Predicting the future course of the markets – interest rates, stock prices, commodity prices – is impossible. That is true even in times when the future seems set, when it seems predictable, when there is consensus about the impact of all the factors that affect markets and ultimately economies. It is even more true during times of great uncertainty, times of great change, especially of a technological nature. It is even truer still when the actors who tend to move markets – politicians and central bankers, although that may be repetitive – make decisions that seem arbitrary and capricious.

Investors today face the uncertainty of great technological change – or at least we think so – and great uncertainty about future geopolitical and economic policy. The US and Israel bombed Iran over the weekend with the apparent goal of regime change, which they have accomplished with the killing of Iran’s Supreme Leader Ali Khamenei. Whether the new regime looks much different from the last one is yet to be determined, but the new crew has certainly not been shy about lobbing missiles around the rest of the Middle East in retaliation. War creates uncertainty no matter where it is prosecuted but when missiles are flying around an area of the world that supplies almost a third of the supply of oil, the impact on the global economy and markets can be extreme.

Or not. There’s no way to know; that’s what uncertainty is – not knowing. We could wake up tomorrow morning to the reinstallation of a western friendly Shah as the new leader of Iran. Or we could end up with someone worse than Khamenei, although finding someone worse would be a tall task, even in Iran. This is not the first conflict in the Middle East and we are accustomed – or at least those of us old enough to have done this a few times are – to seeing a spike in oil prices that fades with a resolution of the problem. We saw that in the first Gulf War when crude oil spiked from $16 to $40 from July ’90 to October ’90 and then fell back to $17 by early ’91. In the second Gulf War, the buildup to the invasion of Iraq pushed oil prices from $17 to $40 and prices fell as the war started, down to $25 a couple of months after the invasion.

We saw a similar effect when Russia invaded Ukraine a few years ago. Oil prices rose from $62 a few months before the invasion to $118 at its start and back to $63 a year or so later. With the attack on Iran, we saw a similar rise in the run up, with crude prices up from $55 in December of last year, to $67 last Friday and likely somewhere north of that come Monday. Or again, maybe not. US WTI crude oil futures have been moving toward contango for weeks, usually an indication the market is well supplied, maybe too well.

So, what should investors do? Probably nothing since none of us have any idea how this will end. It was once conventional wisdom that high oil prices were associated with US recession but with the emergence of fracking and the rise in US production, that isn’t as true as it once was. How long the conflict lasts could be a deciding factor but probably only if it impedes the flow of oil from the rest of the Gulf producers; the world does not have a shortage of oil even if Iran goes off line for a while.

The outlook for the economy is not, however, solely dependent on the outcome of the Iran campaign. The potential impact of AI on the future economy has been a recent source of angst, specifically concerning employment. A recent “research” report from a previously obscure firm has been blamed for some of the recent weakness in software stocks. Their thesis – a work of fiction that might be helpful to their portfolio – is that AI will raise productivity so much and so rapidly that it will cause mass unemployment. I am skeptical of the argument for a number of reasons but mostly because economics is not these guys strong suit. Near the start of the paper they introduce something they call “Ghost GDP” – output that “shows up in the national accounts but never circulates through the real economy”. The doom and gloom TLDR? AI is going to raise productivity so far, so fast that the economy will crash and unemployment will go to 10%. Um, yeah, sure.

Beyond that I’m skeptical of the argument because, based on my experience with other “game changing” technology introductions, the impact of AI will likely not be as big as the cheerleaders assume or arrive as quickly as they believe. High unemployment may be in our future – we have not repealed recessions – but I seriously doubt it will be a result of a surge in productivity growth. In fact, with the current administration’s antipathy toward foreigners limiting (reversing) immigration, the future growth of the US economy is almost entirely dependent on productivity growth. Indeed, AI may be the only thing standing between the US and a revival of that 1970s phenomenon we called stagflation.

Still, the prospect of job losses from AI seem real, especially after Jack Dorsey announced that Block (the parent of payments processor Square) would lay off half its workforce because of AI. Considering that Block has missed analysts’ earnings estimates the last four quarters, I’d bet that AI is just a convenient excuse, but what do I know? Paypal hasn’t exactly been killing it either so maybe it’s just the payment processing business as a whole. Or maybe he’s worried about stablecoins. But AI is making things so much better I can get rid of 4000 people? I’m not really buying it. You know who else isn’t buying it? The market. There has certainly been a selloff in several groups of stocks, most prominently software, that could be affected by AI – emphasis on could – but if the market believed in the 10% unemployment path for AI, the selloff would be widespread as almost every company would be affected by a recession. In fact, the opposite is happening.

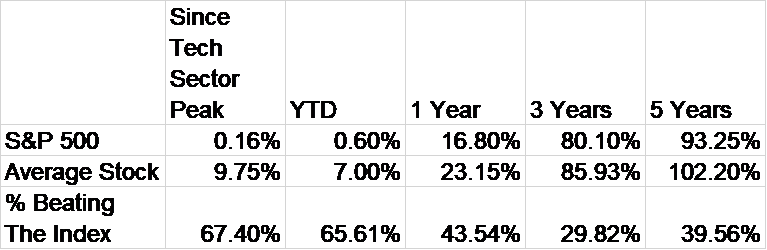

The technology sector peaked on October 29th and through Friday is down 10.2% over that period. That, in turn, has had a deleterious effect on the S&P 500, which had a tech sector weighting of over 34% at the peak. The S&P is up just 0.2% since then but think about what that means. If a third of the index is down over 10% since the end of October, the rest of the index had to rise over 5% to offset the tech loss. In other words, the market may believe that some companies will be hurt by AI, but it doesn’t seem to believe it will hurt the economy. If AI raises productivity it will be a positive for growth not a negative. That also happens to be consistent with the history of technological change.

Over the last four months, as the S&P 500 has treaded water, the average return of a stock in the index is 9.75%.

Since 1990, in an average year, 47% of stocks in the index managed to produce a higher return than the index itself but over the last four months that has jumped to over 2/3 of stocks beating the index. The 3-year and 5-year numbers are also interesting, in that they show that the market advance over those periods was very narrow. Beating the index over the last 3 years has been very, very difficult.

I can’t tell you what will happen in Iran and, in general, I don’t think investors should make portfolio changes based on geopolitics. Regardless of what you and I may think we know, I guarantee you someone knows more; we don’t have an edge that would allow us to make a wise decision right now. It is far better to focus on what we do know. Despite lots of uncertainty and turmoil over the last year, the economy hasn’t changed much. It is somewhat concerning that the 10-year Treasury yield dropped below 4% last week but we’ve been here in this cycle before and avoided recession. There isn’t enough evidence of a slowdown – yet – to make any portfolio changes. And because the economy continues to grow, stocks have done pretty well over the last year, especially if you wandered away from the S&P 500 and the tech sector.

As I write this on Sunday afternoon, I don’t know where the market will open tomorrow but I’d guess lower; there are always those who act emotionally at times like this. But don’t be surprised if stocks shrug off the attack; it wasn’t exactly a surprise.

This is a time when we should take Winston Churchill’s advice to “keep calm and carry on”. And remember we know a lot less than we think we do; that isn’t a Churchill quote at all.*

*The phrase was written for a poster produced in 1939 and if it was used at all, it was sparingly. In true Brit fashion – chin up, old chap – they did just that, without the need for written exhortations.

Stay In Touch