last long. I must have been busy with something else that hour. I always find it odd when people want to argue with the market when those who do almost always end up losing.

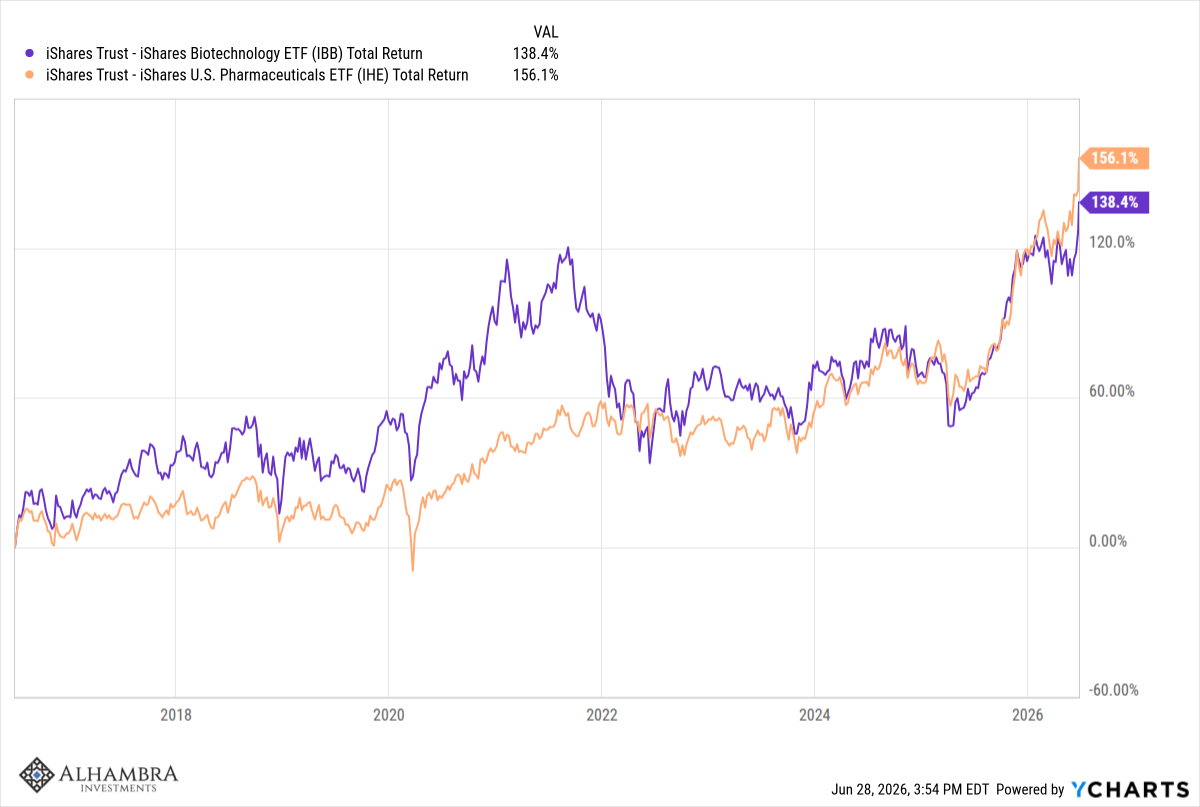

The rise in earnings estimates isn’t exactly widespread though it does seem to be improving. In addition to tech and energy, estimates for the materials, communication services and financials have also risen. Industrials, health care and consumer staples have fallen. It is important to look forward though which is what markets do so well. While estimates for the healthcare sector as a whole are still falling, biotech and pharmaceutical stocks are breaking out to new highs. Biotech earnings estimates are rising (up 12%) but pharma stocks are still seeing negative revisions. But with the big pharma companies trying to plug a patent expiration hole with biotech acquisitions, the market seems to be betting that expectations will start rising again.

International indexes are also still performing well although the degree of outperformance has recently faded some as the dollar has rallied. Still, the fact that non-US stocks are performing well is good news for diversified portfolios. There isn’t nearly as much exposure to technology outside the US so just keeping pace with the US markets is a feat.

