We have a lot to be thankful for here in the US of A. It is sometimes hard to remember that while being constantly bombarded by negative news, about the economy and the country more generally. I don’t like to comment about politics – I have to watch my blood pressure these days – so I’ll stick to economics and despite the problems we have, there is a lot to be thankful for. The current data reflects an economy still trying to rebalance from the COVID shock; the goods/manufacturing side still working off a hangover from the COVID stuck-at-home buying spree and the services side continuing to recover.

The result is an economy growing roughly at trend of 2% and I’d say that’s pretty amazing given the enormity of the COVID shock. But I’ve been writing and talking about that rebalancing for over a year so it isn’t a surprise. And frankly, it wasn’t that hard to figure out, that the goods boom wouldn’t last and neither would the services bust. COVID and the response to it had a dramatic impact on consumption and balance sheets.

The trends in consumption were already in place – goods consumption has been rising relative to services since 2009 – while the changes to balance sheets were more profound. Household and corporate balance sheets improved – dramatically – while government finances deteriorated – dramatically. That’s why we’ve been consistently saying, for over a year, that recession isn’t imminent. That could change but it hasn’t so far and markets certainly aren’t predicting it right now.

Everyone knows the bad things going on right now. Our government makes drunken sailors look prudent (and that from an ex-drunken sailor), there are multiple wars going on, China isn’t to be trusted, our own political process has turned into a circus, prices are still rising, mortgage rates are through the roof, rents are crazy, and all commercial real estate is on the verge of foreclosure.

But there are some good things going on if you take the time to look:

- Real disposable personal income (adjusted for inflation, after tax) is up 3.5% over the last year

- Real personal consumption expenditures are up 2.4% over the last year

- As of Q3 2023, the delinquency rate on all loans at US commercial banks was just 1.33%. The average since 1985 is 3.27%.

- As of Q3 2023, the delinquency rate on single-family mortgages was just 1.7%, down from 2.3% prior to COVID

- Light vehicle sales (cars and trucks) are up 14.3% over the last year

- Consumer prices are up 3.2% over the last year. That’s down from a 9.1% annual rate a mere 17 months ago

- Producer prices are only up 1.3% over the last year. Corporate margins are fine.

- Import and export prices are both down over the last year (2% and 4.9% respectively)

- Median sales price of a new home is down 12.3% over the last year

- Single-family new home sales are up 33.9% over last year

- New claims for unemployment are essentially unchanged over the last year at generationally low levels

- The economy has added nearly 3 million new jobs over the last year

- The unemployment rate is 3.9%, up from 3.4% in April which was the lowest since 1969

- The labor force participation rate has risen from 62.2% to 62.7% over the last year

- Real average hourly earnings are up 0.8% over the last year

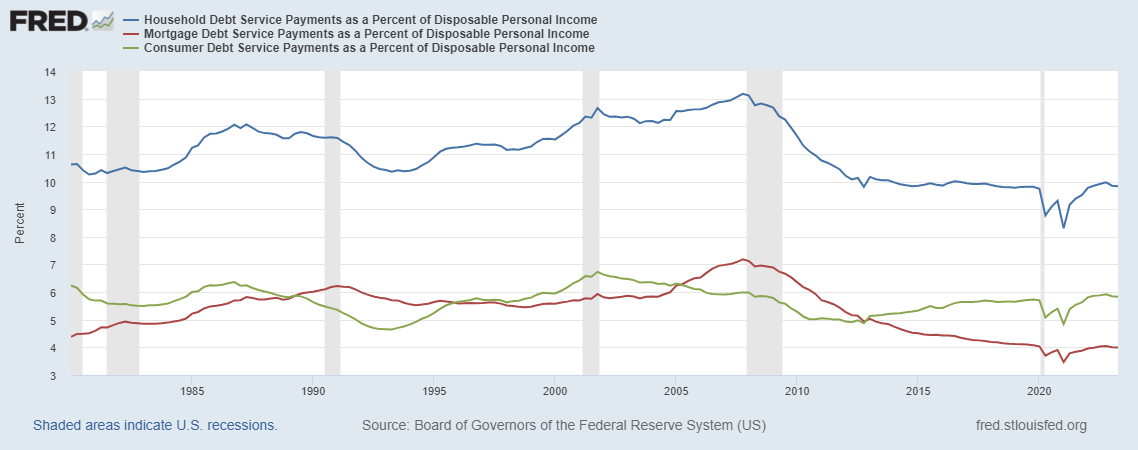

- Household debt service payments as a % of disposable personal income are less than 10%

- Mortgage debt service payments as a % of disposable personal income are less than 4%

- Consumer debt service payments as a % of disposable personal income are less than 6%

I’m not saying that we don’t have our problems because, of course, we do. There are always parts of the economy that are undergoing change, sometimes good, sometimes bad. That’s just how economies work. You can’t look at only one side of the ledger and expect to get a clear view of the world. And that applies to those who always look for clouds as well as those who see only silver linings.

Environment

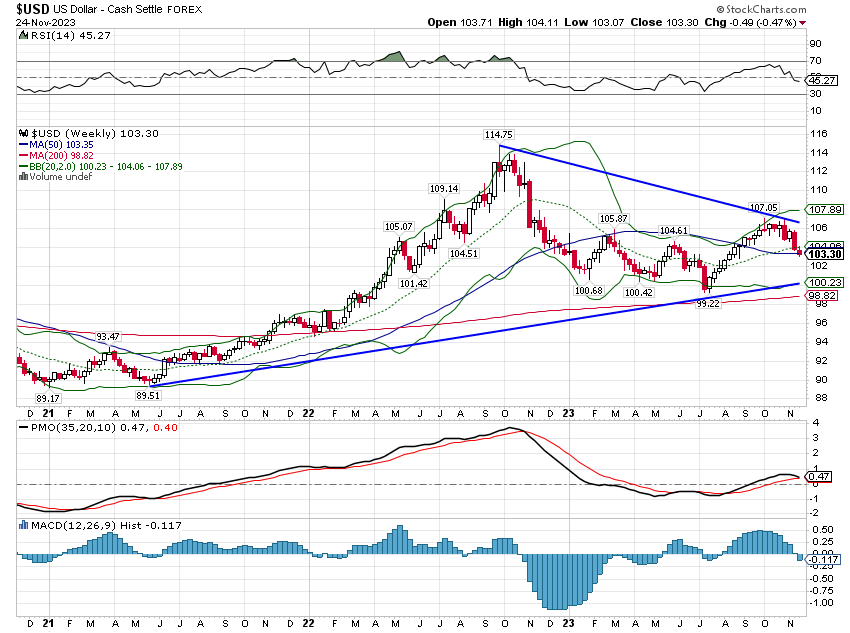

The dollar is pretty clearly in a short-term downtrend with all the time frames we monitor weekly now in the red. It isn’t a big move though, down just over 2% in the last year, and it doesn’t warrant big changes to your portfolio – yet. For now, the intermediate and long-term trends for the dollar are still up.

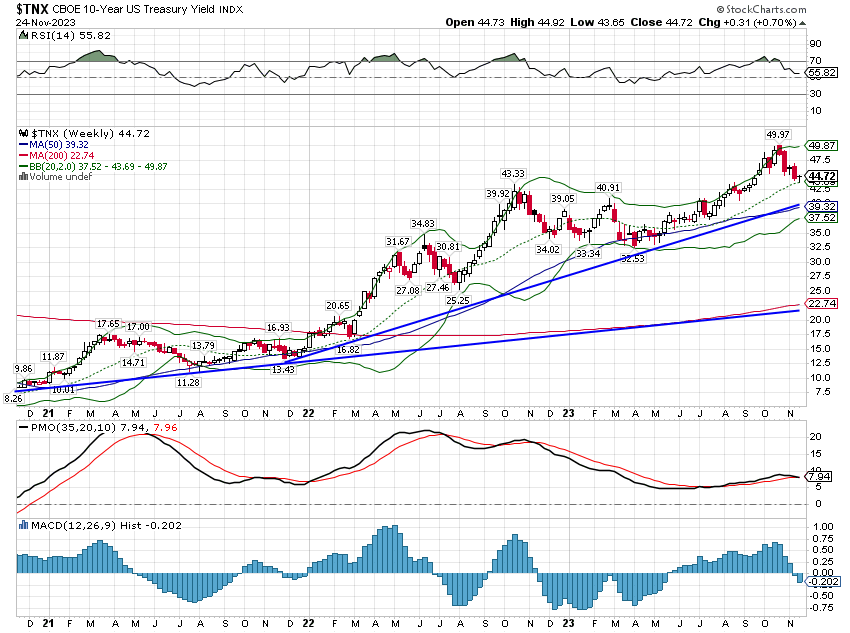

The 10-year Treasury yield was up very slightly over the last week but the intermediate-term trend remains up as well. A move down to 4% seems quite reasonable. The belief that rates have peaked seems quite widespread now and so, of course, I’m starting to get a little skeptical. I have a long-term view that rates and inflation are going to be higher, that this is a secular change from the post-financial crisis period. I’ve also said I think this is a cyclical peak but right now I’m wondering if it will prove short-lived. For now, I think we have to respect the intermediate-term trend and wait for more evidence.

Markets

Note: The figures below are for the last 5 trading days not just the previous calendar week.

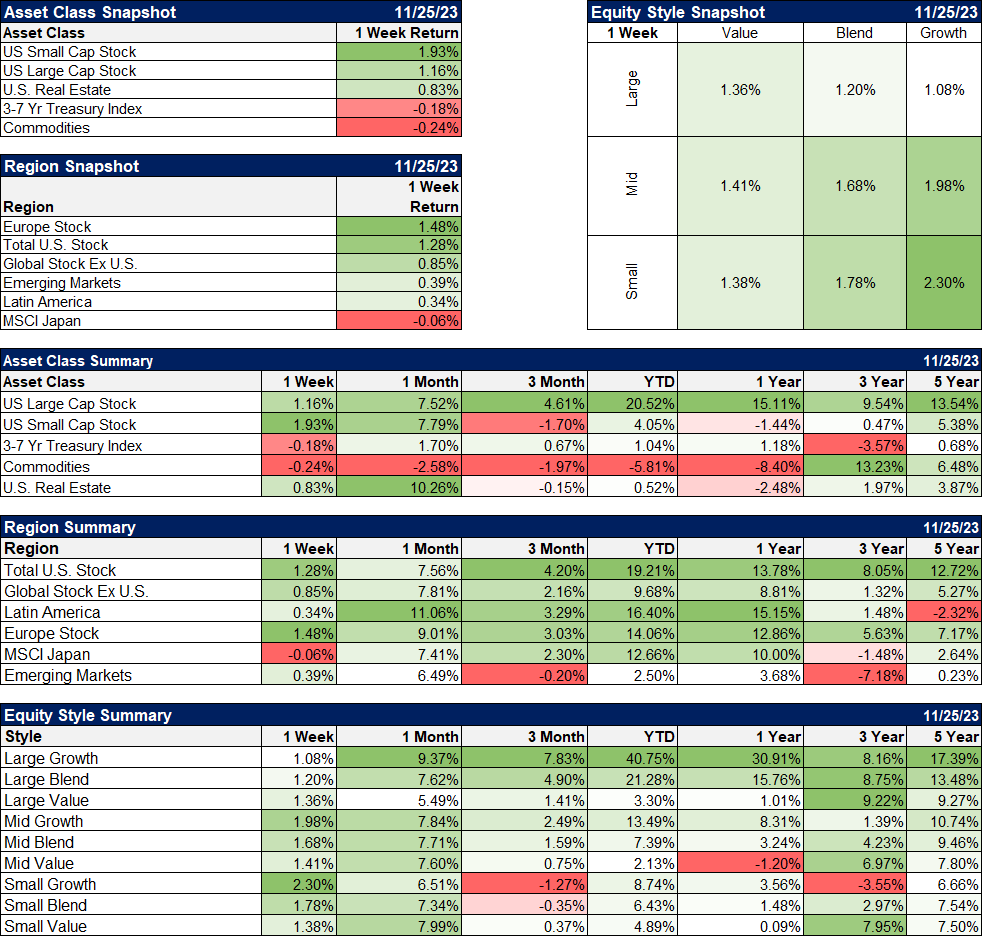

Small and midcap stocks have performed pretty well in November with the Russell 2000 slightly outperforming the S&P 500. Still, large caps have been the place to be this year, and growth stocks especially. And the trend isn’t new with large cap leading over the last 3 years as well. That doesn’t apply to value which has outperformed growth over the last 3 years.

From a valuation standpoint, small and midcap and especially value are the obvious choices but that hasn’t mattered much. Even if you exclude the weak companies of the Russell 2000 by shifting to the higher quality S&P 600, you still get small-cap underperformance. I don’t know when this will change but if history is a guide, when it does the result will be quite satisfying. In the meantime, it’s nice to at least get a month where holding small value doesn’t feel like the dumbest idea you ever had.

As noted above, the figures below are for the last 5 trading days.

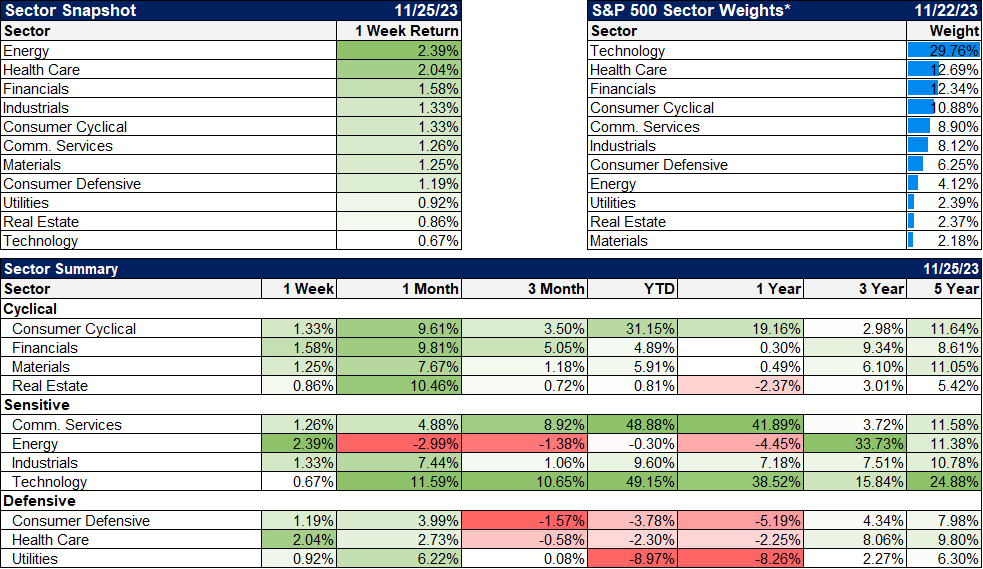

Healthcare was the biggest winner of the holiday-shortened week, up 2.25%. The sector has been in a 2-year+ holding pattern and this didn’t change that but it is back to the long-term trend. This is certainly not an investor favorite right now so it might be a good place to research.

Real estate continued its recovery and is now positive for the year.

Market Indicators/Economics

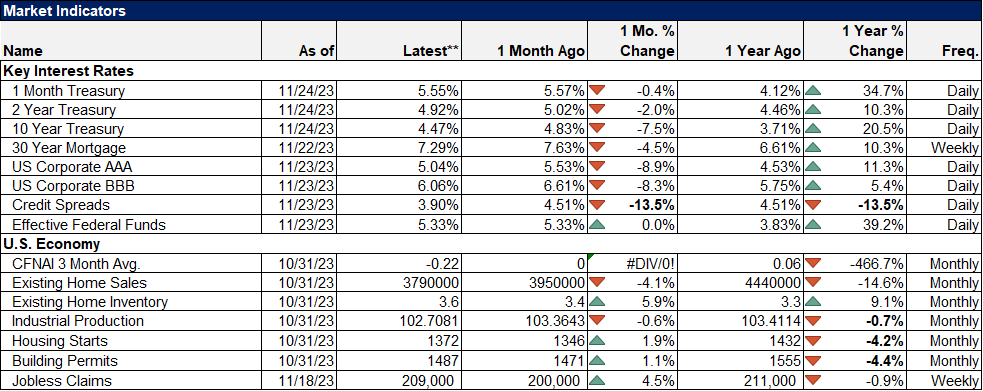

The economic data last week was pretty slim but a few things stand out. The CFNAI (Chicago Fed National Activity Index) fell -0.49 and the 3-month average fell to -0.22. Normally, this would worry me some because a reading on the 3-month average of -0.75 is associated with recession. But last month’s drop was concentrated in production-related indicators like industrial production. IP was down because of the UAW strike so this should be a short-term thing. We’ll see next month but for now, I don’t think the drop in the CFNAI means much.

Doug has commentary on the week’s economic releases.

Thanksgiving Week Economic Releases

Credit spreads have continued to narrow with the October rise now fully reversed.

There are plenty of problems in the world and it doesn’t take much effort to find someone who can’t wait to tell you all about them. Good news requires a little more work because “The Economy is Doing Fine, Go See A Movie” doesn’t get nearly as many clicks as “The Entire Banking System May Collapse Next Week”. But you’d be a lot better off doing the first thing and ignoring the last one.

The economy goes through many ups and downs during the course of a business cycle. Sectors ebb and flow, prices rise and fall, supply and demand wax and wane, all responding to the whims and desires of millions of individuals. That’s what happens in a (mostly) free market economy. Unless you know some way to predict what those billions of individuals around the world are going to do, I don’t know of any way to predict what the economy is going to do. So stop trying to predict the future and concentrate on the present.

Joe Calhoun

Stay In Touch