Stocks were up nearly 4% last week due to a ceasefire between the US and Iran that was supposed to open the Strait of Hormuz and allow oil to start flowing again. Crude oil fell 14% while the GSCI commodity index fell almost 7%. The dollar, which really hadn’t rallied much during the conflict, fell 1.3%. All of this despite the fact that evidence of the strait opening was conspicuous by its absence. There may have been a few more ships that got through last week but it was nowhere near what normally transits the narrow passage. And now, as I write this on a beautiful spring afternoon in South Carolina, trying to watch the Masters, word comes that peace talks have failed and President Trump has threatened to blockade the strait. Oops.

The rally off the lows actually started two weeks ago – the S&P 500 bottomed on March 30th – but all that did was get the YTD return back to flat. If you’re trying to trade around this war – and I don’t know why anyone would – what do you do now? Last week looked like the kind of whipsaw we often see in corrections where the index resumes its previous uptrend. But unless something positive happens next week, that’s going to look like a big head fake in the rear view mirror. If you were lucky enough to buy the low, what’s your P&L going to look like tomorrow morning? Up a few percent?

I think most investors think of risk control in terms like this; they want to sell at the high and buy at the low. The problem with that is that it requires you to sell when everything looks great and buy when everything looks terrible. It is a very difficult thing to do in the real world. There is also an asymmetry to tops and bottoms that I think few appreciate. There’s an old saying on Wall Street that tops are a process and bottoms are an event. I’ve been an investor for 44 years (I bought my first stock in 1982) and that describes most of the corrections I’ve lived through. And this market top – whether it is the beginning of a bear market or not – has been a long process, one that goes back to the end of October. Yes, October.

The Iran War has gotten the blame for this correction but the S&P 500 has gone nowhere since October 28th, almost six months ago. Yes, the main correction happened over a short period of time but I’m not even sure that is mainly about Iran. The S&P 500 made a nominal new high on January 27th – again, well before the Iran War started – and fell 9.1% to the low at the end of March. What’s interesting though is that most of the stocks in the index did better than the index itself. 325 stocks fell during the correction but only 177 of those were down more than the market and the average stock was down less than 3%.

From a sector standpoint, it does look like a broad correction with 9 of 11 sectors down but as with the individual stocks that make up the index, 9 of 11 sectors outperformed the index. The two laggards were technology and consumer discretionary.

If, on the other hand, you date the correction start to late October (the January high was less than 1% above the October high), things look quite a bit different. From the October peak to the March low, 5 sectors were up, 1 was flat, and 5 were down. And again, only two performed worse than the index – you can guess what they were. So, either way, there’s been a correction but taking the longer view shows that it isn’t really affecting “the market” that much unless you define the market as the S&P 500.

It also shows that if market timing is your preferred method of risk control, you really should have started selling in the 4th quarter last year when things were still frothy, especially in the tech sector. Buying back in is a bit trickier but there are two methods that have produced good results in the past. You can use the VIX as a guide or just start to buy when the index drops 10%. For the VIX you want to start buying once it exceeds 30 – with the knowledge that the VIX could go a lot higher – and average in over the next 6 months. That produces good returns 1 year out. Buying after the index drops 10% also produces good results; the index is higher after 1 year in 75% of corrections/bear markets since 1950. That’s not perfect obviously and every correction/bear market is different but at least the odds, as best they can be calculated, are in your favor.

Market timing though should probably be a small part of your risk control strategy. We did some selling late last year and most of our clients came into the year with about 10% cash. And we did some buying in late March when the VIX closed above 30, but the effect on our portfolios was not large. What did have a big impact was asset allocation, which is the only true way to consistently reduce risk. Diversification is not something you do when you’re worried about a correction; it is something you do all the time. Making tactical changes in a volatile market, under duress so to speak, isn’t ideal, to say the least.

Investors were not without ways to make money in markets since the S&P peaked nearly 6 months ago.

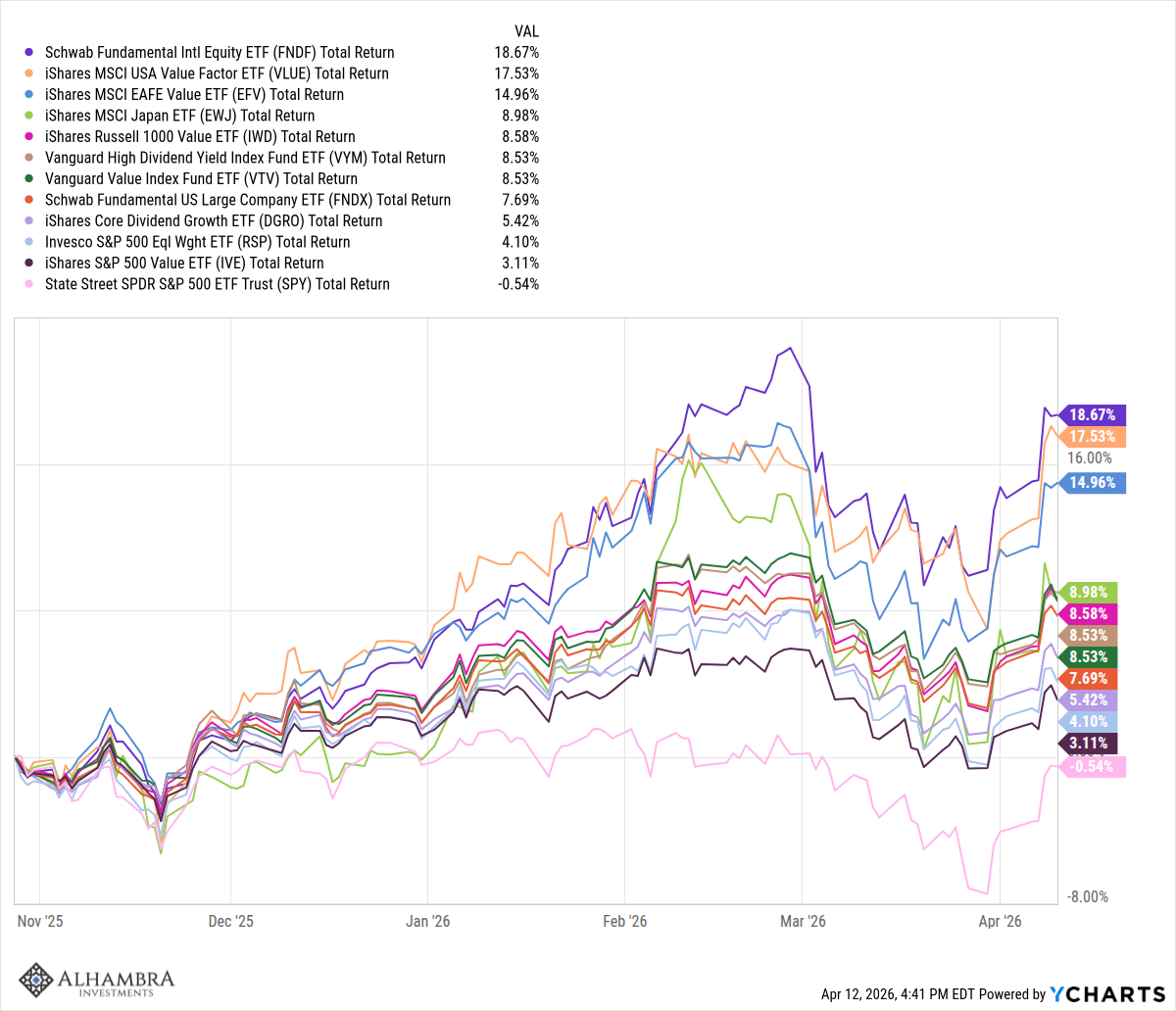

Let’s take a look at what has happened in large cap stocks since this correction started in late October. The S&P 500 has spent 5 1/2 months making you nothing but nervous but there were plenty of other tactical choices that did much better. I’m not suggesting you should own a long list like this but it shows how deep the bench was in this correction.