So, yes, there does seem to be some good news out there compared to the narrow performance we’ve seen over the last few years. It isn’t just the Mag 7 or the S&P 500 top 10 or tech that is doing well. But, if you know me, you know I’m not comfortable just taking things at face value. And when we look under the hood of some of these indexes, what we find is….the market is broadening out because the AI boom is spreading beyond the big tech companies.

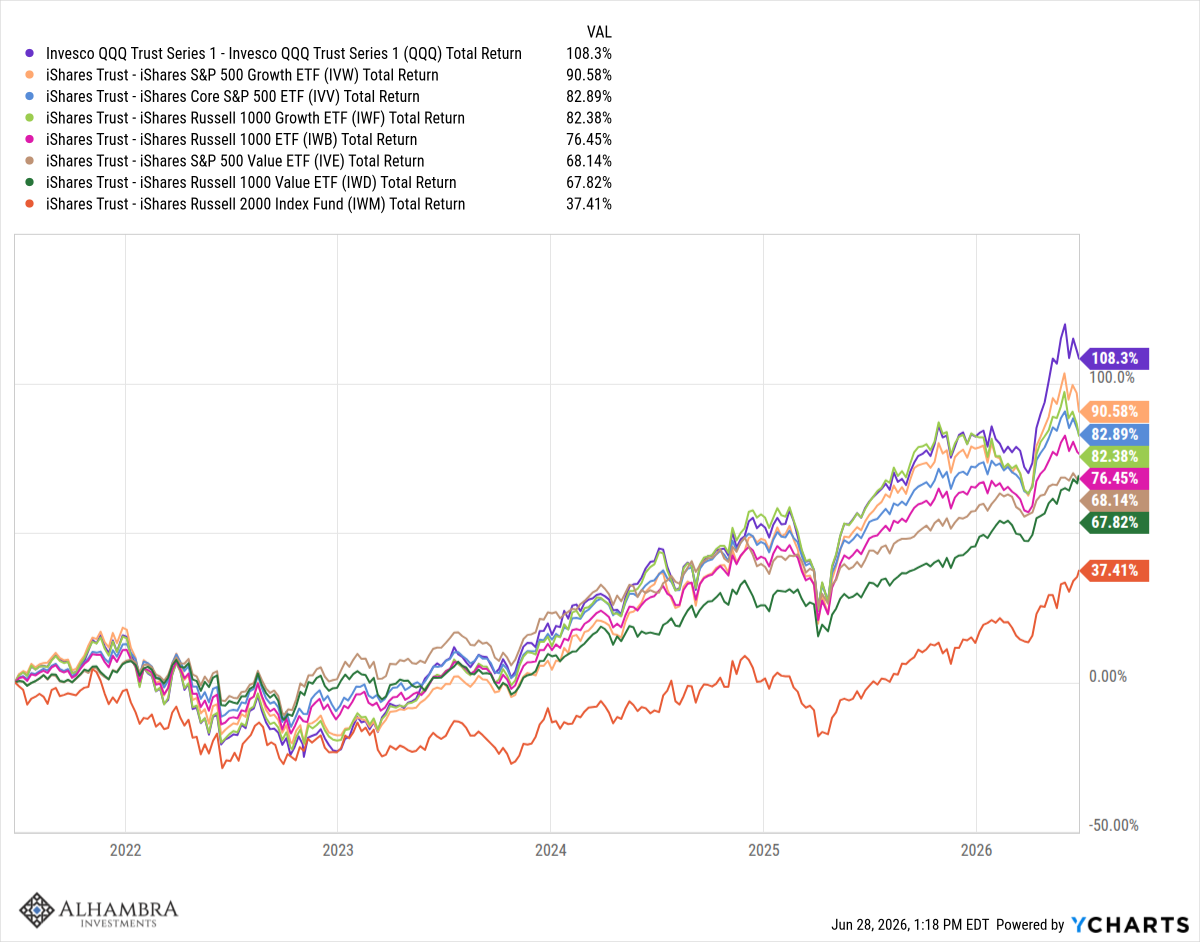

If you look at the returns of the NASDAQ 100, the Russell 1000 growth index and the S&P 500 growth index over the last 3, 5 or 10 years, it is these large cap growth indexes that have outperformed. They dominate the top of the performance list over the last 5 years while value and small caps are at the bottom.

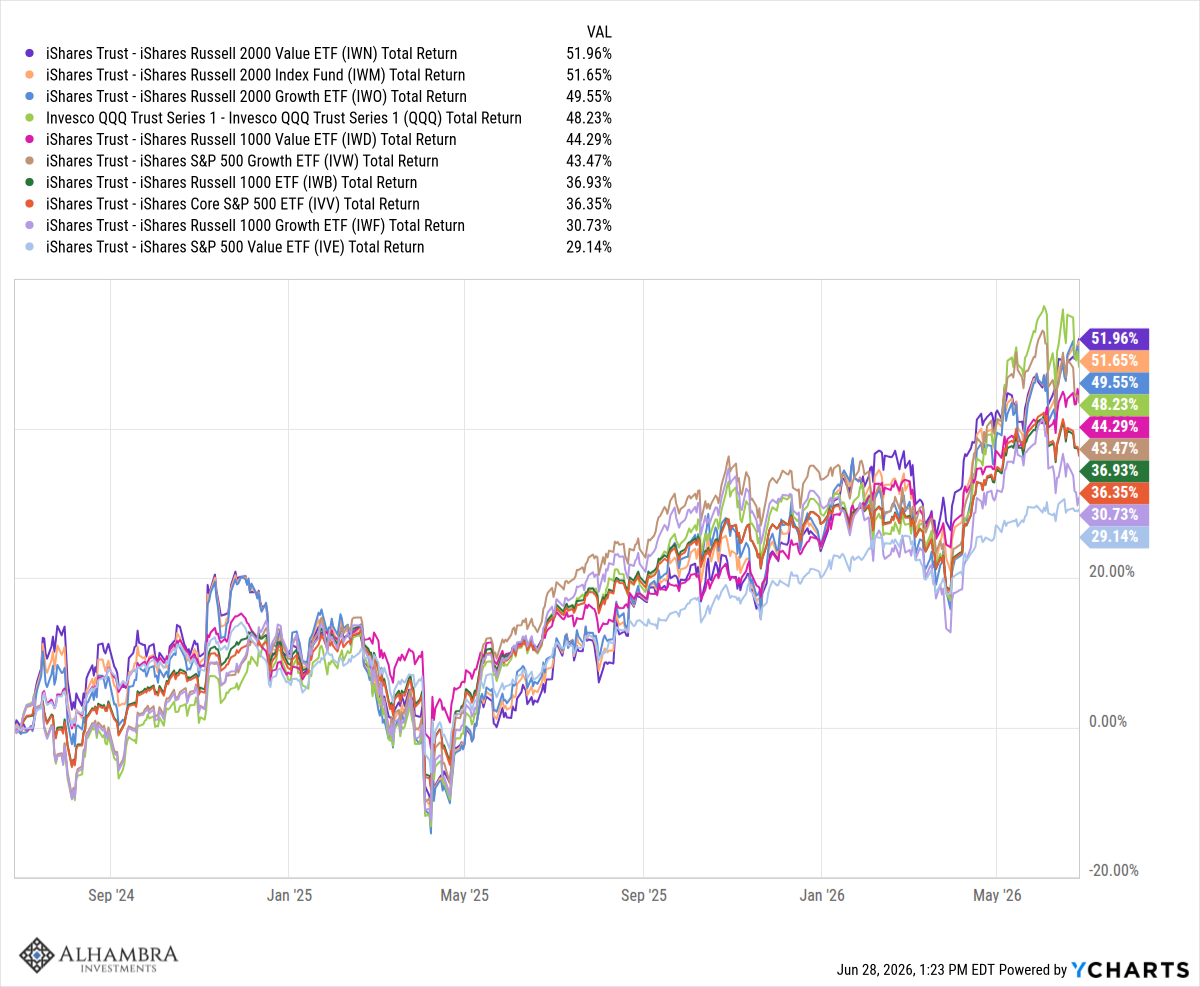

If you look at the last two years, you start to see a new leaderboard. Small value has moved to the top of the list while large growth has moved down.

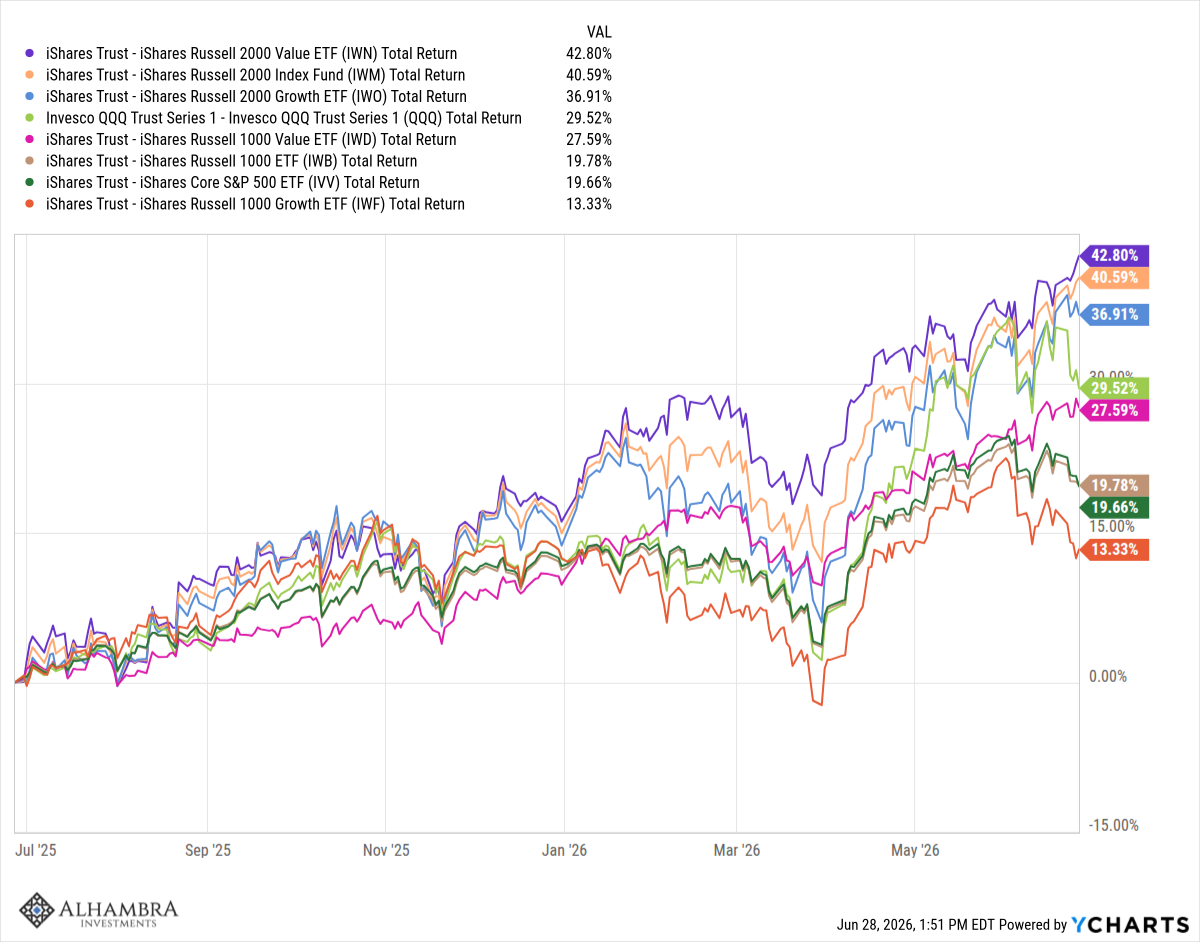

Over the last year, small cap stocks are still in the lead and the Russell 1000 value index has nearly matched the NASDAQ performance. Meanwhile, the blended indexes (Russell 1000 and S&P 500) have fallen and large growth is at the bottom of the list.

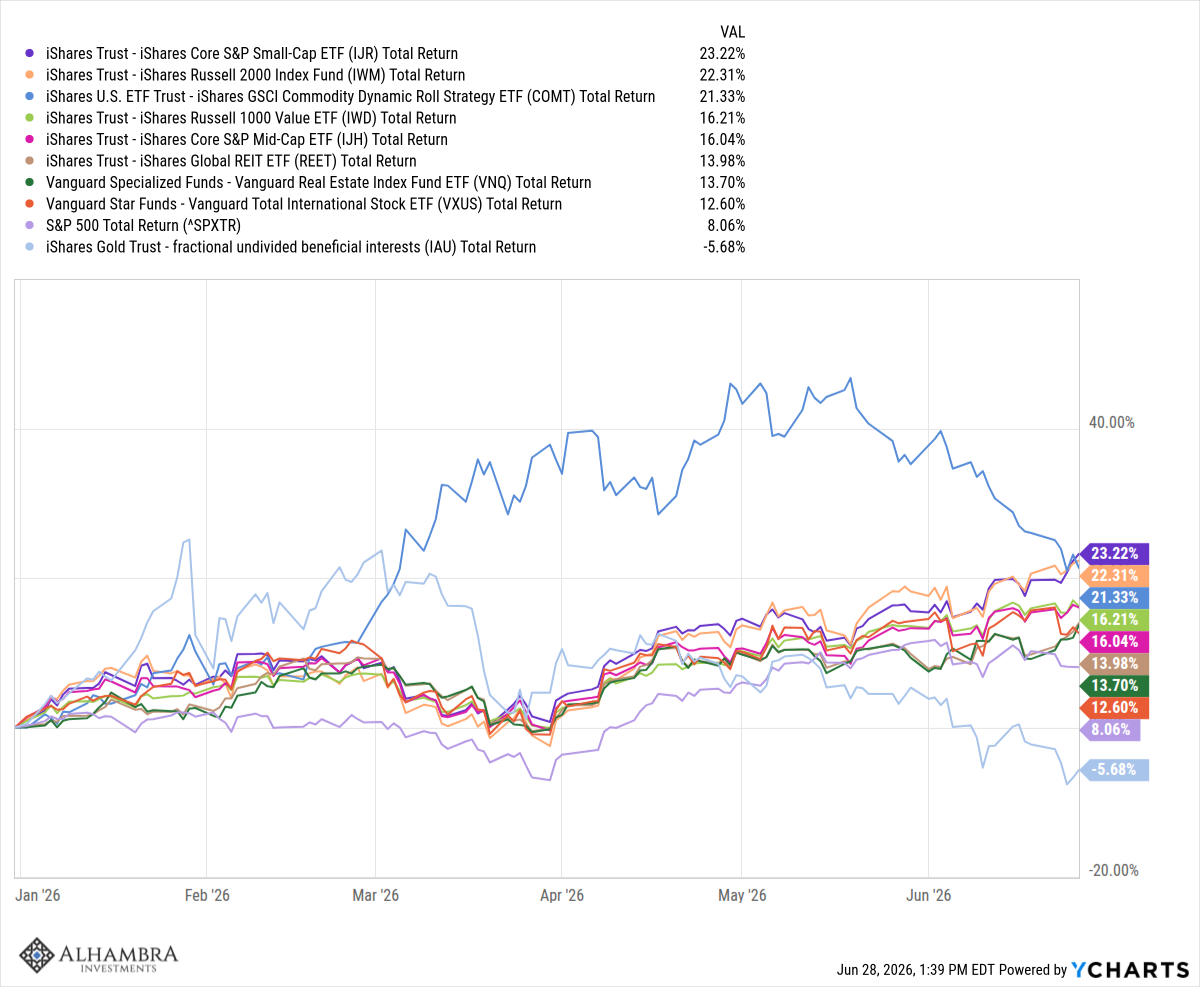

The shift has intensified some this year. In fact, there have been a lot of ways to beat the S&P 500 this year. Small and midcap stocks, value stocks, REITs, commodities and international stocks have all outperformed the S&P this year. Of the big asset classes we track, only gold has underperformed the stock index this year:

Will S&P 500 Underperformance Persist?

As a value oriented investor it is tempting to see this as the long awaited revival of value investing and to the extent the value indexes are outperforming, I guess it is. I would also point out that the outperformance of value goes back a ways since the 3 year numbers are pretty darn close to the S&P 500. The same could be said about small and midcap stocks which have been underperforming for a long time. Their performance has improved dramatically in relation to the large cap indexes over the last 3 years. But if you’re just looking at the index returns you aren’t getting the full picture.

