As a preface to this update ostensibly on Europe, it’s all really about Euro$ #5 sadly rounding into form. In this first part, I’m going to have resurrect the quotation marks surrounding the term “rate hikes”, or bring back RHINO (rate hikes in name only) given what’s going on in Treasury bills.

Not rate hikes, or enough of them.

Our dead horse needs more clubbing.

Where's that dead equine? I'm going to beat on it some more.

— Jeffrey P. Snider (@JeffSnider_AIP) May 5, 2022

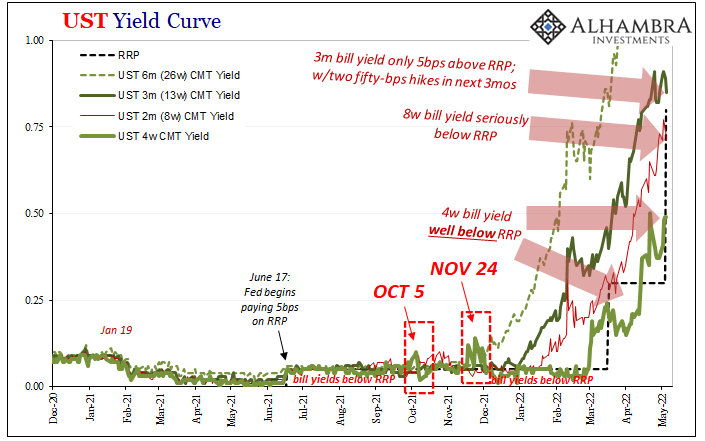

Tbills today:

4w @ 49bps, 31 less than RRP

8w @ 71bps, 9 less than RRP

3m @ 85 bps (down 2d in a row), just 5 above RRP even w/two fifty-bps rate hikes during those three months.

"Rate hikes" pic.twitter.com/G63Tt3R2iG

The numbers are simply staggering considering what they represent; and that is tightening which has nothing whatsoever to do with the Federal Reserve. Collateral scarcity remains paramount and the illiquidity which tags along seems to be spreading if still lumpy (see: equities).

That much is absolutely Euro$ #5 becoming nastier as more of the world’s monetary agents are herded into fewer available of these most pristine assets. The Treasury Department has partially responded to this imbalance, too, having announced plans to convert the 119d cash management bill into a regular benchmark (4-month) offering.

Considering where the 3-month bill is currently, more so where it is not given about 100 bps in additional Fed hikes are likely between now and three months from now, there’s ample reason for Treasury to make the move.

If only someone there would be honest about why bills are so “popular”, as the huge premium prices being paid for them attests.

For the mainstream audience, all they’ll ever say is, rate hikes, duh; as if investors (rather than collateralized leveraged systemic players) are staying up front on the curve given what the FOMC has in store.

Nuh uh. That does not, cannot explain those huge – and obvious – premiums particularly given the Fed’s alternative investment in the RRP. Popularity of these bills didn’t suddenly turn up because RRP or IOER are going up. That’s the beauty (for our purposes; to policymakers, this is too revealing) of the RRP because it exposes the underlying collateral truth in a way that none of the mainstream Fed-is-everything explanations can rationally explain away.

With all this in mind, Jay Powell says his rate hikes will be easily managed (why not, they’re pretend) because the economy is in such a great place.

Is it? Really?

As noted yesterday, according to quite a few measures the US economy is already in a place that last time had panicked Powell into rate cuts. Not to mention the negative Q1 GDP, which even if it doesn’t signal the start of recession, it sure does signify an overall weak therefore susceptible domestic situation.