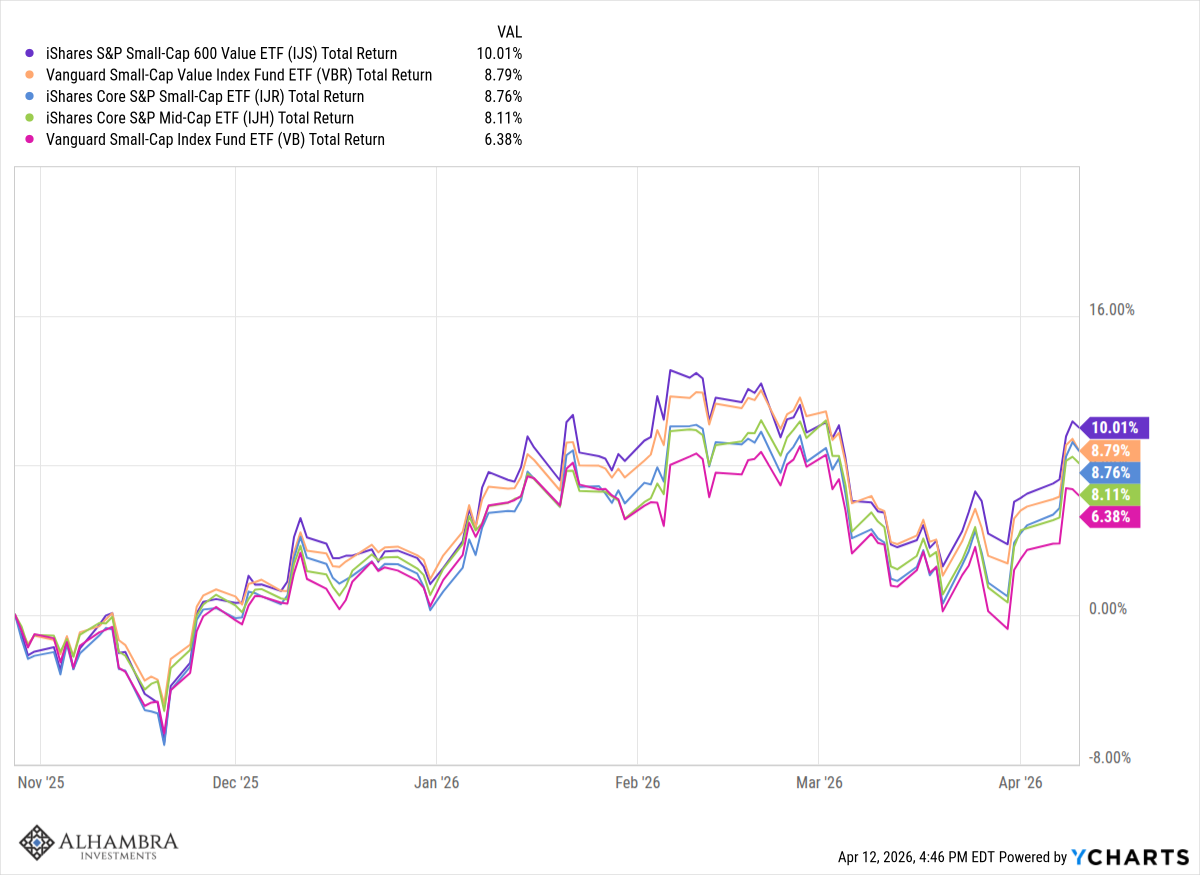

Small and mid-cap stocks have also outperformed:

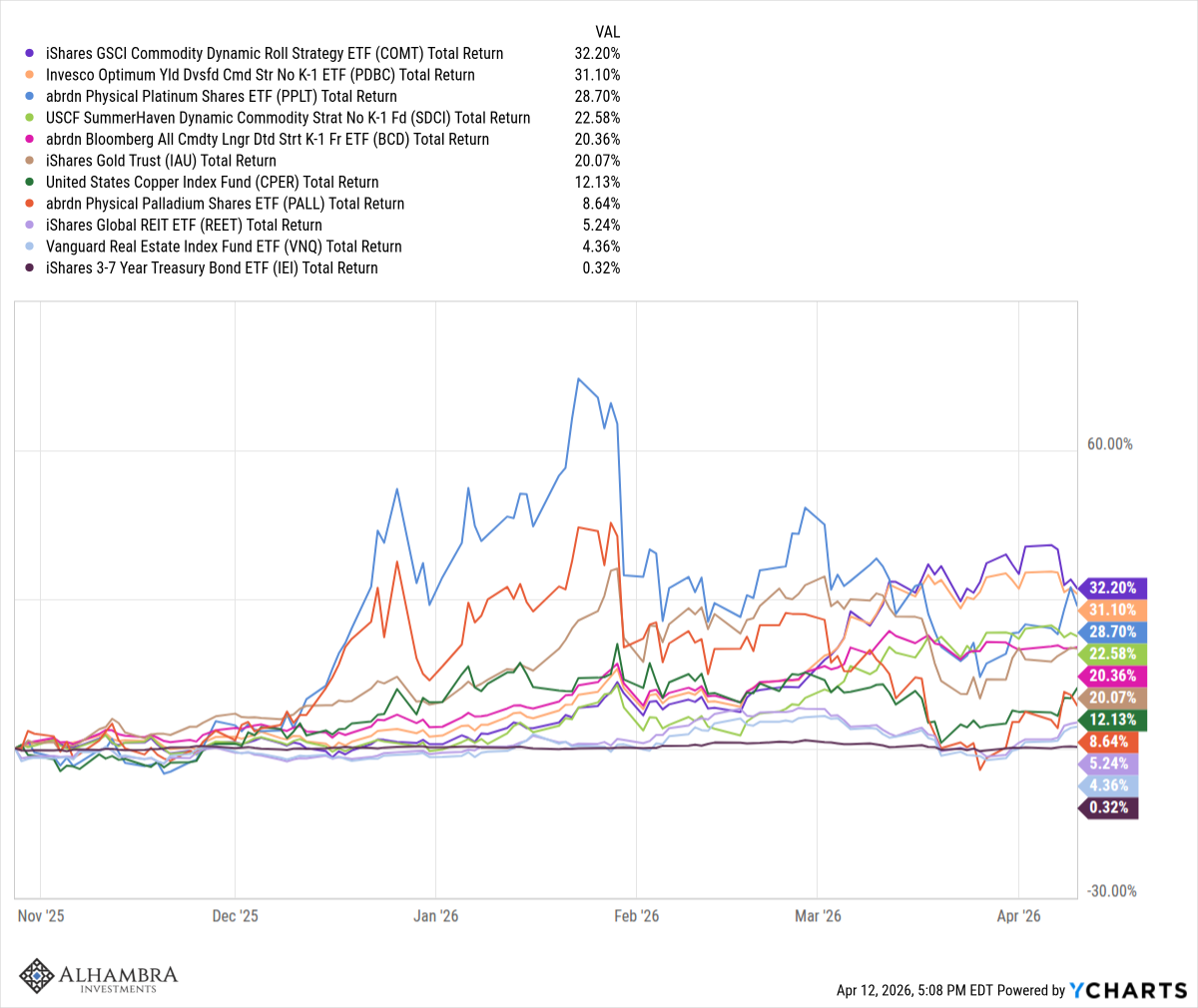

In the diversifying part of your portfolio, you’ve had better choices too. The traditional 60/40 portfolio diversification is achieved with bonds alone but that has lost some effectiveness over the last few years because stocks and bonds have been positively correlated. That happens in higher inflationary environments when interest rates tend to rise. There are other assets that have a low or negative correlation to stocks though and some of them have done quite well. A note of caution though. I see a lot of firms putting “liquid alternatives” in this part of your portfolio. In particular, private credit has been pushed pretty hard over the last few years and investors in these funds are now sitting on losses and limited – or no – liquidity. My personal rule is that if I can’t get paid by regular settlement, I’m not interested; liquidity doesn’t matter until it does and then it matters a lot.

We made a choice several years ago to diversify away from the S&P 500 because we were not comfortable with the large allocation to technology stocks. We shifted some of our US large cap investments overseas, some to value, and some to dividend growth. The international exposure was driven by our views on the dollar and has paid off nicely, especially over the last year. But those choices were not perfect, we didn’t get all the best performers. Diversification isn’t about getting it perfect; it’s about reducing the odds of a really bad outcome.

I don’t know what is going to happen with the war in Iran and neither do you. We can’t predict what’s going to happen next week or next month or even next year. When the range of potential outcomes is wide – and that is almost always true in markets but especially right now – the logical choice is to diversify widely.

Joe Calhoun

Stay In Touch