Personal intuition usually serves well in both economics and finance, which is why, despite all the billions of dollars and amazing efforts otherwise, this business is still an art and not a “science” (even pseudo-). I should have remembered as such the last time I actually reported on a sentiment survey, as the Chicago PMI a few months back tumbled precipitously. At first glance, it looked like the type of outlier that could have held some significance in the realm of post-revision inventory, but alas that collapse was met the following month by an equally “outlying” rise about back to where it all started.

The problem of sentiment surveys is not just the conspicuous lack of hard dollars that enforces a measure of “honesty” (currency is, after all, the primary means of measurement) but rather that the very intent contained within them almost never matches how they are interpreted. They are broadly and generally used to extrapolate all manner of biases and analysis, which is what I was guilty of doing with Chicago.

The latest ISM Manufacturing index offers an almost exact case in point. The current level matches a “recovery” high from back in the middle of 2011. So an index value of 59 must mean robust growth is in progress?

That certainly was not the case back in 2011, as that 59 represented the peak in the cycle. In other words, the ISM Manufacturing three years ago told us nothing about future prospects and only denoted a minor relativism with what came immediately before it. That was the proper interpretation then, and it survives even now after the massive revisions to the major economic accounts.

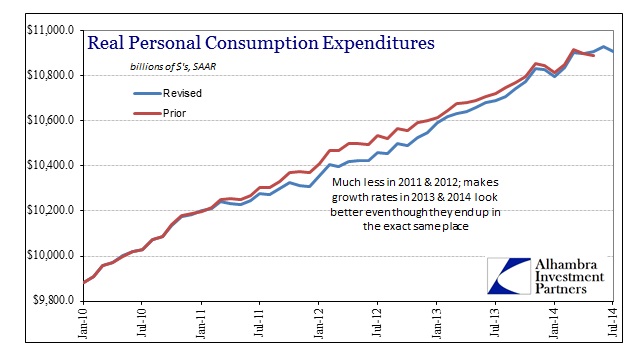

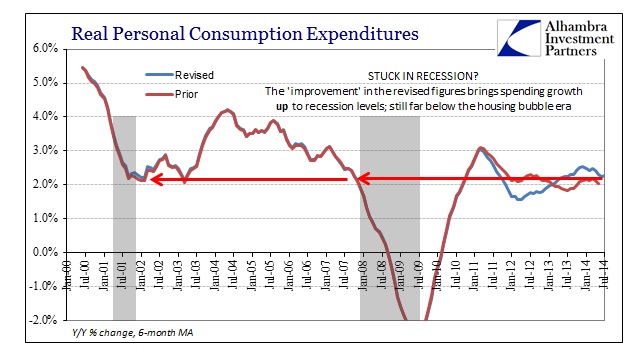

The GDP revisions took away a significant amount of growth that was believed to have occurred in 2011 and 2012 – in other words that ISM of 59 looks even more suspicious right now than it did back then. Those revisions were also applied to wages, income and even household spending (PCE). The chart above shows just how much spending was “lost” in the revised calculations, starting, oddly enough, right around the month the ISM was peaking the last time.

That means that all those extrapolations of how the ISM was a leading indicator of consumer spending turned out to be instead highly misleading. As we know from numerous other accounts (always searching for corroboration because of these inconsistencies that seem to be gaining in scope and scale) growth broadly decelerated from that point (and the revisions say has accelerated slightly once more).

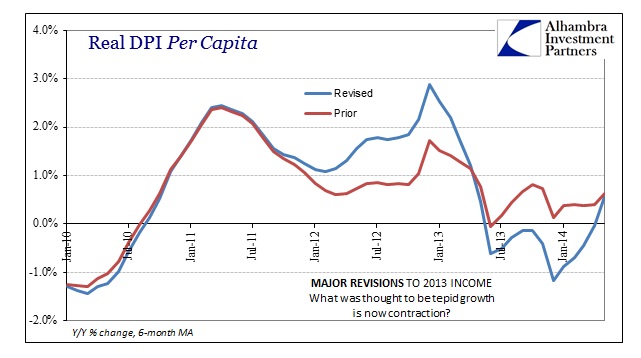

That might be understating a lot about the changes in income, in particular. The revised track of income growth (using real DPI per capita) is wholly different. In what is clearly an oddity, income growth was revised much higher in 2012 and much lower in 2013 – reversing the course of GDP and spending revisions fully. It isn’t clear if the BEA has rethought and recurved just how much of an effect the tax law changes then had on the timing of income payments, but even with that as a factor it does not explain the full manner of what they now say transpired.