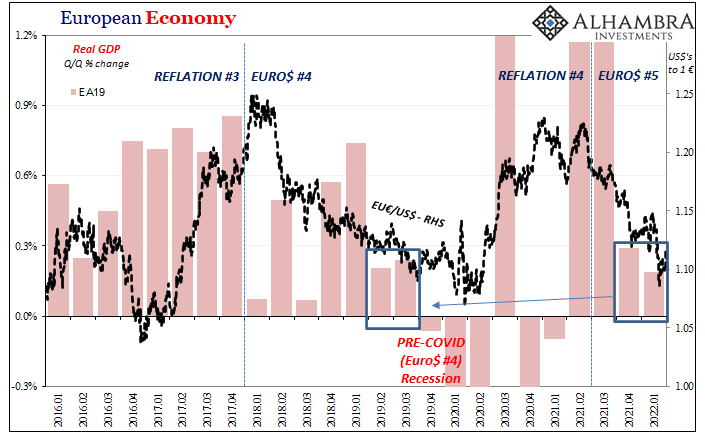

Here again, I’ll return to Europe. The reason is that buzzword globally synchronized, only now properly stated. The European Central Bank’s preference for a decidedly snail’s pace hasn’t diverged so remarkably from the Federal Reserve’s damn-the-torpedoes approach because Europe’s economy is heading in a different direction from its American counterpart.

On the contrary, the ECB is basically on hold given how much more obvious the weakness is there. Europe is merely further along heading in the same direction as the US is.

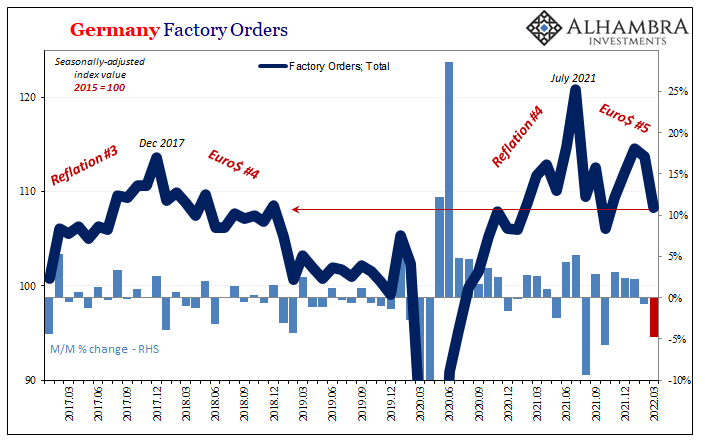

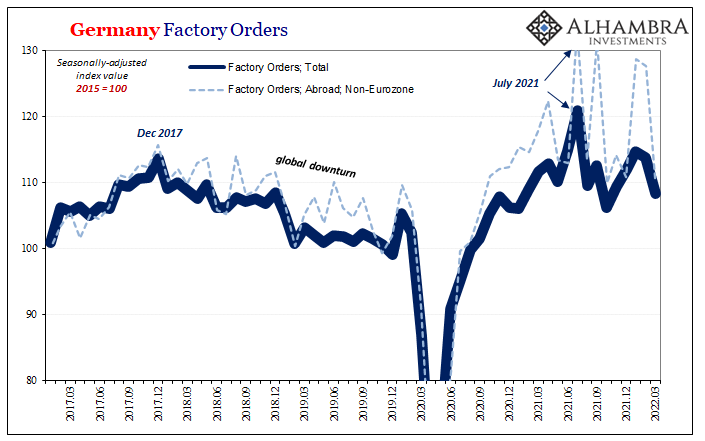

At the unfortunate forefront, as usual, the Germans. The latest data from there is pure Euro$ #5 and number five in the place where it will hurt the most: the goods economy, which means Germany’s externally-oriented factory sector.

According to deStatis, factory orders there plummeted in March 2022. While some of that decline can be blamed on the German government sanctioning Russia, cutting off goods trade, not all of it is war related. More than that, as you can easily see, the one segment of the economy doing the most has been doing a lot less since the middle of last year, long before our current geopolitically eruption.

Again, Euro$ #5.

These latest estimates show forward-looking orders now less than a year ago, the first annual decline since September 2020, and down to an output level that is now no better than December 2018 (not exactly a good month to be compared to) even though four-plus years have passed in between.

In other words, clearly not good.

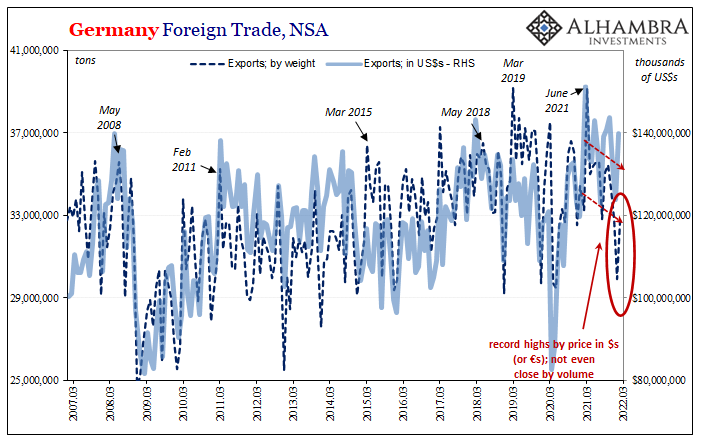

One key reason why is the downside to last year’s price illusion playing out at home (Germany) and abroad. To the latter, factory orders overseas have become extremely volatile and are now turning lower. This mimics the condition of German exports, which by value seem great yet by volume are awful already and getting worse (preliminary for March 2022 were bad in nominal terms, so we’ll have to wait see just how much more awful by volume).

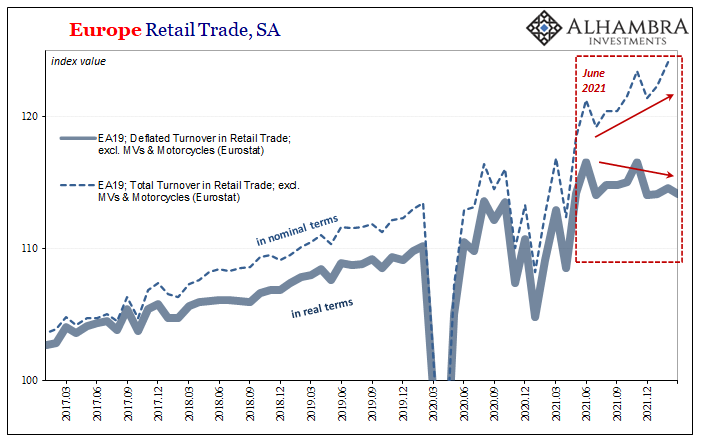

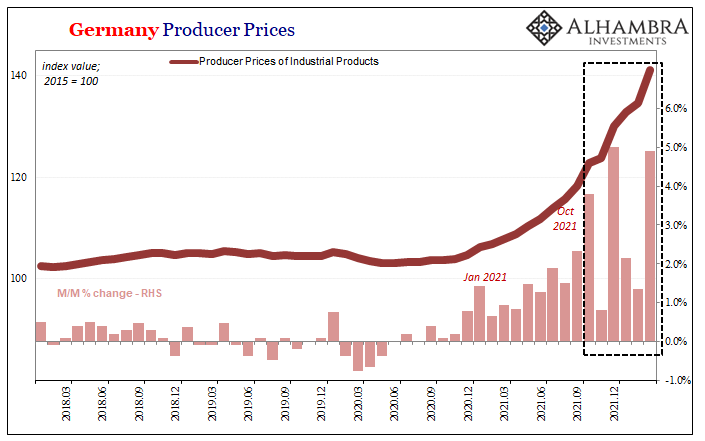

Domestically, retail sales in Germany are the exact same, the price illusion making it seem like Germans are spending – which they are – but also getting less for paying all the more. Sales in real terms have slumped, putting more pressure on producers who are at the same time being absolutely ravaged by input costs (PPI above; notice the change also in October).

This is not inflation. It is the demand destruction associated with the nasty “surprise” (for those convinced this is inflation) awaiting the downside of last year’s global supply shock.

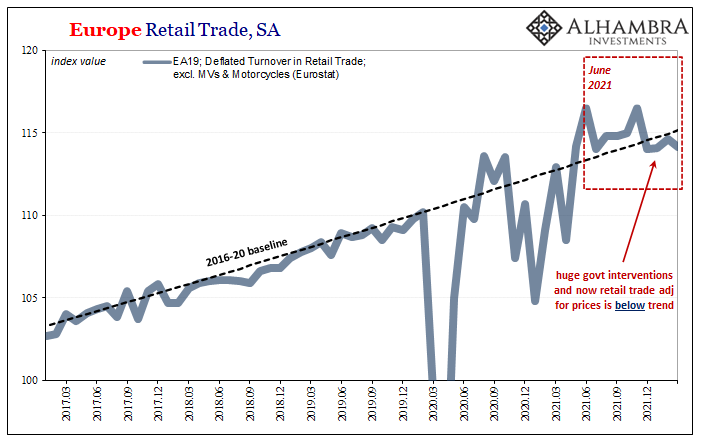

And, for consumers, it is global. Retail sales across Europe as a whole are an even better depiction of this condition; to the point that retail sales here have actually fallen below the prior, lackluster baseline trend!

This is why German factories are receiving fewer orders when not long ago (up to July last year) they’re resurrection might have seemed unstoppable. It was the risk, along with some others, that this was a mistaken impression, that price illusion rather than recovery had taken hold, which led to the formation (and vision) of Euro$ #5.

Risk aversion which then becomes self-reinforcing across markets and national sections of the global economy, more and more synchronized as #5 goes unchecked.

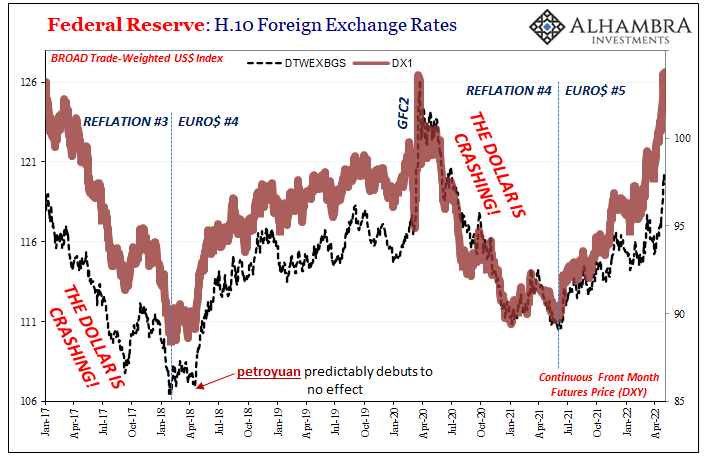

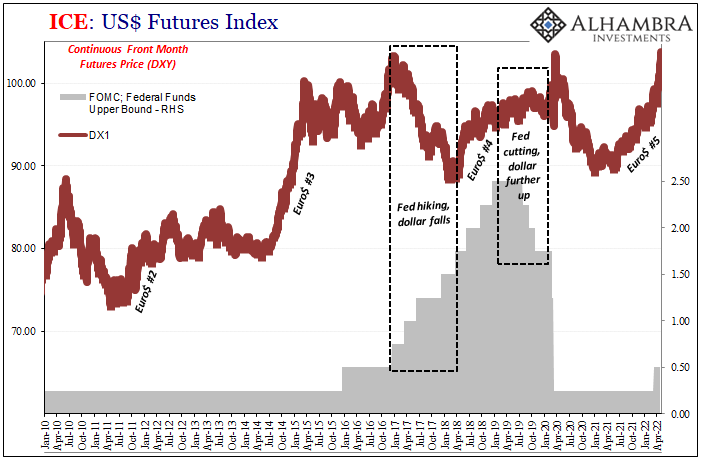

That’s the dollar’s behavior in exchange value, which has already done much of the dirty work Jay Powell is only now attempting with his fairy tale tools. Leading indicators, from T-bills to the European economy. Even if consumer prices are different this time, we’ve seen all this before.

Four times. Now five.

Stay In Touch