Of the top 25 holdings in the Russell 2000 small cap index, 16 of them have a connection to AI. The Russell 1000 value index holds Micron, Google, Amazon, Intel, Caterpillar, Applied Materials, AMD and Sandisk in its top 25 holdings. Even in the real estate indexes, 3 of the top 6 names in the MSCI index and 3 of the top 5 in the Dow Jones index are AI related. I would also point out that, of the top 25 holdings in the Russell 2000 small cap index, none qualify for retention in the index based on market cap. The top holding, Bloom Energy, has a market cap of $71 billion. That’s not small by any definition of he word.

Bloom is very much an AI play, selling fuel cells for “behind the meter” data center power. It went public in 2018 at $15/share and traded up to $25 on day one. By October of 2019 it was $2.67 but recovered to trade back up to $25 in the summer of 2025*. Since data centers came calling the stock has climbed as high as $345 and today trades at $252. Most recent year over year revenue growth was 130% so it is definitely participating in the boom. But is it really worth 117 times next year’s estimated earnings? 20 times sales? For a company with an operating margin of 8%? Well, it isn’t in the Russell 2000 value index so I guess that’s okay.

About the only place you can go to avoid AI – mostly – is to the international indexes. The top four holdings in the Vanguard Total International Stock index are AI related (TSMC, Samsung, SK Hynix and ASML) but they only account for 9.4% of the index and technology is only 21% of the index versus 38% of the S&P 500. There are other indexes with even less tech exposure such as Schwab’s Fundamental International Equity index ETF with only 2 names of the top 25 AI related and tech sector exposure at just 13.1%. And it has outperformed the Vanguard fund over the YTD, 1,3,5 and 10 year periods as well as since inception in August of 2013. So, yes, you can get away from AI and technology but getting good performance while doing so is hard.

Will basically everything keep beating the S&P 500? Almost certainly not, but if you’ve been reading these weekly commentaries for a while, you know what I’m going to say – I don’t know. And neither do you. And neither does your brother in law (and your sister, sister-in-law or mom is probably the better person to ask about investing anyway; see here). But what’s happened over the last couple of years is why we diversify, because we don’t – and can’t – know what comes next.

The recent upturn in the stock market outside of the large tech names is welcome and it has certainly been a boon for diversified portfolios. Our Global Moderate Risk ETF portfolio, diversified across 6 asset classes, has outperformed the S&P 500 this year**. That probably won’t continue of course, but it is nice while it lasts. Stocks and bonds alone didn’t get you there by the way. The standard 60/40 stock/bond portfolio has worked incredibly well for a long time but there are conditions under which it does not do so well, some of which we’re experiencing today. Hint: stocks beat inflation over the long term but they don’t perform well when inflation is high.

I’ve spent years eliminating the things that don’t really matter for investing success so I could focus on the things that do and it turns out to be a shockingly short list. There are no sure-fire, can’t miss, right every time market indicators so stop looking. There are a few that increase our odds of success but good, intelligent investing is mostly about ourselves and how we react to events. In other words, they are completely within our own control. It isn’t easy but it is pretty simple.

Joe Calhoun

*Over the last 40 years the average first day return for US IPOs is about 19% but they underperform the market over the first two years after their debut. Small company IPOs perform the worst while larger company IPOs perform better, as you might expect. But there is a caveat: large company IPOs outperform if they are profitable when they come to market. Otherwise, not so much. Which is why I wasn’t much interested in the SpaceX IPO.

**This is not an audited report. I checked 38 accounts invested in that model and they have all outperformed the S&P 500 total return YTD. The returns for those accounts are after fees. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value. Asset allocation and diversification do not guarantee a profit or prevent a loss. This is also a very short time frame and these accounts have not outperformed stocks alone over the long term. Over the last year these same accounts are mostly within 1% of the S&P 500 return though. I find it fascinating that a diversified portfolio, even one that has an allocation to bonds that have done almost nothing over the last year, can keep up with the broad equity market. I’ve been doing this for well over 30 years and I still get surprised.

Stay In Touch