To see Real DPI Per Capita drop negative for nearly all of 2013 is not only highly unusual, it is contradictory to pretty much everything about the mainstream narrative. In fact, such sustained negativity in income is highly recessionary, reserved exclusively for just such periods.

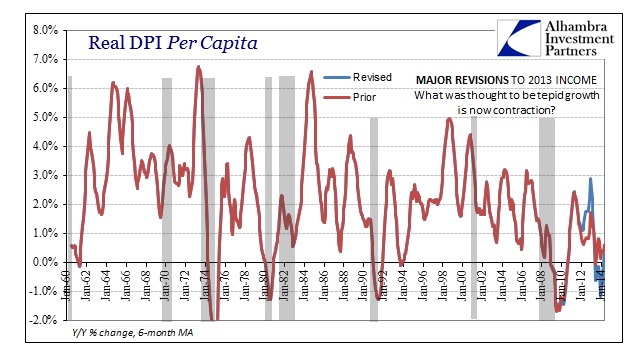

The data series begins in 1959 and the only periods where income is negative for more than a month or two (and that only happened once in 1993) coincides with recession. That should be alarming, raising the very real possibility that the US economy is not in some stable “muddle” but may have become as unstable as the European experience with repeated contraction. That would suggest that any “growth” estimated now is rather just another bounce off such a downslope; alternating between contraction and absence of contraction rather than full recovery.

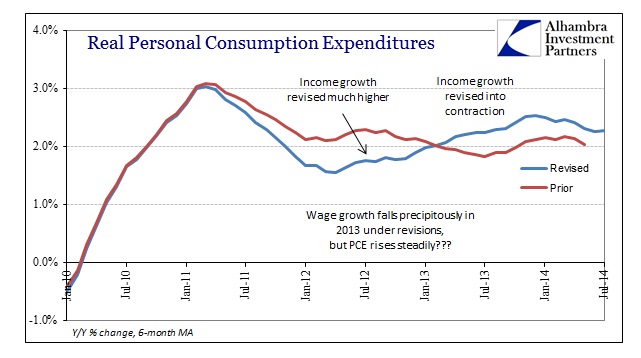

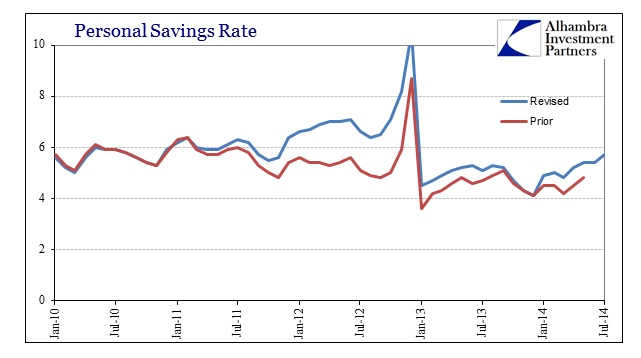

What is even more curious, however, is the reversal of pattern next to consumer spending. Real PCE has been revised downward, as stated above, in 2012 and upward in 2013. That leads to a situation where spending is doing the exact opposite of income?

The only way that makes sense, mathematically, is through an upward shift of the entire track of the personal savings rate. The statistical count now shows that consumers have been uniformly saving throughout the period, rather than the obvious downslope that usually accompanies such “cycles.”

The savings rate was moved upward in 2011 and especially 2012 not because of income alone rising, but because the level of spending is now viewed to be, contra the 2011 ISM euphoria, significantly less. Thus, somehow, the savings rate now takes on this odd shape of rising into the end of 2012 and then jumping lower into the disagreement (in the opposite direction) between income and spending in 2013.

Whatever the case with income changes, there is at least consistency on a much larger (and much more important) scale with broad perspective. Despite revisions to the immediate trajectory of spending growth, the slow ascent does nothing in this wider framework toward suggesting economic health of any kind. In fact, it has taken these odd revisions just to get back to a level consistent with mild recession (2001), which is equal or lessor with the onset of the Great Recession.

Where these revisions look as if the economy is gaining, even if that turns out to survive further revisions in the near future (and then more thereafter) it doesn’t amount to all that much. And that is the problem here, as the focus has been ground down to nothingness, a reductionism in standards that belies the bigger picture of “recovery.” And even if the US is avoiding, somewhat, the European experience, that also amounts to very little comfort as the most charitable interpretation here is chronic instability. Some might call it the “Lesser Depression.”

As secular stagnation gains in acceptance, we won’t have to wonder if it is valid, only advancing great argument about where this is all heading and why it is occurring. In that regard, you would think the orthodox position vis a vis sentiment surveys would be much more cautious; not just because they don’t mean what people think they mean, but rather there appears to be a very serious contrarian element to them.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch