Can Tech Stocks Keep Outperforming?

Technology stocks have been outperforming for a long time. That’s how technology gets to be nearly 40% of the S&P 500 and the Russell 1000 and 60% of the NASDAQ 100. The concentration of the indexes in technology stocks is a function of how well they’ve performed and the performance has solid, fundamental roots. They continue to outperform this year, the AI boom the driving force now, but the outperformance of tech – and the underperformance of just about everything else – actually dates back to 2017. Ironically, while AI is driving today’s outperformance, it is also reversing the things that started the outperformance 10 years ago.

The period from 2017 to today has seen the technology sector outperform every other sector by a wide margin. In fact, tech is the only sector that has outperformed the S&P 500 over that time and the difference is kind of astounding. Technology stocks returned nearly 25% per year over that time while the index returned 14.7%. Seven of the eleven economic sectors generated single digit annual returns over that time while just three, other than tech, managed double digit returns: financials, industrials, and consumer discretionary. Most other times see roughly half the sectors beating the index and half underperforming.

What was the catalyst? There were actually two. The primary change was the maturity of the SaaS (software as a service) and cloud computing business models. Prior to this change, technology was a much more cyclical business. Companies went through capital intensive upgrade cycles in hardware and software. The shift to the cloud changed the industry from a cyclical, capital-intensive model to an asset light model that raised margins and reduced the need for capital. A secondary factor, the Tax Cuts and Jobs Act of 2017, allowed the tech companies to repatriate overseas cash and use it to buy back massive amounts of stock. Reducing the equity base raised all the returns on capital metrics and the stocks responded; higher return on equity indeed.

The problem investors face today is that the cloud computing companies are no longer asset light. Data centers are not just cloud computing on steroids and the necessary infrastructure investment is shifting the tech industry to an asset heavy, capital-intensive infrastructure model. The hyperscalers (Amazon, Microsoft, Google Cloud, Meta, Apple, Oracle, etc.) are engaged in a huge capital spending spree that is eating capital well beyond their available free cash flow. The most obvious example is Alphabet’s (Google) recent secondary offering of convertible preferred and straight equity of $85 billion. They aren’t the only ones changing direction; Amazon, Meta, Microsoft, Oracle, Salesforce, Intel, Cisco, AMD, and Apple have all either stopped their stock buybacks or severely curtailed them. Meta is supposedly considering an equity offering of its own. And don’t forget the SpaceX IPO and the expected OpenAI and Anthropic offerings later this year. The age of shrinking equity is coming to an end.

Less noticed – at least by most equity investors – is the massive issuance of debt. The five major hyperscalers issued $120 billion in debt in 2025 and AI-related debt this year is expected to reach over $500 billion with almost $150 billion already announced by the big five. Return on equity is at an all-time high for the sector because of this new debt; the ROE/ROIC ratio sits over 6 for the sector. In addition, ROE has been goosed by all those stock buybacks shrinking the equity base since 2017. That is changing and will start to show up in a lower ROE over the next few years. With buybacks off the table – at least for now – the equity base will rise naturally due to employee equity/option grants. That will reduce ROE but ROIC will also compress due to increased debt. Furthermore, interest costs will reduce net income which will tend to reduce both ROE and ROIC. Tech stocks outperformed for ten years because of conditions that are now coming to an end.

Having said that, how tech stocks perform in the future still depends on whether they can produce an acceptable return on these investments. As you might have guessed, I have my doubts. These stocks today are priced as if the outcome is a foregone conclusion but there are a lot of ifs that can’t be answered right now:

- Will the price of compute fall? If all the capacity on the drawing boards is actually built, I think the answer is obvious but will it be built? That’s a legitimate question as there are some powerful bottlenecks such as shortages of transformers, switchgear, cooling systems, battery backups, gas turbines, memory chips, and possibly the most critical, labor. Even if all those are solved, the grid isn’t ready to add all the new capacity needed to power all the data centers on the drawing board. And don’t forget the NIMBY public backlash. If AI capacity is limited because of these shortages, prices may stay high. On the other hand, delays mean a slower revenue run rate for the suppliers – like Micron for instance – and the market probably won’t like that.

- Even if fewer data centers are built due to shortages of critical materials, what gets built could still be too much. Software engineers are figuring out how to achieve the same algorithmic results using vastly less compute. Through breakthroughs in model architecture, quantization, and small specialized language models, the amount of compute required to perform a task is dropping exponentially. If a task required 100 GPUs to process in 2024, but software optimization allows it to run on just 2 GPUs now, token prices may be irrelevant.

- Will chips continue to advance at a rapid rate? If they do, will the hyperscalers be forced to continue their large investments? If chips are fully depreciated over 3 or 5 years, what’s the impact to reported earnings? The OBBBA included expensing of investments with a life under 20 years but that is a tax issue and doesn’t impact EPS.

That’s just a few of many unknowns right now and there are more, some of which we can’t even imagine right now. As with past technological changes I suspect it will not be the tech companies who build the AI infrastructure that will be the biggest beneficiaries. The companies that built the railroads in the 19th century weren’t the biggest beneficiaries; indeed many of them went bankrupt. But Sears created an entire industry on mail order delivered on cheap rails. It wasn’t the companies that laid all that fiber optic cable around the turn of the century who benefitted either. Global Crossing went bankrupt installing fiber no one knew what to do with but Amazon and the streaming companies turned that capacity into cash. And I expect AI to be no different. If computing power becomes ubiquitous and cheap – and I think that is highly likely – it will be the companies that put that excess capacity to its best use that benefit the most. That may include some technology companies – ironically considering how the market is punishing them today, I think software companies are an obvious beneficiary – but most of them will be from other sectors.

Can tech stocks keep outperforming? I suppose anything is possible. The sector has, after all, been outperforming for ten years and continues to do so while still posting great earnings. But an AI-dominated technology sector isn’t the same technology sector that beat the rest of the market by 15%/year for ten years. All good things come to an end and technology’s run will too. The industry has already invested over a trillion dollars in AI since 2023 and the run rate is expected to be over $1 trillion a year by 2030. Or so some analyst guessed in a “research” report I read recently. Jensen Huang, who might be talking his book, says the total of the physical infrastructure installed on the global grid will reach $3 to $4 trillion by the turn of the decade. Can the industry turn all this investment into a return that justifies today’s stock prices? They better.

Mid-Year Market Update

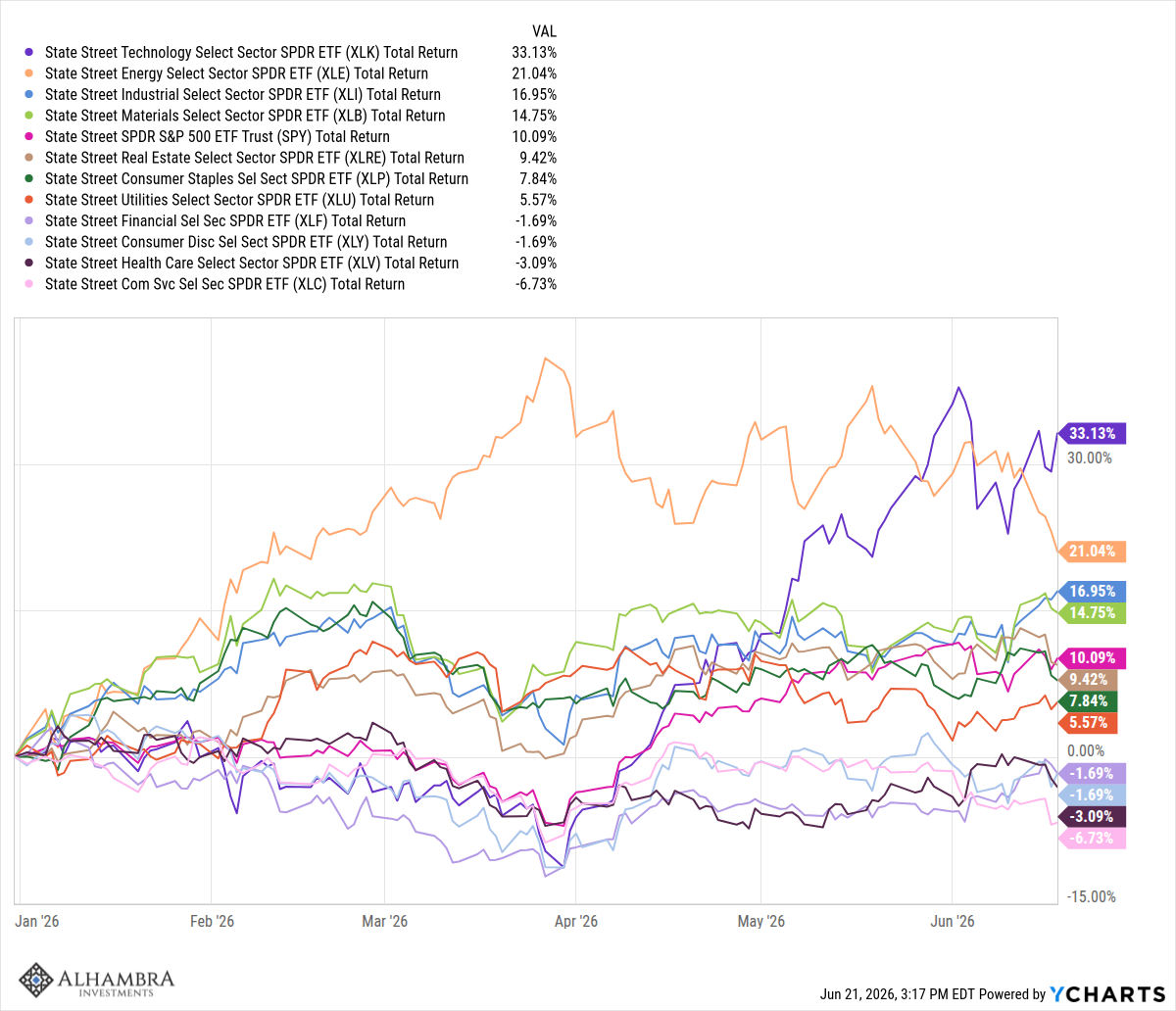

There have been two competing narratives this year in the investment discussion – the Iran War and the AI buildout. We can see that impact in sector returns YTD where technology, energy, materials, and industrials have all outperformed the S&P 500:

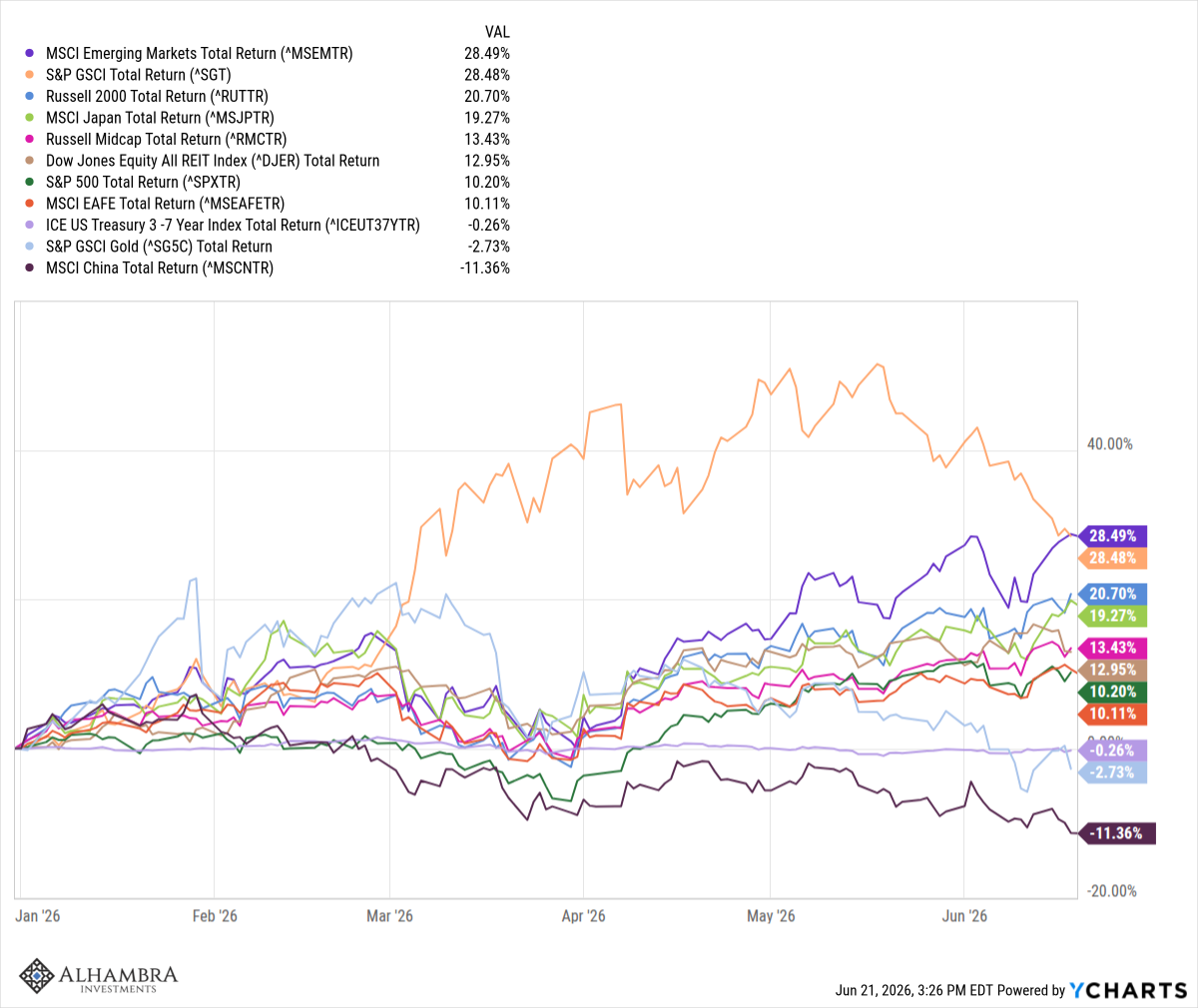

We can also see the effect in the global markets across asset classes, although it isn’t as monolithic. Roughly half of the EM index is in South Korea and Taiwan, which are obviously benefitting from the AI buildout. And commodities are an obvious beneficiary of the Iran War-driven rise in the price of oil (even though it has come down a lot in the last few weeks). But other areas like small and mid-cap stocks, Japan, and REITs aren’t all that connected to AI or the war. If anything, Japan has been negatively affected by the war and REITs should be negatively impacted by higher interest rates. It is also interesting that the EAFE index has managed to keep up with the S&P 500 despite a firm dollar and little connection to AI in developed economies outside the US.

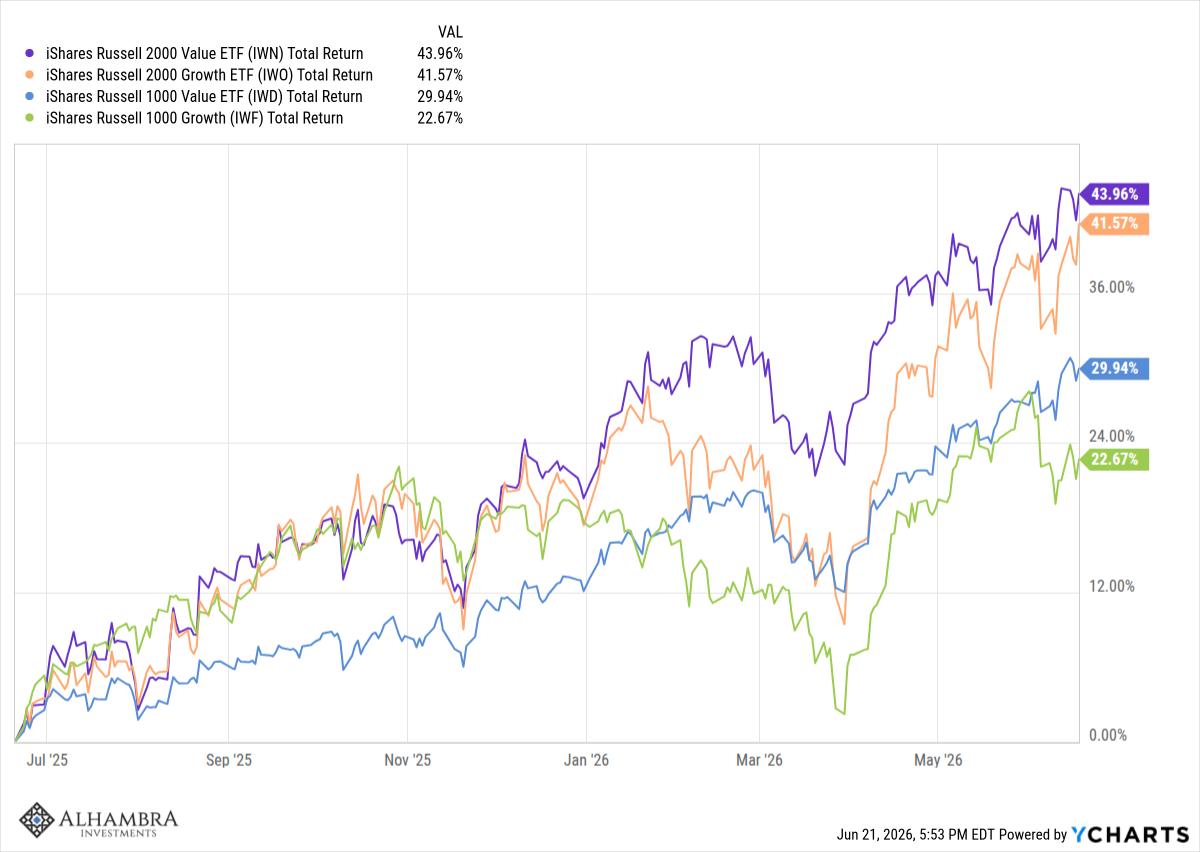

Growth vs Value is a messy affair this year with some value indexes winning and some growth indexes ahead. In the Russell complex, it is value winning in small and large:

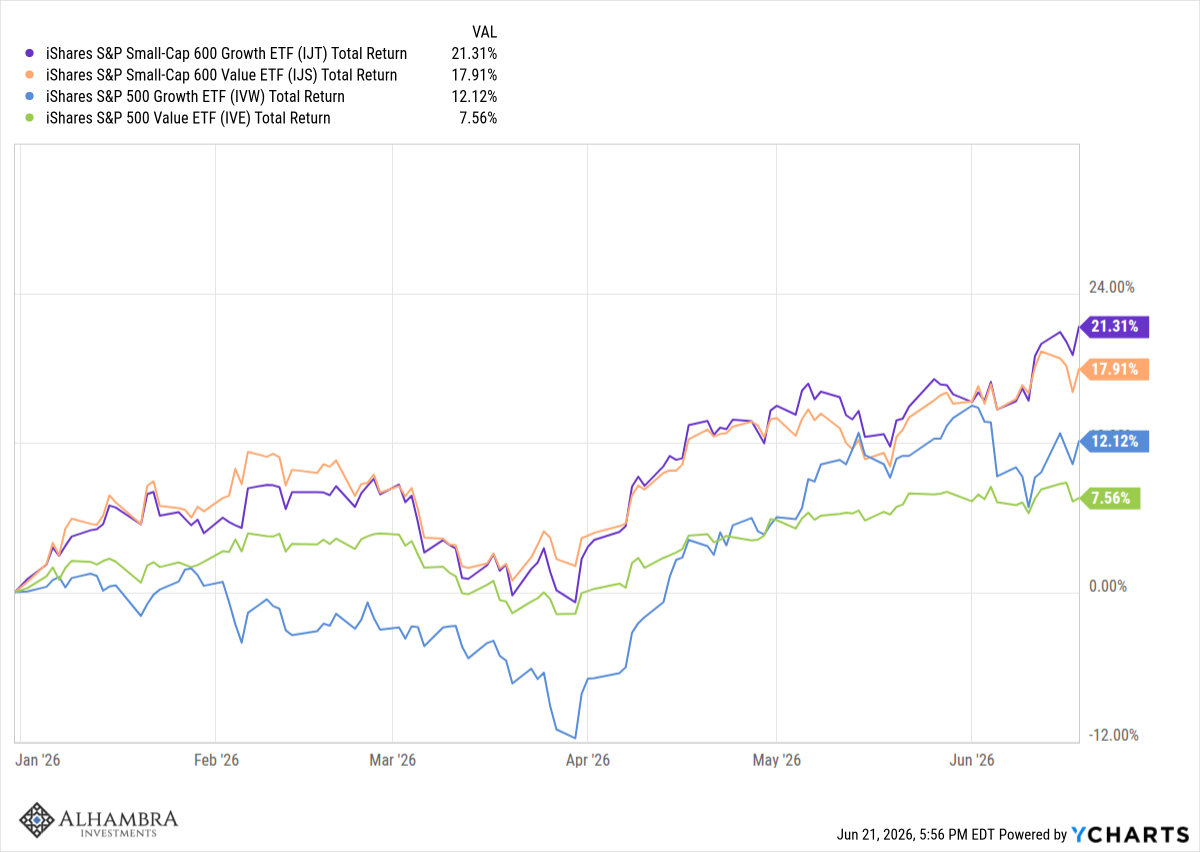

But growth is the winner in the S&P indexes:

Real estate has performed well this year despite a rising interest rate environment:

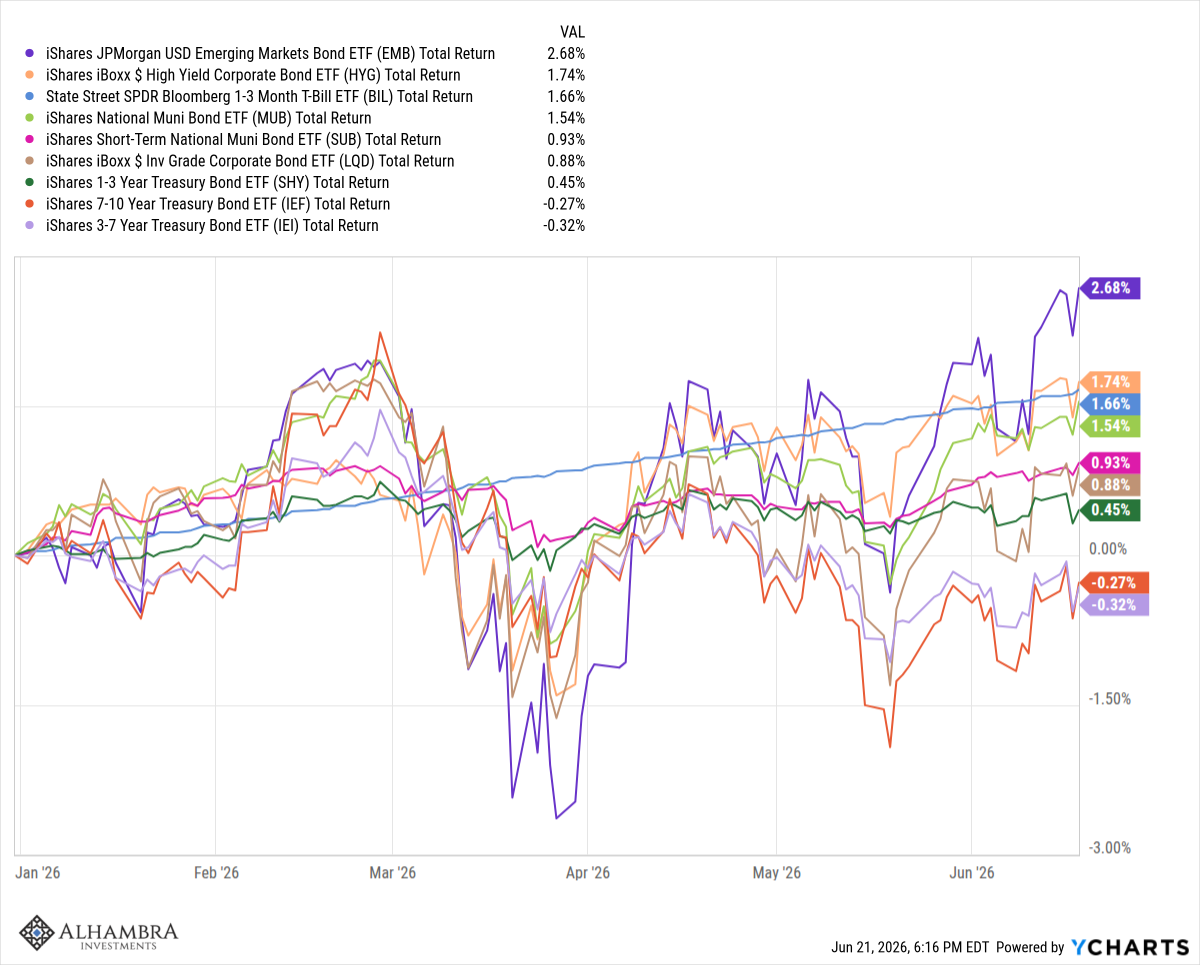

Making money in bonds this year has been a matter of sticking to short duration or taking on some credit risk. Dollar-denominated EM bonds were the biggest winners with junk a close second.

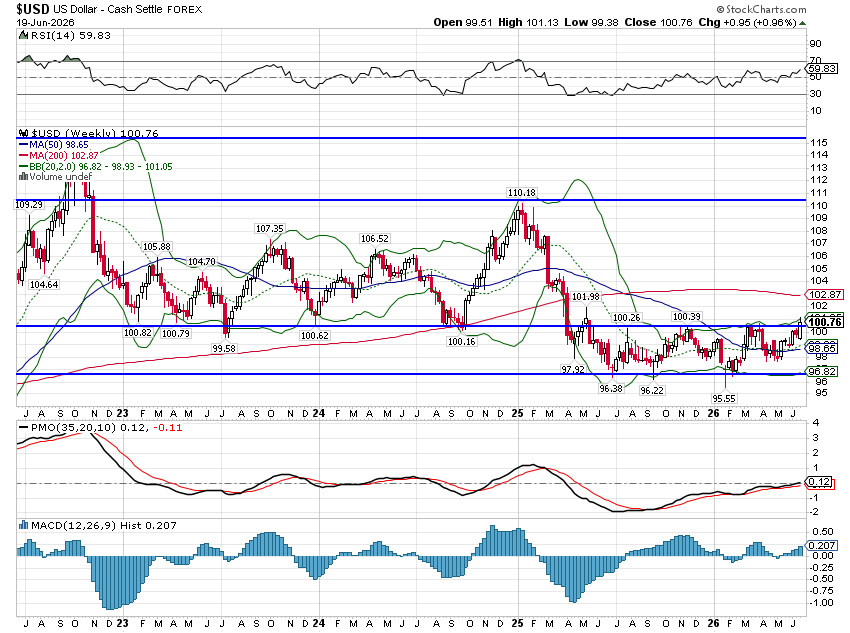

The dollar is up 2.5% YTD and is threatening to break out to the upside. This is being driven by rising rates and a shift in expectations regarding monetary policy. It may continue for a while and a move up to around 105 would not be shocking but with market-based inflation expectations falling (down 45 basis points since the beginning of May for the 5 year breakeven), I don’t expect it to last. A rising dollar will be a drag on non-US dollar assets until this rally ends.

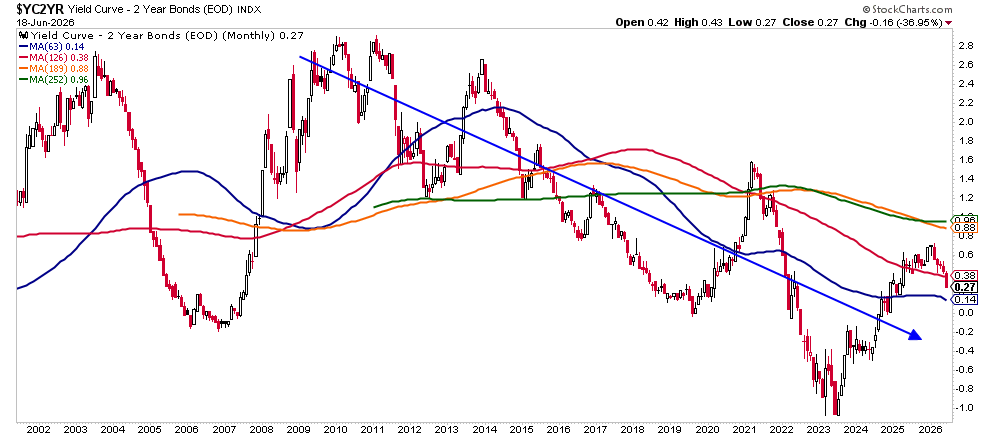

Short-term rates have been rising faster than long-term rates recently so the yield curve has been flattening. Flatter curves are generally associated with slower future growth but the change isn’t significant enough to make a call like that yet.

Valuations for stocks have fallen a bit this year even as prices have risen but some of that is due to one-time factors that probably won’t repeat (mark to market gains on AI stock holdings). Stocks are still expensive and we are probably getting close to a cyclical peak in tech earnings. Given the changes to the sector I outlined above, it may be a secular peak but there’s no way to know yet. At the same time, interest rates are rising which is generally a headwind for higher stock prices but as I said above, inflation expectations have been falling as the Iran War winds down (assuming it really is). Sentiment is too strange to parse right now; there’s speculative activity all over the place but more traditional sentiment metrics are pretty neutral. I’d suggest approaching the second half with low expectations and a sense of history. Midterm election years – second years of the Presidential cycle – are historically the worst of the four year cycle but tend to perform better after the election. Having already exceeded the historical average for this year, a more subdued second half would not surprise me.

Joe Calhoun

Stay In Touch